Developer Contributions - One-time charges collected by local governments from developers to offset the cost of infrastructure and services necessitated by new development.

Special Assessments - An additional fee or tax assessed on businesses or residents in specified geographic areas benefiting proximity to a highway or other transportation facility or corridor.

Fees - Similar to a utility fee, transportation fees are assessed based on how individual businesses and households use transportation facilities.

* Incremental Growth - A mechanism allocating back to infrastructure from some specified portion of increased property tax revenues fostered by new infrastructure - often for a specified period of time.

Joint Development - Sale or lease of land or air rights on or adjacent to transportation facilities. This can include donations of land or other in-kind resources from the private sector in ongoing commercial operations.

Concessions - Sale or lease of government owned assets - such as toll roads or bridges - to private-sector investors/operators.

Advertising and Naming Rights - Sale of advertising space or naming rights on a transportation facility. Note: Commercial uses within Interstate Highway System right of way, including rest areas, is prohibited by law; however, they may be allowed on toll facilities and in transit stations.

* Topic of this webinar

Outline of Presentation

Tax Incremental Finance Overview

Why is There a Need for Incremental Revenues?

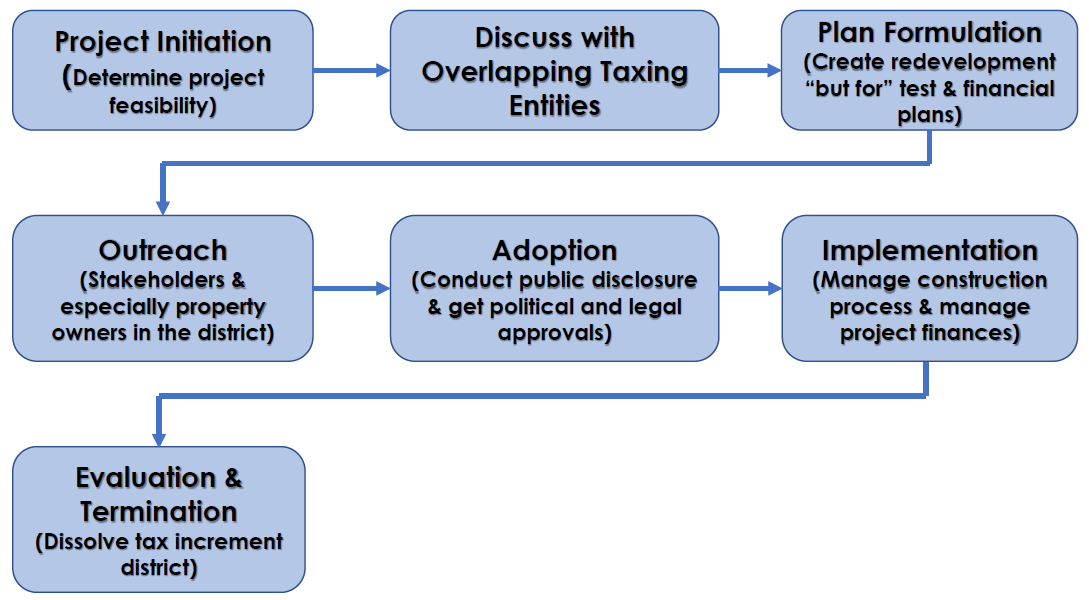

Process to Create a TIF District

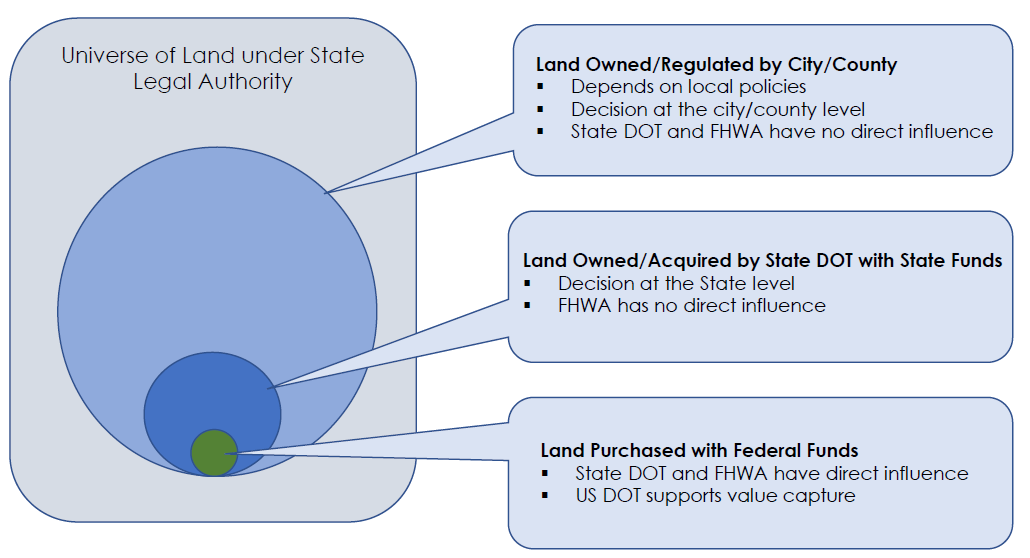

Federal Roles

Case Studies

Q&A

Tax Incremental Finance Overview

Glossary of Terms

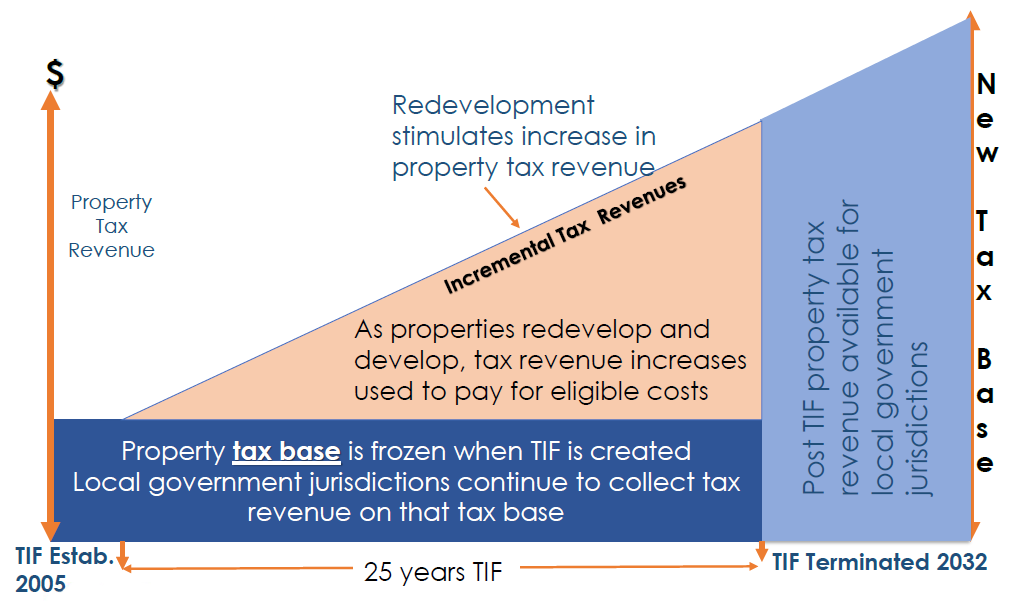

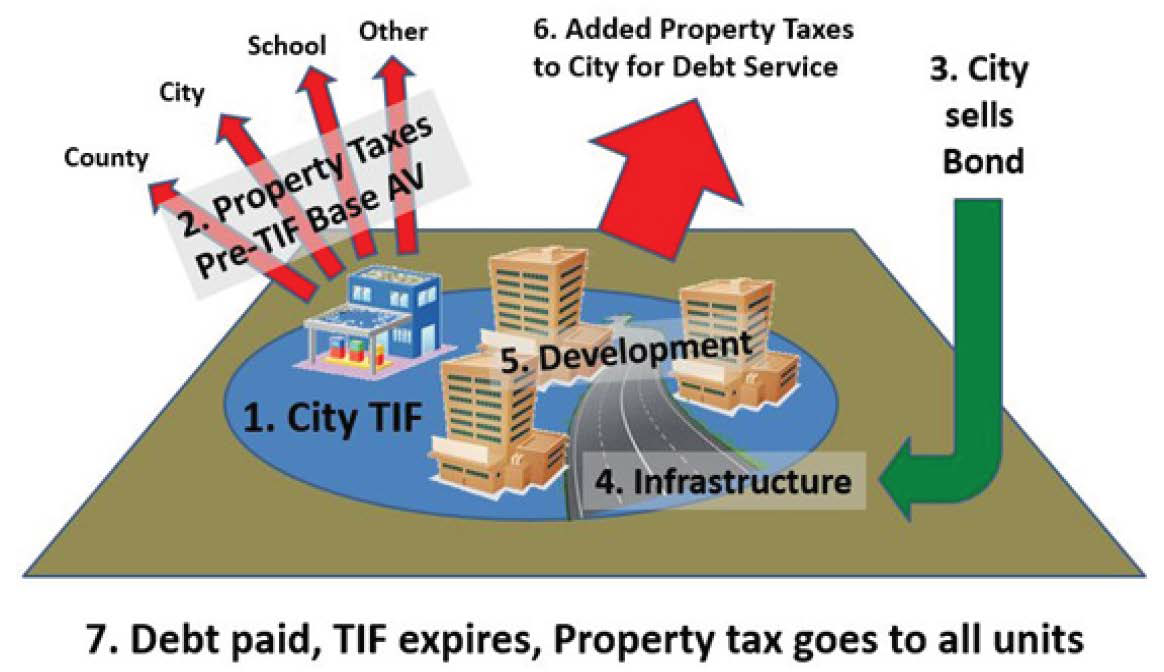

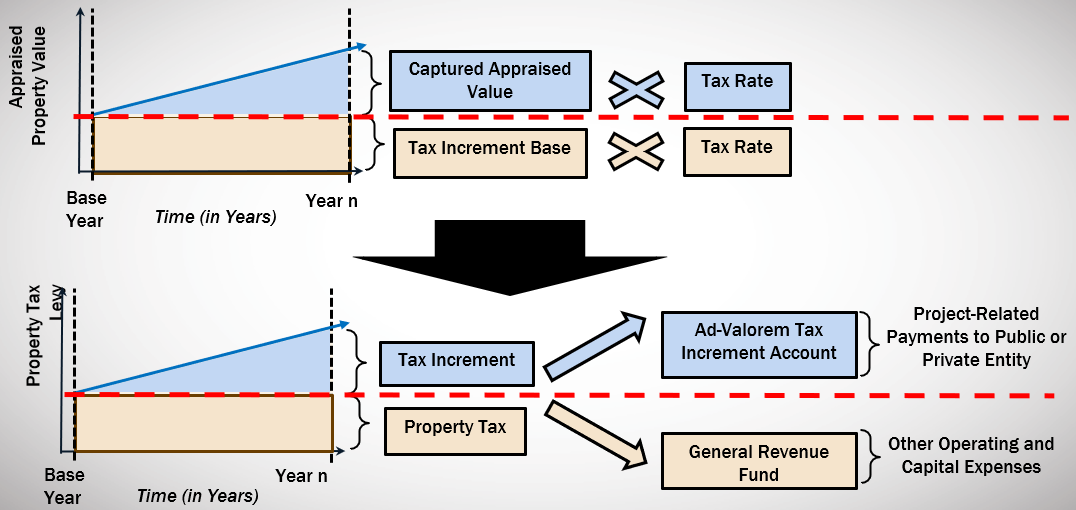

Tax Incremental Financing (TIF): a revenue/funding tool available to local authorities to encourage economic development that would not occur without public assistance.

A Tax Increment District (TID): the contiguous geographical area within a municipality consisting solely of whole units of property that are assessed for general property tax purposes.

"Blight" - The legal term "blight" describes a wide array of urban problems, which can range from physical deterioration of buildings and the environment, to health, social, and economic problems in a particular area.

Neighborhood blight and the presence of vacant and abandoned properties have profound negative impacts on afflicted communities. Blighted properties decrease surrounding property values, erode the health of local housing markets, pose safety hazards, and reduce local tax revenue.

A revenue tool that captures and uses increased property tax revenues from new development within a defined geographic area to fund public infrastructure

Available in 49 of 50 states and the District of Columbia

Represents the new tax revenues generated from new development properties within the Tax Incremental District and are split into two components:

Base Revenues

Incremental Revenues

Incremental Revenues Financing Tools

Pay-as-you-go financing: expenditures are undertaken as incremental revenue is realized

Developer financing: Local reimburses the developer for TIF-eligible costs as it obtains incremental revenues

Municipal financing:

Revenue bonds & general obligation

Taxable revenue bond

Municipal financing with developer participation: Local authority issues bonds while the developer simultaneously pledges to purchase all or a significant portion of bonds

What is the Need for Value Capture: Tax Increment Financing?

