U.S. Department of Transportation

Federal Highway Administration

1200 New Jersey Avenue, SE

Washington, DC 20590

202-366-4000

Highway-related finance data is the focus of Chapter 2. Chapter 2 provides guidance for completing FHWA 500-Series forms related to highway finance: FHWA Form 531 – Revenues; FHWA Form 532 – Expenditures; FHWA Form 541 – Obligations Issued; FHWA Form 542 – Transportation Debt; FHWA From 536 – Local Highway Finance; and FHWA Form 534 – Capital Outlay and Maintenance Expenditures.

Section 2.1 covers revenues generated from taxes, tolls, and other charges levied on fuel, vehicles, and highway users, as well as transfers of revenue between different levels of government. Section 2.1 also covers receipts and outlays from the highway and transit accounts of the Federal HTF and their annual opening and closing balances.

Section 2.2 covers debt obligations used to finance highway facilities, including total outstanding obligations at the beginning and end of each year, as well as changes resulting from new debt issues, retirement of outstanding obligations, and refunding of existing debt.

Section 2.3 covers the reporting of financial information for State and local toll facilities.

Section 2.4 covers the Local Highway Finance Report, which summarizes the funding of highways by local governments. Local governments include counties, townships, municipalities, special districts, and other general-purpose authorities.

Section 2.5 covers the capital outlay and expenditures for highway purposes report.

See sections 2.1 through 2.5 for guidance on completing the highway finance–related forms.

Fuels and FASH conducts certain validation tests when a State submits a form. Then it generates a report showing (1) the total percentage change over the past 3-year period and (2) a line graph for the 3-year period. The report highlights data that shows questionable trends from one year to the next. Fuels and FASH prompts the State to view the graphs and reports and to return to the form for editing if data variances are outside of normal trends.

Using the 3-year data reports generated by Fuels and FASH, the State should compare the current data with the previous year’s data, and if there is a significant increase, decrease, or other anomaly, the State should investigate to identify the reason. If the State finds a legitimate reason for a large difference from the previous year’s data, it should add a comment justifying the difference. Otherwise, the State should return to the data sources to rectify the issue with the data.

After a State submits a form, an FHWA analyst reviews the form, examining the Fuels and FASH data quality report and reading the State’s comments and justifications. The FHWA analyst may ask the State for more information. After this review, the analyst may accept or reject a form. The following reasons could lead to a form being rejected:

The FHWA analyst performs an in-depth review of all State forms for quality control; FHWA staff may request additional information or corrections if the review finds erroneous data, and States can go back to edit the form to explain the figures.

With the exception of a few components of the motor fuel and vehicle registration data, the FHWA does not adjust State-reported 500-Series Data.

FHWA Form 531, State Highway Income, reports a State government’s revenue from highway users and others. This revenue funds the State’s highway and mass transit programs.

FHWA Form 532, State Highway Expenditures, reports the State government’s highway and mass transit–related expenditures and any non-transportation distribution from highway user revenues.

FHWA Form 531 and FHWA Form532 forms together are intended to provide an annual cash flow statement in which major revenue sources and major expenditure items for highway and mass transit purposes are identified. They provide a balanced statement of all funds controlled or administered by State agencies that perform highway program-related functions.

This section describes how to complete FHWA Form 531 and FHWA Form 532 forms.

State DOTs are ultimately responsible for the submission of FHWA Form 531 and FHWA Form 532 forms to FHWA. Different States have different organizational structures, but typically, the State finance, budget, or accounting division of the State DOT is responsible for collecting the highway program income and expenditure data. In some States, however, a non-DOT agency such as a Department of Revenue is responsible for collecting the data.

If the State DOT relies on other offices and agencies for the data required for FHWA Form 531 and FHWA Form 532 forms, it should ensure that their processes for data collection meet FHWA’s reporting requirements. Coordination among agencies to establish processes for translation or transformation of data may be necessary to meet FHWA reporting requirements.

The relevant FHWA division office should coordinate with State agencies to identify the agencies, offices, and personnel responsible for data collection, preparation, and quality control. The division offices assign a state Sponsor to provide coordination among agencies for the preparation of data for FHWA.

Absence of coordination among State agencies may affect data quality and timeliness; staff turnover and retirement can disrupt established processes and affect data quality and timeliness. State agencies should document their procedures for data collection, analysis, and reporting to ensure the transfer of this essential knowledge when staff leave an agency. Proper documentation and knowledge transfer flatten the learning curve for new staff and reduce knowledge gaps that could lead to the reporting of erroneous data.

The State DOT should notify FHWA Office of Highway Policy Information of the contact information of the staff responsible for data preparation, which includes the person’s name, position title, office or agency name, email address, and phone number.

