Exhibits

P3s represent a growing trend as a project delivery option for infrastructure projects in the U.S. The relative cost savings, efficiency gains, and allocation of project risks delivered by private sector participants in infrastructure development make P3s an attractive proposition for many transportation agencies. However, the associated transfers of cost, risk, and return to the private sector require transactions that often involve extensive negotiations of financial, structural, and legal agreements. An important consideration in these negotiations is the treatment of taxes and the impact of that treatment on project value.

While tax considerations are important for private sector bidders as well as city, state, and federal P3 sponsors, there is currently no specific federal legislation or policy that details the tax treatment of P3 projects. This is primarily because each P3 is unique by nature, pursued in light of the specifics of local economic and political conditions and structured to match the desired amount of private sector involvement of that particular project. The choice of legal structure is also heavily reliant on location and the relevant applicable tax laws at federal, state, or local levels.

This paper, therefore, seeks not to define a particular approach to tax implications and considerations for P3s, but attempts to highlight some key principles of P3 structures in the U.S. for both public and private sector participants.

A P3 may be subject to a variety of taxes depending on the jurisdiction in which it is located. Private sector P3 concessionaires are required to pay taxes associated with the operations of their business (i.e., the project). These direct taxes are paid by the concessionaire to federal, state, and local governments and therefore represent a potential benefit to the P3 sponsor.

In addition, if the P3 project stimulates economic activity, it may generate additional revenues through increased indirect tax receipts from property, sales, and other taxes not directly paid by the P3. However, this impact can often be considered to be a product of the project itself, not the project delivery method (P3 vs. traditional). Accordingly, the indirect tax impacts of the project are often considered by the public sector sponsor when deciding to proceed with the project, but are not analyzed further when analyzing which project delivery mechanism to use (P3 or conventional). We note that, depending on how this analysis is performed, it may understate the benefits of P3's, which are often pursued to accelerate project development and to ensure that maintenance standards are maintained through the lifecycle of an asset, which could result in accelerated and increased indirect taxes.

Examples of direct taxes that may be typically levied on a P3 project (including at the investor level) are shown in Exhibit A, and a description of these taxes are provided below 2:

| Federal | State | Local | |

|---|---|---|---|

| Income Tax | ✔ Check mark | ✔ Check mark | |

| Sales Tax | ✔ Check mark | ✔ Check mark | |

| Property Tax | ✔ Check mark | ✔ Check mark |

Exhibit A above describes the direct taxes that generally can be levied on a P3 project at the Federal, State, and Local level. The primary tax levied at the Federal level is the income tax, while States may levy Income, Sales, and Property taxes. At the Local level, primarily Sales and Property taxes can be applied on a P3 project.

As a general rule, taxes levied directly on the P3 project will increase the cost of the project to the private sector partner. This cost, in turn, will be passed through to either: (i) the public sponsor through higher availability payments or up-front contributions, which may result in lower up-front cash payments from the private sector, or (ii) users of the project through higher user fees.

Significant heterogeneity surrounds the tax treatment of P3s. While non-specificity of tax rules and regulations is a contributing factor, there is also significant variation in the tax strategies and structures of winning bidders in addition to bespoke federal, state, and local tax concessions granted to a given infrastructure project. Analysis of these tradeoffs will be an important factor in negotiations between the public and private parties. Gaining a better understanding of historical risks related to the generation of tax revenues can be helpful to performing this analysis. In Exhibit B we further detail how a sponsor might compare projected and actual project revenues to better understand the risks related to tax projections for P3 projects.

| P3s are often large-scale projects based on their cost, economic impact, and project life-cycle. This is particularly true in the United States where access to low cost, long-term debt in the municipal bond market and a diversity of permitted contracting mechanisms (e.g., Design-Build contracts and Performance-based operating agreements) may make public project delivery relatively more competitive than in other parts of the world. Actual tax revenues generated by these projects are often difficult to determine as the private owners of these projects are not typically required to disclose this information, except the estimates used in the original financial projections (to the extent bid models are disclosed). As a proxy, comparing actual revenues to the original projected revenues for the project, one may be able to infer a similar performance of tax revenue streams and other related benefits to the government. |

The economic activity generated by a P3 can be divided into direct and indirect economic activity. Direct economic activity is activity associated with the construction, operations, maintenance and rehabilitation of the project. Indirect economic activity is the secondary or induced economic activity that occurs as a result of the direct economic activity. An example of direct economic activity would be the employment of a construction worker, while indirect economic activity would result from that worker spending his or her salary. Another example of indirect economic activity would be a change in property values or a change in business activity along the project service area. Both of these span the entire lifecycle of the P3 and represent sources of tax revenue to the government.

Published studies that estimate the amount of direct, and indirect, economic activity created by P3s remain limited for public consumption. The authors of this paper identified and reviewed several reports which provide insightful examples into the effect of P3s as economic stimulants. A 2014 analysis commissioned by the Canadian government analyzed the economic activity of P3s over a 10-year period. 4 It noted that between 1991 and 2014, Canada instituted 206 P3 projects for a total direct spend of $63 billion (CAD). The analysis used a proprietary model to estimate the indirect economic activity resulting from P3s. Tax revenue effects were only estimated on direct economic activity and were only estimated at the national levels - the local level was excluded due to differing tax rules. The following results were found for the 2003 thru 2014 period, which represent total project costs of $51.2 billion (CAD).

