- Introduction

- Implications of the Investment Requirement Scenarios

- Highway and Bridge Investment Requirements

- Investment Requirements for Highway Preservation and Capacity Expansion

- Investment Requirements for Bridge Preservation

- Investment Requirements for System Enhancements

- Transit Investment Requirements

- Comparisons Between Reports

- The Economic Approach to Transportation Investments

- Background

- Economic Focus Versus Engineering Focus

- Multimodal Analysis

- Uncertainty in Transportation Investment Requirements Modeling

- Congestion Pricing and Investment Requirements

- Chapter 7: Capital Investment Requirements

- Chapter 8: Comparison of Spending and Investment Requirements

- Chapter 9: Impacts of Investment

- Chapter 10: Sensitivity Analysis

Introduction

Chapters 7 through 10 present and analyze estimates of future capital investment requirements for highways, bridges, and transit. These chapters provide general investment benchmarks as a basis for the development and evaluation of transportation policy and program options. The 20-year investment requirement estimates shown in these chapters reflect the total capital investment required from all sources to achieve certain levels of performance. They do not, however, directly address which revenue sources might be used to finance the investment required by each scenario, nor do they identify how much might be contributed by each level of government.

These four investment-related chapters include the following analyses:

Chapter 7, Capital Investment Requirements, provides estimates of future capital investment requirements under different scenarios. The "Cost to Maintain" scenarios for highways and bridges and for transit are designed to show the investment required to keep future indicators of conditions and performance at current levels. The "Cost to Improve" scenarios for highways and bridges and for transit are intended to define the upper limit of appropriate national investment based on engineering and economic criteria. The benchmarks included in this chapter are intended to be illustrative and do not represent comprehensive alternative transportation policies.

Chapter 8, Comparison of Spending and Investment Requirements, relates the estimates presented in Chapter 7 to current and anticipated highway and transit capital expenditures in the United States. The chapter identifies "gaps" that may exist between current funding levels and future investment requirements under different scenarios. It also compares the current mix of highway and transit capital spending by type of improvement (especially preservation and expansion) to the future investment mix suggested by the models.

Chapter 9, Impacts of Investment, relates historic capital funding levels to recent condition and performance trends. It also analyzes the projected impacts of different future levels of investment on measures of physical conditions, operational performance, and system use.

Chapter 10, Sensitivity Analysis, explores the impact that varying travel growth forecasts and some other key assumptions would have on investment requirements. The investment requirement projections in this report are developed using models that evaluate current system condition and operational performance, and make 20-year projections based on certain assumptions about the life spans of system elements, future travel growth, and other model parameters. The accuracy of these projections depends in large part on the underlying assumptions used in the analysis. The uncertainty inherent in the estimates is further discussed in this introduction.

Unlike Chapters 1 through 6, which largely include highway and transit statistics drawn from other sources, the investment requirement projections presented in these chapters (and the models used to create the projections) were developed exclusively for the C&P report. The procedures for developing the investment requirements have evolved over time, to incorporate new research, new data sources, and improved estimation techniques relying on economic principles. The methodologies used to estimate investment requirements for highways, bridges, and transit are discussed in greater detail in Appendices A, B, and C.

The move from a purely engineering approach to one incorporating economic analysis is consistent with the movement of transportation agencies toward asset management, value engineering, and greater consideration of cost effectiveness in decision making. The economic approach to transportation investment is discussed in greater detail below.

Implications of the Investment Requirement Scenarios

The 20-year capital investment requirement projections shown in this report reflect complex technical analyses that attempt to predict the impact that capital investment may have on the future conditions and performance of the transportation system. While the discussion focuses heavily on the impacts of investing in a manner consistent with "Cost to Maintain" and "Cost to Improve" scenarios, these represent only two points on a continuum of alternative investment levels. The Department does not endorse either of these scenarios as a target level of investment. Where practical, supplemental information has been included to describe the impacts of other possible investment levels.