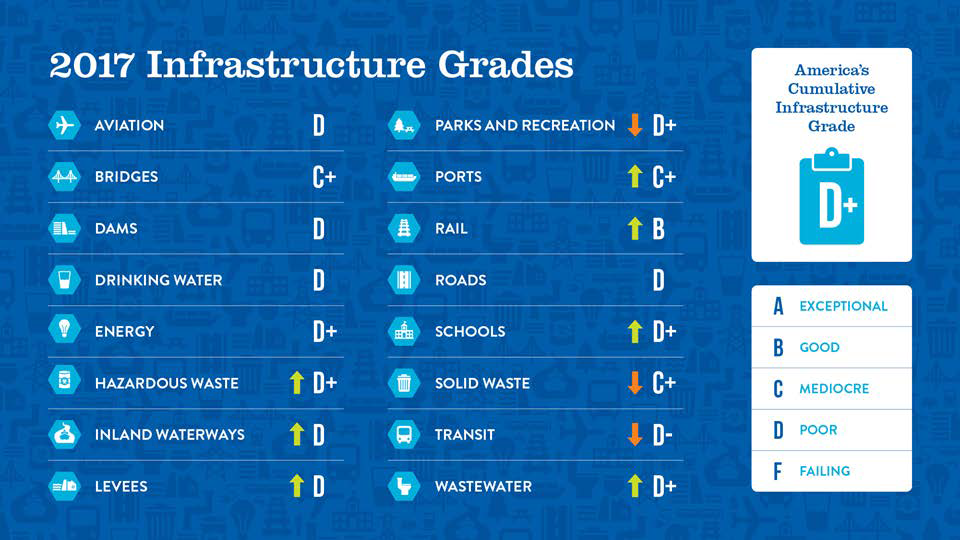

Infrastructure Crisis

National Highway System Conditions (ASCE 2017)

One out of every 5 miles of highway pavement is in poor condition

8% or 47,000 bridges rated in poor condition

43% or 260,209 bridges are over 50 years old

$836 billion backlog of highway and bridge capital needs

The fundamental purpose of TIF is to attract investment to an area in which little or no new development or growth would take place without the use of the TIF

This is sometimes called the "but for" test - no growth/development would happen but for the use of TIF

TIF District Maintenance

Annual TIF audited reports

Update district database to provide information for interested parties

On-going monitoring and continuing disclosure requirements

Investor quarterly reports

Termination of Tax Incremental Finance District

Reach the end of maximum Tax Incremental Finance District statutory life (25-30 years)

A TIF District may be terminated by a resolution from the municipality's government

The Department of Revenue must be notified

A final accounting report (audited financial statement) must be completed

Challenges: Community Buy-In

Redevelopment and economic development do not happen in a vacuum, and the process can be highly political

Diversion of tax dollars for private development can be controversial

Raises policy questions regarding the proper role of government

Issuance of "public" debt for "private" development can be unsettling

Tax revenue "diverted" from other municipal services

Thay Bishop, FHWA Center for Innovative Finance Support, OIPD

Stefan Natzke, FHWA Office of Planning, Environment, and Realty

Members

Jennifer Ahlin, Virginia Department of Transportation

Janine Ashe, FHWA District of Columbia Division

David Cohen, FHWA Office of Project Development & Env. Review

John Duel, FHWA Office of Planning, Environment, and Realty

Kathleen Hulbert, FHWA Infrastructure Office

Andrea Kirk, FHWA Center for Local-Aid Support, OIPD

Chip Millard, FHWA Freight Management & Operation

Diane Mobley, FHWA Chief Counsel Office

Kevin Moody, FHWA Resource Center

Ben Orsbon, South Dakota Department of Transportation

Jill Stark, FHWA Office of Planning, Environment, and Realty

Lindsey Svendsen, FHWA Office of Planning, Environment, and Realty

Jim Thorne, FHWA Office of Planning, Environment, and Realty

Bingxin Yu, FHWA Transportation Policy Studies

VCIT Focus Areas

Communication - Developing the tools to help FHWA staff and others promote Value Capture to local public agencies (Value Capture Implementation Manual)

Technical assistance - Providing technical assistance to local public agencies interested in pursuing Value Capture (Peer Program)

Clearinghouse (website) - Identification of best practices and lessons learned and promoting further discussion on innovative funding options for local public agencies, lessons learned from past and current efforts, etc

Value Capture Implementation Manual

1. Introduction

2. Assess Funding Options and Need for Value Capture

3-8. Select Appropriate Value Capture Technique

9. Develop Business and Economic Case and for Stakeholders

OUR VISION IS TO MAKE ATLANTA THE MOST ECONOMICALLY DYNAMIC AND COMPETITIVE CITY IN THE WORLD.

