U.S. Department of Transportation

Federal Highway Administration

1200 New Jersey Avenue, SE

Washington, DC 20590

202-366-4000

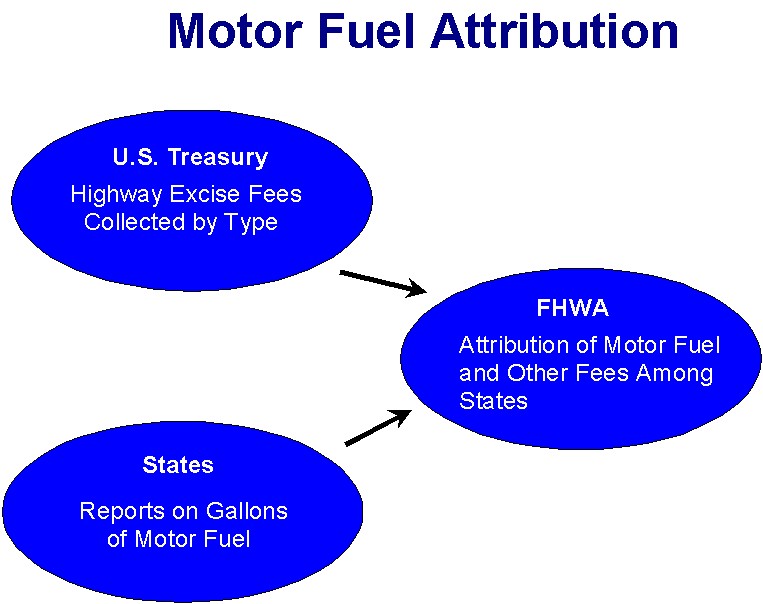

Each year, highway users pay billions of dollars in highway excise taxes, which end up in the federal Highway Trust Fund. While motorists pay these taxes as they purchase the various taxed items, the US Department of Treasury actually collects most of these taxes from large corporations located in a handful of States and deposits the receipts into the Highway Trust Fund. Federal legislation generally requires that funds paid into the Highway Trust Fund, be returned to the States for various highway program areas in accordance with legislatively established formulas. Each State is guaranteed that at least 92% of its highway user percentage attributions to the Highway Account of the Highway Trust Fund will be returned to the State. Since contributions by the highway users in each state cannot be directly measured, procedures have been developed to attribute funds to the States.

The Highway Trust Fund includes a Highway Account and a Mass Transit Account. The Highway account is the primary source of revenues for Federal-aid funding returned to the States for carrying out various highway programs. Formulas for distributing Federal-aid highway funds for the Surface Transportation Program, the National Highway System, and for Interstate Maintenance use motor fuel and other excises attributed to each state as distribution factors. Given the large amounts of funds involved in these programs, the accuracy of the attribution process is critical. What Steps Are Needed to Attribute Receipts? The U.S. Department of the Treasury provides to FHWA documentation of the actual revenues received, by type of highway fee, into the Highway Account of the Highway Trust Fund. The states provide reports to FHWA on the gallonage of motor fuel recorded and taxed in each state, by type of fuel. FHWA, in cooperation with the states, has developed procedures to attribute revenues. The FHWA analyzes the State generated data and develops the final attribution estimates for the states based on the state data.

Net Highway Account Revenues for 2010 have been estimated as follows by source:

| Fee Category | Amount ($ Millions) |

|---|---|

| Gasoline | $20,320 |

| Diesel and Special Fuel | $7,063 |

| Truck and Trailer Sales | $1,562 |

| Truck Tires | $318 |

| Heavy Vehicle Use | $887 |

| Interest and Other | $14,742 |

| TOTAL | $44,892 |

The Treasury Department collects federal excise taxes. Most federal highway user taxes are not collected directly from the highway users in each state, since most collections are from large corporations. The Treasury Department lacks information which allows the attribution of the taxes to highway users in each state. The only fee collected directly from users is the federal heavy vehicle use tax. However, this is paid by the vehicle owner, and the address of the vehicle owner is not equivalent to where the vehicle is used. The Treasury Department estimates all of the Highway Account receipts by type, and provides this information to the FHWA. There is a time lag in this reporting, and the Treasury Department may revise its estimates of the fees collected before announcing a final certified amount.

The FHWA and the states have developed a set of procedures for allocating Highway Account revenues to the highway users in each state. The attribution relies on state reports of the consumption of each type of motor fuel: gasoline, gasohol, special fuels (mostly diesel), and other alternative fuels. States report on fully taxed fuels, exempt sales, partially exempt sales, full and partial refunds, and fuels taxed at reduced rates. Attributions are made separately for gasoline and gasohol, based predominantly on the state reports. FHWA includes government use of gasoline in gasoline attributions, but excludes government use of diesel fuel in diesel attributions. There are federal fees assessed on heavy vehicles which are not fuel taxes. These include a tax of 12 percent on the retail prices of truck sales for vehicles with over 33,000 pounds gross vehicle weight, and for truck trailer sales of over 26,000 pounds gross vehicle weight; a graduated tax on heavy tires of 15 cents per pound over 40 pounds, plus 30 cents per pound over 70 pounds, plus 50 cents per pound over 90 pounds. A heavy vehicle use tax is applied to trucks of 55,000 pounds and over gross vehicle weight, at $100 plus $22 dollars per 1,000 pounds in excess of 55,000 pounds, with a maximum of $550 per truck. These non-fuel based fees are attributed to the states in the same proportions as special fuels are attributed to the individual states.

Because of differences in State legislation and administrative procedures, the data collected and submitted to FHWA by states differ. State agencies which originally collect the information may not be the State Departments of Transportation. FHWA must make adjustments to the state motor fuel data to account for public use of gasoline, gasoline losses, and special fuels used off highway and for public uses. FHWA has developed a series of models to account for these factors as equitably as possible among the states.

As a result of its own reassessment of motor fuel reporting, FHWA has developed an action plan to improve the accuracy of the motor fuel data.This action plan was implemented over the years 2001 and 2002, and includes improved documentation, improved data tools, stronger process oversight, and possible use of the Treasury Department's new fuel tracking system, the Excise Files Information Retrieval System (EXFIRS) as a verification tool. For further information about the attribution of revenues, please contact the FHWA Division Office in your state.

For more information contact Ralph.Erickson@fhwa.dot.gov or phone 202 366-9235.