This report does not attempt to address issues of cost responsibility. The investment requirement scenarios predict the impact that particular levels of combined Federal, State, local, and private investment might have on the overall conditions and performance of highways, bridges, and transit. While Chapter 6 provides information on what portion of highway investment has come from different revenue sources in the past, the report does not make specific recommendations about how much could or should be contributed by each level of government in the future.

While this report identifies the amount of additional spending above current levels that would be required to achieve certain performance benchmarks, it makes no assumptions about the types of revenues required to support this additional spending. This is significant, as increased funding from general revenue sources (such as property taxes, sales taxes, income taxes, etc.) could have different implications than increased funding from user charges (such as fuel taxes, tolls, and fares). For example, if investment in urban freeways were to be increased dramatically, more drivers would tend to use the newly improved routes. However, if fuel taxes were simultaneously increased to pay for the improvements, this would raise the cost of driving generally, possibly causing some marginal trips to be deterred. If tolls were simultaneously imposed on urban freeways to pay for the improvements, this would likely discourage additional marginal trips and encourage some drivers to switch to nontolled routes. Research is underway to quantify the potential impacts of alternative financing mechanisms on future investment requirements, and is discussed in Part V. The possible implications of congestion pricing in particular are discussed in more detail below.

Highway and Bridge Investment Requirements

Estimates of investment requirements for highways and bridges are generated independently by separate models and techniques, and the results are combined for the key investment scenarios. The Cost to Maintain Highways and Bridges combines two different scenarios: the Maintain User Costs scenario from the Highway Economic Requirements System (HERS), and the Maintain Economic Backlog scenario from the National Bridge Investment Analysis System (NBIAS). The Maximum Economic Investment for (Cost to Improve) Highways and Bridges combines the comparable scenarios from HERS and NBIAS.

As in the 2002 edition of the C&P report, the costs reported for the two scenarios also include adjustments made using external procedures. By doing so, capital investment requirements for elements of system preservation, system expansion, and system enhancement that are not modeled in NBIAS or HERS can be estimated. The investment requirements shown should thus reflect the realistic size of the total highway capital investment program that would be required in order to meet the performance goals specified in the scenarios.

Investment requirements are also reported and analyzed in Chapters 7 and 8 by highway functional class and by improvement type.

Investment Requirements for Highway Preservation and Capacity Expansion

Investment requirements for highway preservation and capacity expansion are modeled by HERS. While this model was primarily designed to analyze highway segments, HERS also factors in the costs of expanding bridges and other structures when deciding whether to add lanes to a highway segment. All highway and bridge investment requirements related to capacity are modeled in HERS; NBIAS considers only investment requirements related to bridge preservation and bridge replacement.

The Transportation Act for the 21st Century (TEA-21) required that this report include information on the investment requirement backlog. It also required that this report provide greater comparability with previous versions of the C&P report. As in the 2002 edition, this report defines the highway investment backlog as all highway improvements that could be economically justified to be implemented immediately, based on the current condition and operational performance of the highway system. An improvement is considered economically justified when it corrects an existing deficiency, and its benefit/cost ratio (BCR) is greater than or equal to 1.0; i.e., the benefits of making the improvement are greater than or equal to the cost of the improvement. Appendix A includes data showing the separate effects of changes in modeling techniques and changes in the underlying data on the investment analysis.

Two HERS scenarios related to the "Cost to Maintain" and "Cost to Improve" scenarios are developed fully in this report: the Maintain User Costs scenario and the Maximum Economic Investment scenario. Other benchmarks are also identified in Chapter 9.

The Maintain User Costs scenario shown in Chapter 7 and the other benchmarks shown in Chapter 9 were developed by imposing a budget constraint on the HERS analysis. Under this procedure, potential highway improvements are implemented (in descending order of BCR) until the funding constraint is reached. The funding constraints are then lowered until the point where these key indicators would be maintained at current levels, rather than improving. For the Maintain User Costs scenario, the funding constraint was lowered until the point where highway user costs (travel time costs, vehicle operating costs, and crash costs) in 2022 would match the baseline highway user costs calculated from the 2002 data. Under this investment strategy, existing and accruing system deficiencies would be selectively corrected. Some highway sections would improve, some would deteriorate; overall, average highway user costs in 2022 would match that observed in 2002.