OUR MISSION

TO ADVANCE ATLANTA'S GLOBAL COMPETITIVENESS BY GROWING A STRONG ECONOMY, BUILDING VIBRANT COMMUNITIES AND INCREASING ECONOMIC PROSPERITY FOR ALL ATLANTANS.

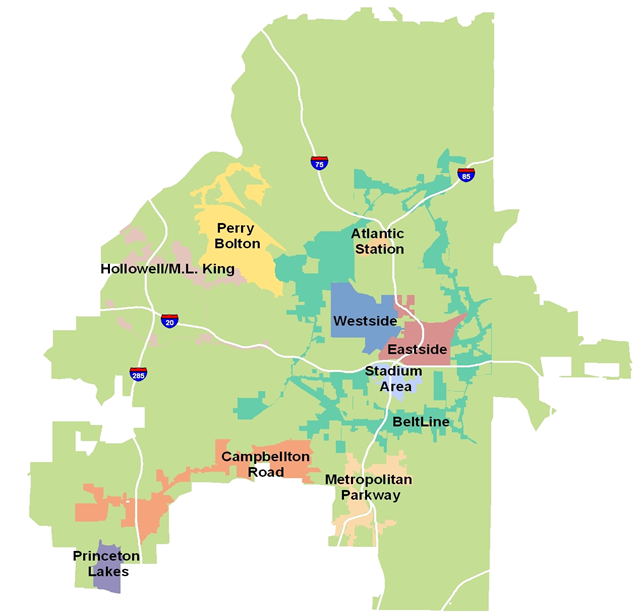

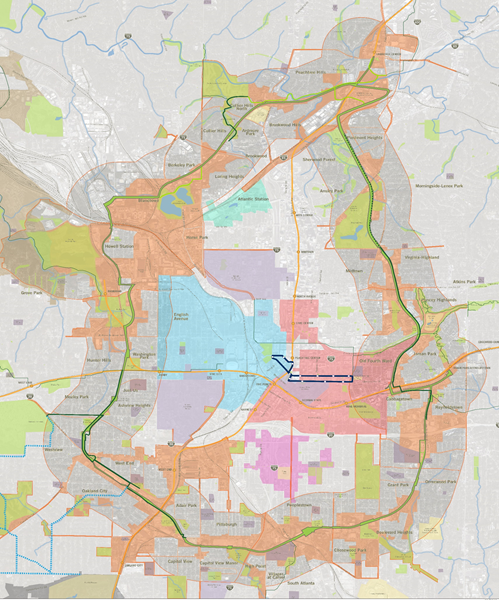

Tax Allocation Districts and Corridors

Atlanta's Tax Allocation Districts

Westside (1992/1998 expanded)

Atlantic Station (1999) - All proceeds pledged to debt repayment. No new projects

Princeton Lakes (2002) - All proceeds pledged to debt repayment. No new projects

Perry Bolton (2002)

Eastside (2003)

Atlanta BeltLine (2005)

Campbellton Road (2006)

Hollowell/ML King (2006)

Metropolitan Parkway (2006)

Stadium Area (2006) 3

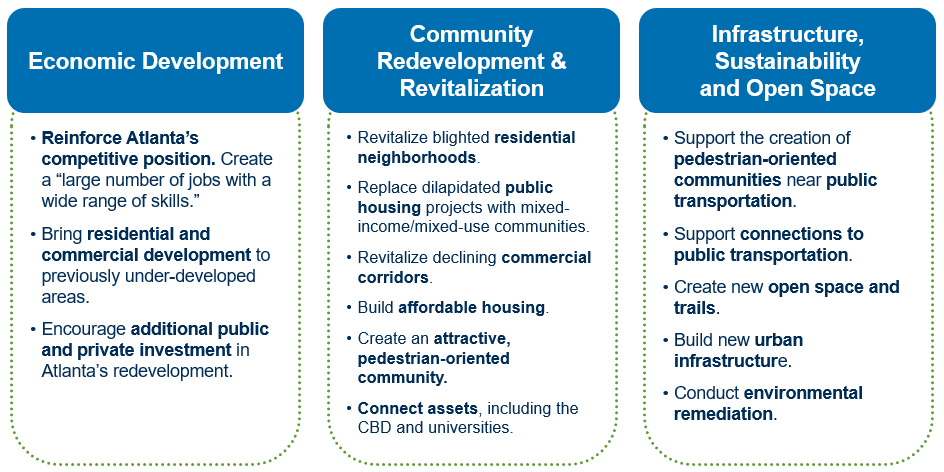

Objectives of Atlanta's TAD Program

Each TAD was establishedwith a redevelopmentplan that addresses specific challenges.