Reporting for FHWA Form 531 and FHWA Form 532 forms should include all State agencies with highway and mass transit functions—not only the DOT, but also highway departments or agencies such as department of public safety and department of public works), State police or State highway patrol, toll authorities, quasi-State and multi-State agencies, and others.

FHWA division offices coordinate with State agencies to identify the agencies, offices, and personnel responsible for data collection, preparation, quality control, and submission. Some division offices form user groups to encourage coordination among agencies in preparing data for FHWA.

FHWA Form 531 and FHWA Form 532 forms are required to be completed and submitted annually. For reporting purposes, States must assemble data in accordance with their agencies’ budget periods and cycles—on either a calendar year basis or a fiscal year basis.

FHWA Form 531, FHWA Form 532, FHWA534, FHWA541, FHWA542 forms must be prepared for the same time period.

States may have to give special consideration to certain uncommon issues in compiling data, or they may have unique circumstances in the collection and reporting of finance data. The following gives States more information about how to handle some of these circumstances.

FHWA Form 531 and FHWA Form 532 forms are designed to accommodate the accounting transactions of State DOTs and other State agencies that have highway or mass transit functions. Highway and mass transit–related activities of State agencies such as parks, boards, conservation commissions, departments of public safety, State police and highway patrol, governor’s office of highway safety, motor vehicle departments, special toll (or free road) authorities, and State bond commissions should be reported.

In some States, aid to local governments for highway purposes is derived from Federal shared revenues or from State taxes, fees, or appropriations (other than road user taxes) that do not pass through State DOT accounts. Any Federal or State funds known to have been distributed to local governments for highway activities during the year should be included on FHWA Form 531 and FHWA Form 532 forms (see also FHWA Form 531 , Item B.6, Funds from Federal Highway Administration, Item B.7, Funds from Other Federal Agencies, and Item B.8, Funds from Local Governments, and FHWA Form 532 , Item A.10, Grants-in-Aid to Local Governments).

Local governments include counties, townships, municipalities, and agencies subordinate to them. Subordinate agencies to local governments may include special highway authorities and districts, regional authorities, and special multi-jurisdictional authorities. Local government highway funding must be reported on the FHWA Form 536. See section 2.4 for specific instructions on local highway finance reporting.

Toll facility data should be identified and reported separately from other State highway finance data. To report this information, submit the Toll facility annual financial report or statement to FHWA. See section 2.3 for more details. Income and expenditure data from State toll facilities is not entered on FHWA Form 531 or FHWA Form 532 forms.

Sinking funds or other debt reserves for highway debt should be reported on FHWA Form 531, Item B.10.a, Investment Income, Bond Sinking Funds.

If the State DOT allocates funds for debt service to an account maintained by the State treasurer, bond commission, or other fiscal officer, record the complete transactions of the debt funds on the FHWA Form 531 and FHWA Form 532 forms.

Sinking funds and debt service for mass transit should be reported separately from highway debt. Report debt service for mass transit on the FHWA Form 532, Item A.11.d, Debt Service.

FHWA Form 531 and FHWA Form 532 forms should be used to record at least the major funds administered by the State for highway and mass transit purposes—often a transportation or highway fund.

If reported by fund category, each major fund (such as a State general fund, or highway or transportation fund) should be reported in separate column. Minor funds can be grouped in a single column.

Because FHWA Form 531 and FHWA Form 532 forms together constitute a balance statement of income and expense, transactions for each fund on the FHWA Form 531 and on FHWA Form 532 forms should be in balance.

If a single fund is used for all highway-related activities, or if highway transactions are made entirely through the State general fund, column (A) should be used to represent the highway fund’s financial transactions.

If all highway and mass transit-related activities are paid for through a transportation fund, use separate columns for highways and mass transit. Use additional columns for informational purposes and for reporting by activity, function, or State agency and to report mass transit activities.

When States fund highway activities through several sources, breaking down income and expenditure by activity, function, or fund can provide a clearer perspective on highway finance. Examples of income and expenditures to be reported on FHWA Form 531 and FHWA Form 532 forms are given below.

In general, motor fuel and motor vehicle distributions shown on FHWA556 and FHWA566, item 8, should be reported on FHWA Form 531 form as receipts. A note of any distribution that is not included on FHWA Form 531 should be made, such as funds designated for agencies other than the DOT.

Report other receipts and expenditures related to highway and mass transit activities on FHWA Form 531 and FHWA Form 532, with the exceptions noted in the table below.

FHWA Form 531 must be submitted by the State DOT in Fuels and FASH.