One concern that has been raised with this scenario is whether this level of funding would be adequate to meet the specified performance goal. While the Maintain User Costs scenario assumes that projects would be carried out strictly in descending order of benefit-cost ratio, this is unlikely to be the case in reality. The actual amount required to achieve this performance objective would be higher if some projects with lower BCRs were carried out instead of projects with higher BCRs. This issue is discussed in a Q/A box on page 7-12, titled "How closely does the HERS model simulate the actual project selection process of State and local highway agencies?"

The Maximum Economic Investment scenario would correct all highway deficiencies when it is economically justified. This scenario would address the existing highway investment backlog, as well as other deficiencies that will develop over the next 20 years due to pavement deterioration and travel growth. This scenario implements all improvements with a BCR greater than or equal to 1.0. Under this scenario, key indicators such as pavement condition, total highway user costs, and travel time would all improve. However, it should be noted that simply increasing spending to the Maximum Economic Investment level would not guarantee that these funds would be expended in a cost-beneficial manner. Achieving the projected results for this scenario would require a combination of increasing spending and modifying Federal highway program requirements and State and local government practices to ensure that no project would be implemented unless its estimated benefits exceeded its estimated costs.

Further information on changes in the highway investment methodology is provided in Appendix A.

Investment Requirements for Bridge Preservation

The bridge section begins with a discussion of the NBIAS model, which was used for the first time in the 2002 edition of the C&P report. Unlike previous bridge models, NBIAS incorporates benefit-cost analysis into the bridge investment requirement evaluation.

This section discusses the current investment backlog and two future investment requirement scenarios. As noted earlier, the amounts reported in this section relate only to bridge preservation and replacement. All investment requirements related to highway and bridge capacity are estimated using the HERS model.

The investment backlog for bridges is calculated as the total investment required to address deficiencies in bridge elements and some functional deficiencies when it is cost-beneficial to do so. Note that this analysis takes a broader approach to assessing deficiencies and does not focus on whether a bridge would be considered structurally deficient or functionally obsolete by the criteria outlined in Chapter 3.

Under the Maintain Economic Backlog scenario, existing deficiencies and newly accruing deficiencies would be selectively corrected such that the total economic backlog of cost-beneficial investments required to correct bridge deficiencies at the end of the 20-year analysis period would be the same as the current amount. Under the Maximum Economic Investment scenario, all cost-beneficial bridge replacement, improvement, repair, or rehabilitation improvements would be implemented.The NBIAS model and other changes in bridge investment requirements modeling in this report are presented in Appendix B.

Investment Requirements for System Enhancements

The FHWA currently does not have a model for estimating requirements for future investment in system enhancements. As a result, the methodology employed in Chapter 7 assumes that such investments will remain constant in the future as a share of the overall highway capital program, increasing or decreasing with the level of investment in system preservation and expansion. The purpose of this adjustment is to allow the total highway and bridge capital investment requirements to be directly compared with the capital spending data presented in Chapter 6.

A similar procedure is applied to investment on rural minor collectors and rural and urban local roads, which are not included in the data used in the HERS model. Chapter 7 includes more information on the estimation of nonmodeled highway investment requirements.

Transit Investment Requirements

The transit section of Chapter 7 begins with a discussion of the Transit Economic Requirements Model (TERM), used to develop the investment requirement scenarios for this report. The TERM uses separate modules to analyze different types of investments: those that maintain and improve the physical condition of existing assets, those that maintain current operating performance, and those that would improve operating performance. The TERM subjects projected investments at each transit operator to a benefit-cost test. Only those with a benefit-cost ratio greater than 1.0 are included in TERM's estimated investment requirements. The TERM methodology is presented in greater detail in Appendix C.

