The modification of an existing building to reduce interior noise may be carried out in several different ways with the same end result. To be able to select the most cost-effective alternative, data on noise reduction benefits and costs for each alternative must be known. The noise reduction provided by various alternatives may be determined using the procedures of Chapter 2. It is the purpose of this chapter to develop a methodology for predicting meaningful costs for each alternative.

The most meaningful basis for quantitatively analyzing alternative building modifications is to define a single number in constant dollars for the combined costs of each alternative that includes the time value of money.

Costs incurred immediately are more significant than costs incurred in later years because of interest, which is the cost involved in the use of money. Interest must be considered on all funds in use, since the selection of one alternative necessarily commits money which otherwise could be invested in another opportunity. Some method must therefore be used to adjust cost figures on the basis of the year in which they occur. The process we shall use in this manual is referred to as discounting with a representative discount rate of 10 percent. We will primarily be concerned with Initial Investment Costs (IC) which are those immediate costs necessary to effect an alternative and Replacement Costs (RC) which occur each time the original modification must be replaced.

The current value of money is called its Present Value (PV). Present value is the sum of anticipated future cash outflows (or inflows) discounted back to the current date at the appropriate interest rate.

The first step in any cost analysis is to decide what time frame will be utilized. The most accurate choice would be the remaining economic life of the structure. This is the period over which improvements to real estate contribute to the value of the property. For the purposes of this manual, 30 years will be used as a time frame for the analysis.

Table 20 is an annual compound interest table (based on an effective discount rate of 10 percent) to be utilized for calculating the discounted PV of Replacement Costs. To simplify PV calculations of replacement costs, the factors listed in the Table for the appropriate replacement years should be added and then multiplied by the initial investment. For example, for our assumed 30-year analysis of an alternative which requires replacement every 10 years, the factors for years 10, 20, and 30 (the years in which replacement occurs) would be added (.386 +.149 + .057 = .592). If the initial investment is $1,000, the present value of replacement costs is $1,000 x .592 = $592.

| Alternatives | |||

|---|---|---|---|

| X | Y | Z | |

| Initial Investment | $500 | $750 | $2,000 |

| Replacement Costs | $500 (every 5 yrs) | $750 (every 15 yrs) | $2,000 (every 30 yrs) |

| Years | Factors for RC |

|---|---|

| 1 | .909 |

| 2 | .826 |

| 3 | .751 |

| 4 | .683 |

| 5 | .621 |

| 6 | .564 |

| 7 | .513 |

| 8 | .467 |

| 9 | .424 |

| 10 | .386 |

| 11 | .350 |

| 12 | .319 |

| 13 | .290 |

| 14 | .263 |

| 15 | .239 |

| 16 | .218 |

| 17 | .198 |

| 18 | .180 |

| 19 | .164 |

| 20 | .149 |

| 25 | .092 |

| 30 | .057 |

*For discount rates other than 10%, see Ellwood, L.W. Ellwood Tables for Real Estate Appraising and Financing, Third Ed., Chicago: American Institute of Real Estate Appraisers (1974).

| Alternatives | |||

|---|---|---|---|

| Cost Category | X | Y | Z |

| IC | $500 | $750 | $2,000 |

| RC (from Table 20) | $500 (.621 +.386 +.239 +.149 +.092 +.057)= $772 | $750 (.239 +.057) = $222 | $2,000 x .057 = $114 |

| Total PV | $17272 | $972 | $2,114 |

When the Initial Costs and Replacement Costs of each alternative are added, it is found that Alternative Y has the lowest Present Value.

In addition to Initial Investment and Replacement Costs, Operating Costs, OC, of Noise Reduction modifications should be considered where appropriate. Once the operating costs of a modification are determined, the Present Value of these costs should be calculated by multiplying the value of the annual OC by the factor 9.427. This factor is based on our assumed 30-year analysis.

Unit cost data (hourly labor rate, cost per square foot) can be obtained from many sources, depending on the degree of detail required. The data sources utilized must permit a cost estimate under current, local market conditions. Three particularly valuable data sources are described below.

These represent a very significant source of cost data since they are constantly in touch with the market. They can provide data on wage rates, materials and equipment prices, and categories of indirect costs. In particular, they are important sources of cost differentials for different types of structures.

The use of a professional cost estimator might be necessary for highly specialized structures.

These provide detailed unit costs for structural components and items of equipment. Three such national services are listed in Table 21. These services publish monthly or quarterly supplements to bring cost studies up-to-date with new construction methods and materials, and to provide area and time adjustment factors in index form so that the base figures can be utilized in the local market area.

Boeckh Building Cost Manual. Milwaukee: Boeckh Division, American Appraisal Co., 1967. Vol. I: "Residential and Agricultural," Vol. II: "Commercial," Vol. Ill: "Industrial and Institutional." Monthly Building Cost Modifier. Dow Building Cost Calculator and Valuation Guide. New York: McGraw-Hill Information Systems Co., quarterly. Marshall Valuation Service. Los Angeles: Marshall and Swift Publication Co., Monthly. |

|---|

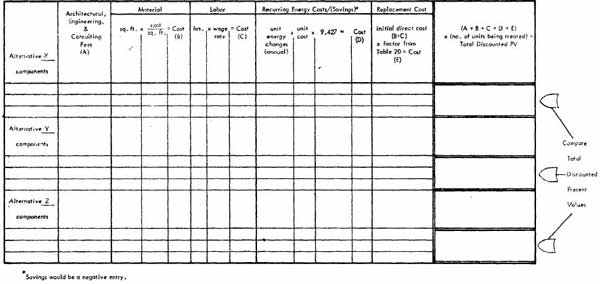

Cost worksheets provide a convenient checklist to ensure that all necessary and appropriate elements of cost are included in the final estimate of Noise Reduction costs. Direct costs will consist of labor and materials. The primary category of indirect costs includes architectural, engineering and consulting fees. Operating costs (or savings) result from increased mechanical ventilation costs and heat energy savings.

Figure 16 shows a worksheet format for deriving cost estimates. This enables an equitable comparison of alternatives by formulating a single total cost for each alternative.