As a second example, The Virginia Department of Transportation's (VDoT) Office of Transportation Public-Private Partnerships routinely estimates economic activity for P3 projects that it undertakes. The estimations are provided in briefing materials; however, the underlying methodology and models are not publicly available. Tax revenue estimates are not provided by VDoT nor can they be calculated without the models. The following economic activity was estimated for the below projects. 5

| Project | Project Cost | Jobs Supported | Economic Activity |

|---|---|---|---|

| 495 Express Lanes | $1.9 billion | 31,000 | $3.5 billion |

| 95 Express Lanes | $0.9 billion | 8,000 | $2.0 billion |

| Norfolk Midtown Tunnel | $2.1 billion | 1,700 | $8.8 billion 6 |

| Total | $4.9 billion | 40,700 | $14.3 billion |

The table above summarizes the project costs, supported jobs, and additional economic activity for a subset of P3 projects. In total, for the five projects, the economic activity is approximately three times the project costs.

We note that much of the economic activity generated by a P3 project (both direct and indirect) would likely have been generated by a traditionally-procured project through employment of a construction contractor, operations and maintenance staff, etc. This may raise the question of whether the P3 structure creates additional or incremental economic activity beyond what would have been created through traditional project delivery. Generally, this can be answered in the affirmative if a P3 has gone through a project delivery evaluation that involved VfM analysis. Without addressing specific numerical examples, we address both elements below:

Economic Activity - If the P3 delivery method is chosen based on delivering the greatest Value for Money (VfM) 7, or lowest risk-adjusted lifecycle costs, then there is reasonably expected to be incremental economic activity associated with P3 project delivery. This is because the P3 delivery is expected to lower the lifecycle cost of the asset to the public sector (including users of the asset.) This will, in turn, enable the public sector to deliver more assets or services, or to lower the overall tax/fee burden on the public, generating more disposable income or savings, and thus economic activity.

Tax Revenues - While the overall lifecycle costs are expected to be lower through a P3 that demonstrates Value for Money, it is also likely to deliver more taxes into the relevant tax bases. This is because the creation of the P3 vehicle creates an additional tax payer in the cash flow structure when compared to a conventional project delivery. This can be seen in the Exhibit C below:

|

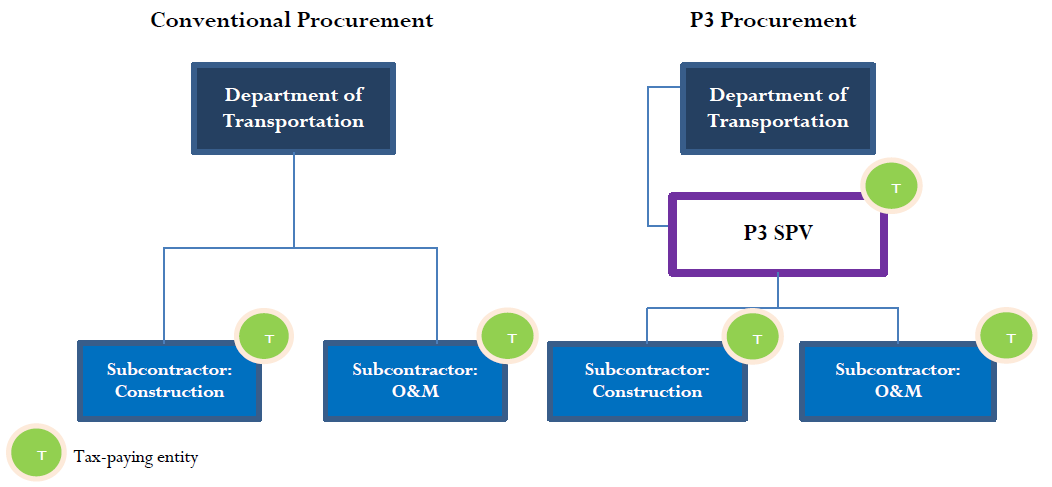

Exhibit C above shows the organization charts for a Conventional Project Delivery and a P3 Project Delivery. For the Conventional Project Delivery, the Department of Transportation (Federal or State) oversees two tax-paying subcontracting entities: Subcontractor responsible for Construction and the subcontractor in charge of Operations and Maintenance. For the P3 Project Delivery, the same Department of Transportation oversees the tax-paying P3 SPV. In turn, the P3 SPV is responsible for the activities of tax-paying subcontractors which are similar to the Conventional Project Delivery subcontractors.

Finally, we note that P3s are often pursued for the stated reasons of accelerating project delivery and ensuring certain performance and quality standards are maintained throughout the lifecycle of the project. The acceleration of the project can also be expected to result in the acceleration of the direct and indirect taxes associated with the project. In addition, while rarely modeled, the fact that the P3 does not have the same level of flexibility in deferring maintenance as a public project may also generate additional economic and tax activity during the project lifecycle.

In conclusion, we note a few key considerations for public sector sponsors of P3 projects when considering direct and indirect economic impacts of P3 projects and the resulting tax streams:

1 Additional non-tax objectives may also be achieved through use of this investment structure (e.g., legal, commercial, and financing).

2 The list of taxes with a further description does not include taxes typically used by public sector sponsors to raise funding to pay milestone, availability, or other performance-related payments.

3 Unless otherwise specified, all Section or § references are to the Internal Revenue Code of 1986, as amended, and the Treasury Regulations issued thereunder.

4 http://www.p3canada.ca/en/about-p3s/p3-resource-library/10-year-economic-impact-assessment-of-public-private-partnerships-in-canada/

5 http://www.virginiadot.org/projects/resources/SYIP/07_MPO_PDC_Presentation_P3.pdf

6 The economic benefits are estimated to be between $170 and $254 million a year when the Project starts operations in 2018. The concession will expire in 2070. Assuming 52 years at $170 million a year, $8.8 billion in constant dollars in economic activity is generated. http://www.vdot.virginia.gov/news/resources/Hampton_Roads/Midtown_FAQs_12_02_11.pdf

7 Value for Money analysis is described in greater detail in Section 4.