Reinforce Atlanta's competitive position. Create a "large number of jobs with a wide range of skills."

Bring residential and commercial development to previously under-developed areas.

Encourage additional public and private investment in Atlanta's redevelopment.

Community Redevelopment & Revitalization:

Revitalize blighted residential neighborhoods.

Replace dilapidated public housing projects with mixed-income/mixed-use communities.

Revitalize declining commercial corridors.

Build affordable housing.

Create an attractive, pedestrian-oriented community.

Connect assets, including the CBD and universities.

Infrastructure, Sustainabilitt abd Open Space:

Support the creation of pedestrian-oriented communities near public transportation.

Support connections to public transportation.

Create new open space and trails.

Build new urban infrastructure.

Conduct environmental remediation.

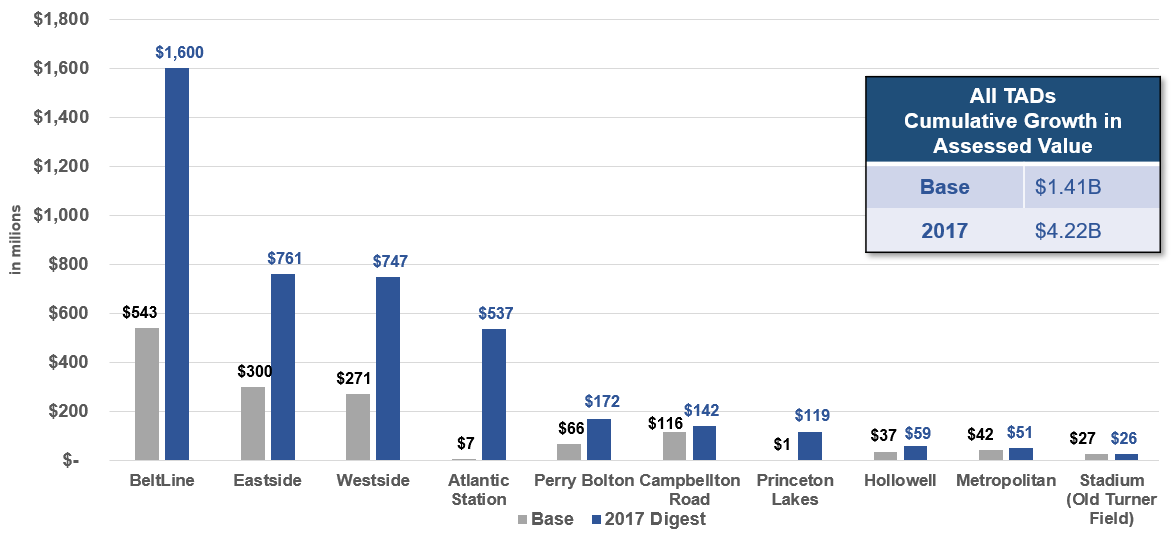

TAD Success Stories

TAD funding has been utilized to develop a wide array of residential, office, retail, hotel, and public amenity projects.

Usage: TAD bonds and incremental tax revenues have been committed to or already provided gap funding to leverage over $9.0 billion in private development.

Projects: TAD bonds and incremental tax revenues have helped fund or have been committed to:

Over 12 million square feet of new residential development, producing over 12,000 units, more than 20% of which are affordable

Over 7 million square feet of new commercial development, including hotels, stores, office buildings and a film production studio.

The TAD program has also helped to fund two fire stations, several community and educational facilities, open space and trail projects, and infrastructure improvement projects.

Since the creation of each TAD, the cumulative increment in assessed value for all TADs is $2.81B.

Atlanta Beltline

Atlanta BeltLine, Inc. (ABI) was created in 2006.

ABI is managing the planning, design and implementation of all aspects of the project.

+/- 3,000 acres of underutilized land along the corridor will become available for public and private redevelopment opportunities.

Funding for the Atlanta BeltLine project comes from a combination of federal, state, local, and private sources.