Unless specified otherwise, items in FHWA Form 531 are entered in whole dollar amounts. Round decimal fractions of dollars to the nearest dollar.

FHWA Form 531 has two tabs, tab A and tab B; tab A is used for a summary, and tab B is for recording essential details about receipts. Items on tab A are numbered to correspond with items on tab B.

On tab B, columns (A), (B), (C) (and so on) are for the State to identify and report funds administered by the State DOT or other reporting agency. The columns may also be used to report data by agency, function, or activity. This structure makes tracking the flow of revenues into each fund and expenditures out of each fund easier.

For each column, specify the type of data (name of agency, function, or activity). Tab B is for recording essential details of summary entries. Provide additional details in a note.

This item is for reporting the funding balances available at the beginning of the reporting year.

Enter the balance of each fund, agency, or activity in the letter-titled columns in items A.1 to A.3. The balances represent cash and the value of investments at cost.

Report the following balances:

= Previous Year FHWA Form 532, Item C, Unexpended Balances at end of the year

This item is for the unexpended balance from the previous year. Enter the amount of cash and investments reported as an unexpended balance for the previous year.

This item is for recording adjustments to prior year ending balances.

Generally, beginning balances should be revised only because of an audit or to add a fund or agency to the reporting. Lapsed appropriations or allocations should not be shown as revisions of the balances because they may not represent cash transfers.

When lapsed appropriations or allocations result in a reversion of funds to the State general fund, the resulting cash transfer should be accounted for as a transfer to the State general fund in FHWA Form 532, Item A.13.a, Transfer to State General Fund for State General Purposes. When adjustments are made in item A.2. to revise a balance in item A.1, an explanation of the revision must be provided in a note.

Transfers among the funds reported on FHWA Form 531 should not be recorded as adjustments of balances, because these are internal adjustments. Transfers are reported in FHWA Form 531, item C, and in FHWA Form 532, item B. These two items must match.

Item A.3 shows the difference of item A.1. and adjustments from item A.2. Fuels and FASH calculates the total automatically.

This item is for reporting income from various taxes, funds, and activities. Ten categories are provided on tab A for summarizing and reporting income by fund, agency, or activity.

Identify income by fund, agency, or activity in the lettered columns for items B.1 to B.11 on tab B.

Below are detailed descriptions of the subitems of item B.

This item is for reporting revenue raised from State motor fuel taxes. Enter the net amount of State revenue that was raised from State taxation of motor fuels. Net motor fuel revenues are directly related to taxation on highway use and highway users of gasoline, gasoline blends, and special fuels as reported on FHWA Form 556.

The revenue distributions represented in this item should correspond to State statutes concerning highway-related funds. The detail for this item assists in reconciling FHWA Form 556 and FHWA Form 531.

If FHWA Form 556 is provided, prepare a reconciliation between FHWA Form 556, item 8, and this item. To prepare a reconciliation, either revise FHWA Form 531 or submit a supplemental statement containing information like details in items B.1.a through B.1.f.

FHWA Form 532 may also have to be revised because FHWA Form 531 and FHWA Form 532 need to balance.

If FHWA Form 556 is not available when FHWA Form 531 is prepared, leave the detail for this item blank.

= FHWA Form 556, Item 8.k, Total

This item is for reporting the amount of net motor fuel tax revenue that was distributed (allocated) by the collecting agency to the State or the expending agency.

This amount should correspond to the total distributions reported on FHWA Form 556, item 8. If FHWA Form 556 is prepared for a different reporting year than FHWA Form 531, the amount reported on FHWA Form 556, item 8.k, is still reported in this item. Make compensating adjustments for the resulting timing difference in FHWA Form 531, item B.1.b.

This item is for reporting any difference between the motor fuel tax revenue reported on FHWA Form 531 and the revenue reported on FHWA Form 556 that is attributable to timing differences.

A timing difference may be caused by a difference in reporting years used for the two reports, or by delay between the time funds are reported as distributed in collecting agency records and the time funds are reported as received in highway agency records. Before entering any amount in this item, verify that timing differences, not differences in definition, are the reason for differences between the reports. FHWA Form 531 and FHWA Form 556 should be prepared using the same definitions for motor fuel taxes.

This item records costs incurred in the collection of motor fuel taxes that were not deducted on FHWA Form 556, item 4.

Typically, deductions from motor-fuel tax revenues for collection expenses and administrative costs made by the collecting agency before distribution of the funds should be reported on FHWA Form 556. If collection expenses are not paid out of motor fuel revenues and instead are paid out of appropriated funds (e.g., general fund account), they should be reported in this item. Enter the amount as a negative number.