The Cost to Maintain scenario maintains equipment and facilities in their current state of repair and maintains current operating performance while accommodating future transit growth. These investments are modeled at the transit agency level and on a mode-by-mode basis. The Cost to Improve scenario determines the additional investment requirements to improve the condition of transit assets to a "good" rating and improve the performance of transit operations to targeted levels. A cost-benefit analysis is performed on these investments on an urbanized area basis.

Breakdowns of transit investment requirements by type of improvement, type of asset, and urbanized area size are also presented for both the Cost to Maintain and the Cost to Improve scenarios.

Comparisons Between Reports

The investment requirement estimates presented in Part II are intended to be comparable with previous editions of the C&P report. However, it is important to consider several factors when making such comparisons:

Different Base Years. Future investment requirements are calculated in constant base year dollars. However, since the base year changes between reports, inflation alone will cause the estimates to tend to rise over time.

Changes in Condition or Performance. Changes in the physical condition or operational performance of the highway or transit systems may affect the estimates of investment requirements between reports. However, the effects are likely to be different for the "Maintain" and "Improve" scenarios.

Cost to Improve. If the condition or performance of the underlying system deteriorates over time, then the models are likely to find more improvement projects to be cost beneficial, or to find more improvements necessary to improve the condition or performance of the system. As a result, the Cost to Improve would be likely to increase over time. The opposite would be true if system conditions and performance were to improve over time.

Cost to Maintain. The "Maintain" scenarios for both highways and transit are tied to the condition and performance of the system in the base year. If conditions and performance are improving over time, however, the "target level" of the "Maintain" scenarios will be likewise increasing between reports (resulting in a "raised bar" for these scenarios). As a result, the Cost to Maintain is likely to increase over time for this reason. Conversely, if system condition and performance are deteriorating over time, then the "Maintain" scenarios in subsequent reports would represent a declining standard that is being maintained.

Expansion of the Asset Base. As the Nation's highway and transit systems expand over time, the cost of maintaining this larger asset base will also tend to increase. For assets with useful lifetimes of less than 20 years, future expansions will also affect the 20-year investment requirement estimates.

Changes in Technology. Changes in transportation technology may cause the price of capital assets to increase or decrease over time and thus affect the estimates of capital investment requirements.

Changes in Scenario Definitions. Although the C&P report series has consistently reported investment requirements for "Improve" and "Maintain" scenarios over time, the exact definition of these scenarios may change from one report to another. Such changes are explicitly noted and discussed in the text of the report when this occurs.

Changes in Analytical Techniques. The models and procedures used to generate the investment requirement estimates are subject to ongoing refinements and improvements, resulting in better estimates over time. The underlying data series used as inputs in the models may also be subject to changes in reporting requirements over time.

The Economic Approach to Transportation Investments

Background

The methods and assumptions used to estimate future highway, bridge, and transit investment requirements are continuously evolving. Since the beginning of the highway report series in 1968, innovations in analytical methods, new empirical evidence, and changes in transportation planning objectives have combined to encourage the development and application of improved data and analytical techniques. Estimates of future highway investment requirements, as reported in the 1968 National Highway Needs Report to Congress, began as a combined "wish list" of State highway "needs." As the focus of national highway investment changed from system expansion to management of the existing system during the 1970s, national engineering standards were defined and applied to identify system deficiencies, and the investments necessary to remedy these deficiencies were estimated. By the end of the decade, a comprehensive database, the HPMS, had been developed to monitor highway system conditions and performance nationwide.

By the early 1980s, a sophisticated simulation model, the HPMS Analytical Process (AP), was available to evaluate the impact of alternative investment strategies on system conditions and performance. The procedures used in the HPMS-AP were founded on engineering principles: engineering standards were applied to determine which system attributes were considered deficient, and improvement option "packages" were developed using standard engineering practice to potentially correct given deficiencies, but without consideration of comparative economic benefits and costs.

In 1988, the FHWA embarked on a long-term research and development effort to produce an alternative simulation procedure combining engineering principles with economic analysis, culminating with the development of the HERS. The HERS was first utilized to develop one of the two highway investment requirement scenarios presented in the 1995 C&P report. In subsequent reports, HERS has been used to develop all of the highway investment scenarios.