Atlanta Beltline & Transit

A Coordinated Approach

Two major efforts are underway to advance transit on the Atlanta BeltLine: the More MARTA program and federal NEPA studies. These support the Atlanta Streetcar System Plan (SSP), which focuses on connecting neighborhoods to key destinations and activity centers. The SSP is a supplement to the City's Connect Atlanta Plan and works in tandem with Atlanta BeltLine, Inc.'s Strategic Implementation Plan (SIP).

More MARTA

16 projects throughout the City of Atlanta will be funded through the More MARTA sales tax. This includes approximately $1.2 billion in funding for Atlanta BeltLine transit projects.

The Big Picture

The plan calls for 50 miles of new streetcar routes and 12 miles of connected transit, which includes investment in other forms of public transportation to provide additional connectivity to the streetcar system. The SSP was adopted by the Atlanta City Council on December 8, 2015.

Atlanta Beltline Challenges

AFFORDABLEHOUSING

EQUITY & INCLUSION

DISPLACEMENT

INVEST ATLANTA

Thank you

Presentation 3

Incremental Growth Techniques:

Transportation Reinvestment Zones

Federal Highway Administration EDC-5 Value Capture Webinar

August 22, 2019

Outline

Introduction and Background

The Texas TRZ

Evolution of the TRZ Legal Framework

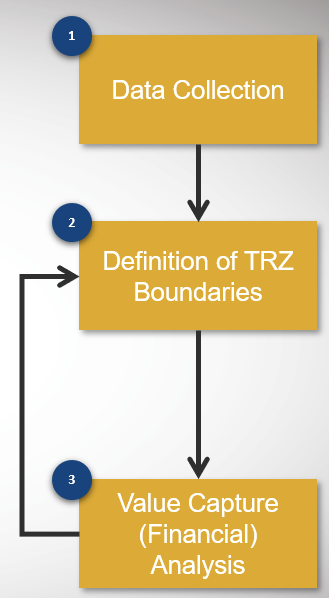

The TRZ Implementation Process

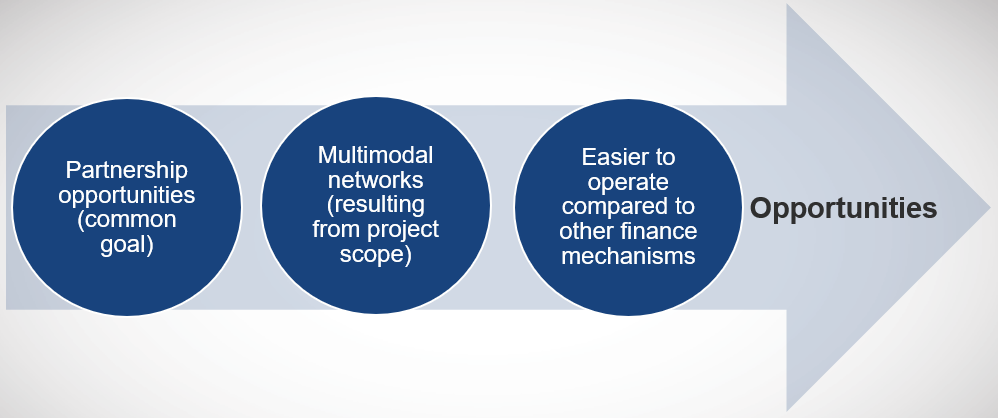

Opportunities and Limitations

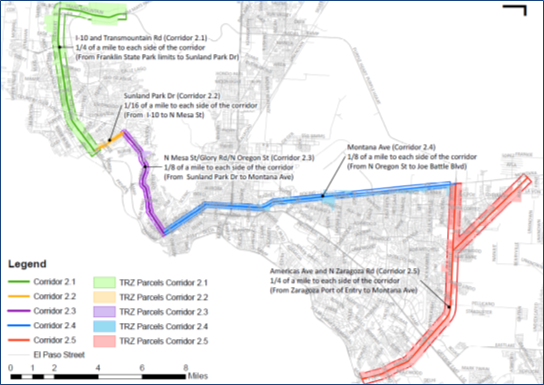

Active Texas TRZs

Introduction

Funding Transportation Needs

Creative Thinking

Doing more with less

Alternative Funding sources

Texas Legislature SB 1266 (2007) Created TRZs

14 Local TRZs Since 2007

Background

Types of Value Capture Mechanisms used in Transportation #1 of 2

Mechanism

Definition

Applicable Purpose

Examples (State)

Impact

Fees (IF)

One-time charge

Local governments collect from developers to finance new infrastructure and services for new development.

