Consideration Of Sustainability In Pavement Design

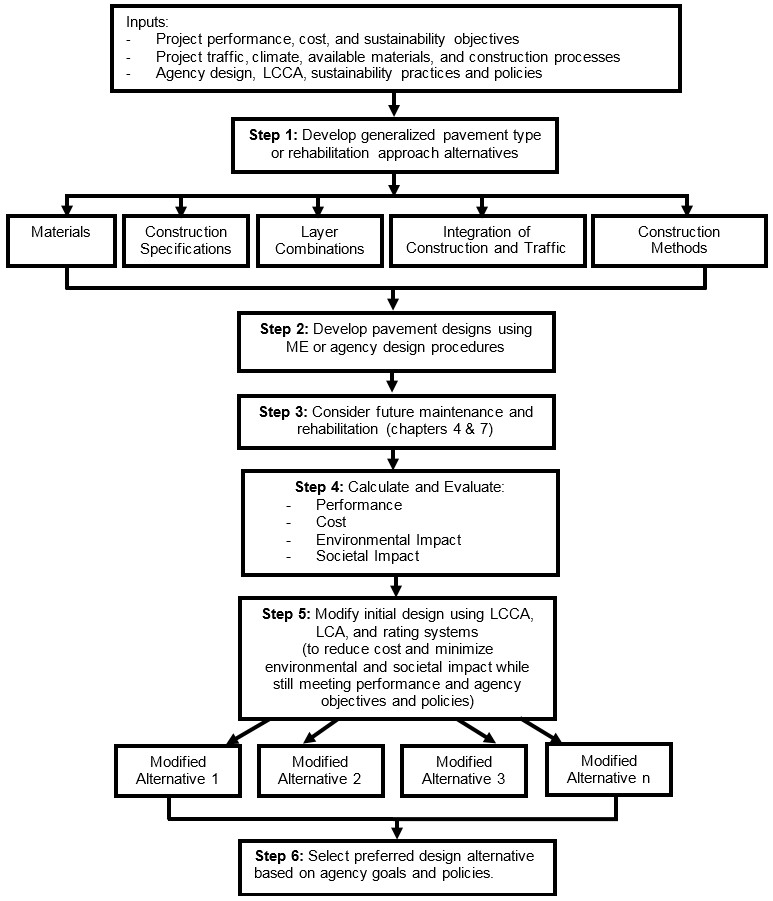

An example of an overall process for considering sustainability in pavement design is shown in figure 1. The process shown in the figure is particularly oriented towards the design-bid-build (i.e., low-bid) project delivery process.

Figure 1. Overall process for considering sustainability in pavement design.

There are numerous alternative pavement solutions that can be proposed for any set of design requirements (see Chapter 4 (.pdf) of the Reference Document for more details.) The pavement design process, whether asphalt, concrete, modular, or composite, must begin by defining the owner/agency design and policy objectives as well as any sustainability objectives. Once various pavement design alternatives have been developed, LCCA, LCA, and pavement sustainability rating tools can be applied to assess economic, environmental, and societal impacts to varying degrees as a way of improving the sustainability aspects of the proposed pavement designs. (see Chapter 10 (.pdf) of the Reference Document for more details.)

Design Objectives

An owner/agency has a number of different objectives to consider when developing a pavement design. These may be explicit objectives included in policy, may be implicit to the local agency, or may be just emerging.

Performance Objectives

The overall performance objectives used in the design process will depend on agency policies. These polices are typically developed based on a number of items, such as acceptable distress and ride quality levels and economic analyses of agency initial and life cycle costs, and may also include some types of road user costs and funding agency guidelines.

In a design-bid-build (DBB) or design-build (DB) project delivery environment, it is assumed that the design methodology will adequately predict the ability of the constructed pavement to meet the performance objectives. Some examples of performance objectives in the DBB or DB delivery environment include:

- Design life, or the number of years it takes to reach the defined end of life based on the effects of the predicted traffic loading and climatic impacts on the assumed pavement structure.

- Reliability, or the probability of reaching the design life before exceeding established distress or ride quality thresholds.

In a design-build-maintain (DBM) project delivery environment, performance objectives are explicitly written as contractual performance requirements that the contractor must deliver during the contract performance period. Some examples of performance requirements for DBM include:

- Maximum allowable IRI.

- Maximum amount of cracking or other indicators of structural deterioration.

Cost Objectives

It is common for an agency's cost objective to be to minimize the overall life-cycle cost of the pavement over a defined analysis period, or it may be to minimize the life-cycle cost while also operating within an initial cost constraint. Additional guidance on LCCA is found in Chapter 10 (.pdf) of the Reference Document, with detailed information available from the FHWA (Walls and Smith 1998). The General Accounting Office has recently reviewed a sample of state LCCA practices and provided recommendations for improvements (GAO 2013).

Sustainability Objectives

Chapter 2 (.pdf) of the Reference Document lists in detail the potential sustainability goals and objectives that are inherent as part of the pavement design process. This includes not only meeting the performance goals and cost requirements, but also minimizing environment impacts and meeting key societal needs.

References

General Accounting Office (GAO). 2013. Federal-Aid Highways: Improved Guidance Could Enhance States' Use of Life-Cycle Cost Analysis in Pavement Selection (.pdf). Report to Congressional Committees, GAO-13-544. General Accounting Office, Washington, DC.

Walls, J. and M. R. Smith. 1998. Life-Cycle Cost Analysis in Pavement Design (.pdf). Interim Technical Bulletin. FHWA-SA-98-079. Federal Highway Administration, Washington, DC.