Executive Order 12893, Principles for Federal Infrastructure Investments, issued on January 26, 1994, directs that Federal infrastructure investments be selected on the basis of a systematic analysis of expected benefits and costs. This order provided additional momentum for the shift toward developing analytical tools that incorporate economic analysis into the evaluation of investment requirements.

In the 1997 C&P report, FTA introduced the TERM, which was used to develop both of the transit investment requirement scenarios. The TERM incorporates benefit-cost analysis into its determination of transit investment levels.

The 2002 C&P report introduced the NBIAS, incorporating economic analysis into bridge investment requirements modeling for the first time.

Economic Focus Versus Engineering Focus

The economic approach to transportation investment relies fundamentally upon an analysis and comparison of the economic benefits and costs of potential investments. By providing benefits whose economic value exceeds their costs, projects that offer "net benefits" have the potential to increase societal welfare and are thus considered to be "good" investments from a public perspective. The cost of an investment in transportation infrastructure is simply the straightforward cost of implementing an improvement project. The benefits of transportation capital investments are generally characterized as the attendant reductions in costs faced by transportation agencies (such as for maintenance), users of the transportation system (such as savings in travel time and vehicle operating costs), and others who are affected by the operation of the transportation system (such as reductions in health or property damage costs).

Traditional engineering-based analytical tools focus mainly on estimating transportation agency costs and the value of resources required to maintain or improve the condition and performance of infrastructure. This type of analytical approach can provide valuable information about the cost effectiveness of transportation system investments from the public agency perspective, including predicting the optimal pattern of investment to minimize life-cycle costs. However, this approach does not fully consider the potential benefits to users of transportation services from maintaining or improving the condition and performance of transportation infrastructure.

By incorporating the value of services that transportation infrastructure provides to its users, the HERS, TERM, and NBIAS models each have a broader focus than traditional engineering-based models. They also attempt to take into account some of the impacts that transportation activity has on nonusers and recognize how investments in transportation infrastructure can alter the economic costs of these impacts. By expanding the scope of benefits considered in their analysis, these models are able to yield an improved understanding of existing and future investment needs for the Nation's surface transportation system.

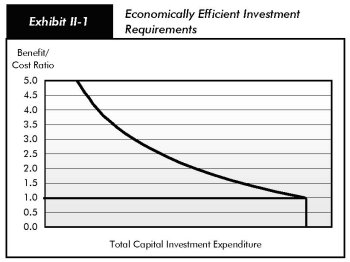

One way to conceptualize the goal of the HERS, TERM, and NBIAS models is shown in Exhibit II-1. For some investment projects, the benefits to transportation system users and others greatly exceed the costs of that investment, resulting in large net benefits and a high BCR. As additional projects are considered and implemented, however, the gap between benefits and costs of subsequent projects diminishes. Thus, their BCRs progressively decline, eventually reaching a point (at a BCR of 1.0) where selecting additional investment projects will no longer increase net benefits from the overall investment program. Projects that do not meet this threshold of economic viability (because they do not offer positive net benefits and thus cannot increase total net benefits provided by transportation system infrastructure) will not be selected or implemented by any of the three models.

Using this economics-based approach to analyze potential transportation investment is likely to result in different decisions about the catalog of desirable improvements than would be made using a purely engineering-based approach. For example, if a highway segment, bridge, or transit system is greatly underutilized, benefit-cost analysis might suggest that it would not be worthwhile to fully preserve its condition or to address its engineering deficiencies. Conversely, a model based on economic analysis might recommend additional investments to expand capacity or improve travel conditions above and beyond the levels dictated by an analysis that simply minimized engineering life-cycle costs, if doing so would provide substantial benefits to the users of the system.

The economics-based approach also provides a more sophisticated method for prioritizing potential improvement options when funding is constrained. By identifying investment opportunities in order of the net benefits they offer, economic analysis helps to provide guidance in directing limited transportation capital investment resources toward the types of system improvements that can together provide the largest benefits to transportation system users.