Cost recovery

Transportation System Development Charges

In OR used to fund existing

and new capacity

Also used in WA and NJ

Special Assessment District (SAD)

Additional fee on properties benefiting from proximity to a new facility

District vote is needed

Projects require district vote

Capture of project expansion benefits

VA and OH (Downtown Improvement Districts),

IL Special Service Areas

Sales Tax District (STD)

Type of SAD requiring project beneficiaries to pay limited sales tax instead of property tax

Capture of project expansion benefits

IL Special Service Areas;

MO and KS Transportation DD

Negotiated Exaction (NE)

One-time charge similar to IFs but not requiring a formal process

Example: in-kind contributions to local infrastructure (roads, parks, etc.) for development approval

Capturing opportunity for value creation and cost recovery

VA proffer

Joint Development (JD or P3)

Development of a transit facility and adjacent private real estate

Private partner provides facility or makes financial contribution to offset construction costs

Capturing opportunity for value creation and cost sharing and revenue sharing with private sector

Massachusetts Turnpike (MA) and Washington Metropolitan Transit Authority (VA)

Air Rights (AR)

Form of JD

Dev. rights above or below infrastructure facility used to generate / capture incremental increase in land value

Capturing opportunity for value creation and cost sharing and revenue sharing with private sector

Massachusetts Turnpike (MA) Interstate 5 (WA)

Land Value Tax (LVT)

Tax imposed on land value benefiting from infrastructure

Capture of project expansion benefits

Pennsylvania counties (PA)

Transportation utility fees (TUFs)

Utility fees assessed on characteristics more closely related to transportation demand than property taxes

Cost recovery: operating and maintenance costs

Oregon TUF for pavement maintenance (OR)

Tax increment financing (TIF)

Mechanism to allocate any increase in total property tax revenues toward public investment within a designated district

Capture of project expansion benefits

TRZs (TX)

The Texas TRZ - Definition

Texas TRZs

Designated contiguous zone around a planned transportation improvement where properties are expected to benefit from the project through land development, value increases

Legal arrangement to facilitate value capture via the property and sales tax mechanism and allow the local government to use incremental tax revenue as collateral

Texas TRZs are not a new tax

Tax rates do not change

Revenue realized only if real property develops / increases in value

TRZs Expedite Transportation Projects

Local match contributions

Multiple funding sources leveraged

TRZ Legal Framework Has Evolved

Process / requirements clarified

Uses / types modified or expanded

Three TRZ Types

Municipal

County

Port Authority

The Texas TRZ - How it Works

The Texas TRZ - Financing Options

Three Financing Options Available for TRZ Revenue Funds

Type

Form

Advantage

Disadvantage

Pay-as-you-go

Expenditure within the budget limit

No financial cost

Slow/late delivery due to capital constraints

Municipal bond financing

Public financing from capital markets

Earlier availability of capital

Flexibility to finance different project types

Higher transaction costs

Higher financial (interest) costs

State Infrastructure Bank (SIB)

Long-term debt from the state

Earlier availability of capital

Lower transaction, (interest) costs

Competition with other local governments

Federalization: added time and cost

Restrictions on financing of projects off the state system

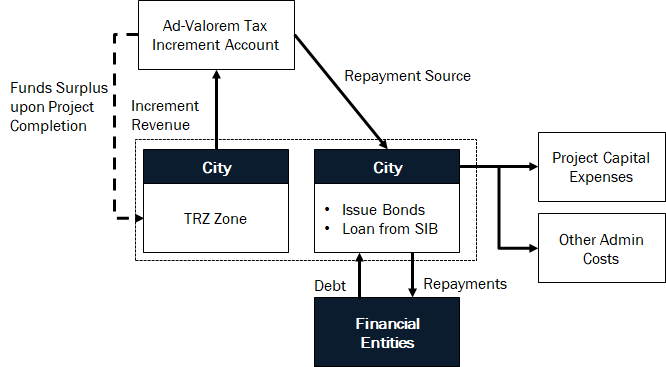

The Texas TRZ - How Funds Flow

Bond and SIB Loan Financing

Start: Public entity borrows money with TRZ revenue as collateral.

Construction: Government starts construction

Operation: Government repays debt using tax increment