Multimodal Analysis

The HERS, TERM, and NBIAS all use a consistent approach for determining the value of travel time and the value of reducing transportation injuries and fatalities, which are key variables in any economic analysis of transportation investment. While HERS, TERM, and NBIAS all utilize benefit-cost analysis, their methods for implementing this analysis, however, are very different. The highway, transit, and bridge models each rely on separate databases, making use of the specific data available for only one part of the transportation system and addressing issues unique to each mode.

These three models have not yet evolved to the point where direct multimodal analysis would be possible. For example, HERS assumes that, when lanes are added to a highway, this causes highway user costs to fall, resulting in additional highway travel. Some of the increased use of the expanded facility would result from newly generated travel, while some would be the result of travel shifting from transit to highways. However, HERS is unable to distinguish between these different sources of additional highway travel. At present, there is no direct way to analyze the impact that a given level of highway investment would have on transit investment requirements (or vice versa). Opportunities for future development of HERS, TERM, and NBIAS, including efforts to allow feedback between the models, are discussed in Part V.

Uncertainty in Transportation Investment Requirements Modeling

The three investment requirement models used in this report are deterministic rather than probabilistic, meaning that they provide a single projected value of total investment requirements rather than a range of likely values. As a result, it is only possible to make general statements about the limitations of these projections, based on the characteristics of the process used to develop them, rather than giving specific information about confidence intervals.

As in any modeling process, simplifying assumptions have been made to make analysis practical and to meet the limitations of available data. While potential highway improvements are evaluated based on benefit-cost analysis, not all external costs (such as noise pollution) or external benefits (such as the favorable impacts of highway improvements on productivity and competition in the economy) that may be considered in the actual selection process for individual projects are reflected in the investment models. Across a broad program of investment projects, such external effects are likely to cancel each other out, but to the extent that they do not, "true" investment requirements may be either higher or lower than those predicted by the model. Some projects that HERS, TERM, or NBIAS view as economically justifiable may not be after more careful scrutiny, while other projects that the models would reject might actually be justifiable if these other factors were considered.

While it is not possible to present precise confidence ranges for the estimates found in this report, it is possible to examine the sensitivity of the estimates to changes in some of the key parameters underlying the models. Such an analysis is presented in Chapter 10.

Congestion Pricing and Investment Requirements

When highway users make decisions about whether, when, and where to travel, they consider both the implicit costs (such as travel time and safety risk) and explicit, out-of-pocket cost (such as fuel costs and tolls) of the trip. Under normal operating conditions, their use of the road will not have an appreciable effect on the costs faced by other users. As traffic volumes begin to approach the carrying capacity of the road, however, traffic congestion and delays begin to set in and travel times for all users begin to rise, with each additional vehicle making the situation progressively worse. However, individual travelers do not take into account the delays and additional costs that their use of the facility imposes on other travelers, focusing instead only on the costs that they bear themselves. Economists refer to this divergence between the costs an individual user bears and the total added costs each additional user imposes as a congestion externality. Ignoring this externality is likely to result in an inefficiently high level of use of congested facilities, resulting in a loss of some of their potential benefits to users.

In an ideal (from an economic point of view) world, users of congested facilities would be levied charges precisely corresponding to the economic cost of the delay they impose on one another, thereby "internalizing" the congestion externality, reducing peak traffic volumes (but not necessarily eliminating all congestion delay), and increasing net benefits to users. In such a case, the economically efficient level of investment in highways would depend only on the cost of building, preserving, and operating highways; users' valuation of travel time; and the rate of interest.

In the absence of efficient pricing, options for reducing congestion externalities and increasing societal benefits are limited. One possibility would be to invest in additional roadway capacity, thereby reducing congestion generally and the attendant costs that highway users impose on one another. In other words, the efficient level of investment in highway capacity is likely to be larger under the current system of highway user charges (primarily fuel taxes) than would be the case with full-cost pricing of highway use. The current situation is sometimes referred to as a "second-best" solution to the problem of optimal highway investment.

In the real world, a number of barriers exist to the implementation of a perfectly efficient congestion pricing system. Calculating and collecting tolls impose costs on both operators and users of a toll facility, and achieving the true optimum would require both a comprehensive knowledge of user demand and the ability to continuously adjust the fees that motorists are charged. However, as these barriers are being reduced, it is becoming increasingly possible to make the current system more efficient through variable road pricing. Significant advances in tolling technology have reduced both the operating costs of toll collection and the delays experienced by users from having to stop or slow down at collection points. Technology has also made it possible to charge different toll rates during different time periods, in some cases even varying the price dynamically with real-time traffic conditions. While many of these technologies require extensive roadway infrastructure (and would thus likely be deployed only on high-volume, limited access roads), other GPS-based, in-vehicle technologies are being developed that could make it possible to assess fees on virtually any roadway (though such technologies would have their own issues and limitations that could inhibit widespread adoption and use). To the extent that such charges reflect the underlying external costs, they can reduce the welfare loss due to the underpricing of road capacity. The economically efficient level of infrastructure investment under a regime of partial pricing could also be reduced accordingly.The implications of inefficient pricing for the highway investment requirements estimated in this report are difficult to quantify precisely. The HERS model selects economically efficient improvements to sample highway sections at prices that reflect only costs currently borne privately by highway users (including fuel taxes). In the case of the "Maximum Economic Investment" scenario, the discussion above would indicate that the level of investment under this scenario would be reduced to some degree if efficient road pricing were widespread, with a stronger impact on capacity investment than on preservation improvements. The "Maintain User Costs" scenario, however, is defined based on a performance target, which makes the impact of imposing a more efficient pricing structure less clear. The key issue is how any increases in tolls or fees would be considered with respect to the user cost target. From an economic point of view, taxes and tolls would be excluded from the computation of user costs in evaluating the benefits of improvements, treating them instead as transfer payments, and would thus be excluded from calculations determining whether the target has been reached. Charging users higher prices for traveling during high-demand periods would simply reduce peak traffic volumes and thus the need for additional investment. However, imposing congestion-based tolls would raise the actual out-of-pocket costs experienced by users, and an argument can be made that they should be included in the performance target, to avoid a "Maintain" scenario in which drivers are effectively worse off in 20 years than they are today. In this case, offsetting the cost of the congestion-based tools would require additional investment in system improvements. At the same time, however, travel would be reduced as a result of the tolls, with a corresponding impact on investment requirements. The net effect on estimated investment requirements for such a scenario could thus be either higher or lower with more efficient pricing if tolls are included in the calculation of the performance target.

The FHWA has research underway that will attempt to address some of these issues regarding pricing and its consequences for efficient investment levels by incorporating new capabilities into the HERS model. The initial products of this research effort should be available in time for inclusion in the 2006 edition of the C&P report. The "Pricing Effects" section in Part V of this report provides a further discussion of this and other ongoing research activities that will be reflected in future editions of this report. This section also references a separate ongoing research effort commissioned by the DOT's Office of Economic and Strategic Analysis under the Assistant Secretary for Transportation Policy, which is focused on developing quantitative illustrations of some of the impacts that widespread implementation of congestion pricing could have on future highway travel and investment.

While the above discussion focuses on highway pricing, the same considerations may apply to transit investments in some cases. While most transit routes have excess capacity (measured either in terms of passengers per vehicle or vehicles per route mile), some heavily used lines in major metropolitan areas do approach their passenger-carrying capacities during peak travel hours, with commensurate deterioration in the quality of service. As with highways, some of this overcrowding could be related to the underpricing of transit service during rush hours. However, also as with highways, practical considerations may limit the ability of transportation authorities to price transit service more efficiently. Further, these overcrowded transit lines are often in corridors with heavily congested highway service, making a joint solution to the pricing problems on both highways and transit not only more important to impose, but also more complicated to analyze, devise, and implement.