These items are for reporting amounts distributed on FHWA Form 531 that are not fully accounted for on FHWA 556, item 8, if any. Specify the agency, activity, or purpose of the distribution.

Distributions reported in FHWA Form 556, item 8. Amounts Distributed, should be fully accounted for on FHWA Form 531 and FHWA Form 532.

If your State excludes some non-highway distributions of motor-fuel tax revenue from FHWA Form 532, report the excluded amounts in this item and identify them separately. For example, if FHWA Form 556, item B.8, includes distributions to a school fund, but a State prefers not to account for these expenditures on FHWA Form 532, item A.13, the amounts should be reported as a deduction here and identified as a distribution to the School Fund.

If multiple non-highway funds or accounts are excluded, such as adjustments for audited financial statements, list each separately. Adjustments can be positive or negative numbers, depending on the nature of the adjustment, and should be entered into Fuels and FASH accordingly.

Add items under B.1. as needed.

Fuels and FASH calculates the total automatically from items B.1.a through B.1.e. This amount should equal the total shown for item B.1. on tab B.

This item is for reporting revenue raised from State motor vehicle, driver license, and motor carrier taxes and fees. Report the net amount of State revenue that was raised from State taxation of motor vehicles, drivers, and motor-carriers. These revenues are related to State taxation imposed on the ownership and operation of motor vehicles for highway purposes through motor vehicle registration fees, dealer licenses, driver licenses, certificates of title, gross receipts taxes, distance taxes, weight/capacity taxes, permit fees, fines and penalties for infractions of the motor vehicle registration laws, and miscellaneous receipts of the State motor vehicle agency.

The information reported in this item should be consistent with that reported on FHWA Form 566, item 8. Amounts Distributed. The detail for this item helps reconcile FHWA Form 566 with FHWA Form 531.

If FHWA Form 566 is not available at the time FHWA Form 531 is prepared, the detail for this item should be left blank.

If FHWA Form 566 is provided, prepare a reconciliation between FHWA Form 566, item 8., and this item. Reconciliation can be either a revised FHWA Form 531, tab 1, or a supplemental statement containing information like notes in items B.2.a through B.2.f.

=FHWA Form 566, Item 8, Amount Distributed

This item is for reporting the amount of net motor vehicle revenue that was distributed by the collecting agency to the expending agency. This should correspond to the amount reported on FHWA Form 566, item 8.

If FHWA Form 566 is for a different reporting year than FHWA Form 531, report the amount in FHWA Form 566, item 8, in this item, and in item B.2.b, make compensating adjustments for the timing difference.

This item is for reporting differences due to the timing of the reporting of funds. Enter any difference between FHWA Form 531 and FHWA Form 566 attributable to a timing difference. Timing differences may be caused by a difference in reporting years or by a delay between the time funds are reported as distributed in collecting agency records and the time funds are reported as received in highway agency records.

Before entering any amount in this item, verify that timing differences, not differences in definition, are the true reason for differences. FHWA Form 531 and FHWA Form 566 should be prepared using the same definitions for motor vehicle, driver license, and motor carrier taxes, fees, and revenues.

This item is for reporting the costs incurred in the collection of taxes and fees for motor vehicles, driver licenses, and motor carriers that were not deducted on FHWA Form 566, item 2 or item 4.

Report collection costs paid after the distribution of revenues from motor vehicle, driver license, and motor carrier taxes that are not reported on FHWA Form 566. Do not report deductions for collection expenses and administrative costs made by the collecting agency before revenue distribution—those deductions are reported on FHWA Form 556.

These items are for reporting amounts distributed on FHWA Form 566, item 8, that are not fully accounted for elsewhere on FHWA Form 531 and FHWA Form 532.

Specify the agency, activity, or purpose of the distribution in a note for the item. All distributions reported on FHWA Form 566, item 8, should be fully accounted for on FHWA Form 531 and FHWA Form 532.

If your State excludes from FHWA Form 532 some non-highway distributions of revenues from taxes and fees for motor vehicles, driver licenses, and motor carriers, report the excluded amounts in this item and identify each of them.

For example, if FHWA Form 566, item B.8, includes distributions to a school fund, but the State does not account for these expenditures in FHWA Form 532, item A.13, the State should report these amounts as a deduction in this item and add a note that they were distributed to the school fund.

If multiple non-highway funds or accounts are excluded, list each separately.

This item shows the sum of items B.2.a through B.2.e. Fuels and FASH calculates the total automatically. This amount should equal the total shown for item B.2.

This item is for reporting the net revenues received from appropriations for all highway and mass transit activities from State general funds.

The purpose of the appropriations should be identified in the customizable item name provided in Fuels and FASH. Add a note with necessary details or explanations.

Although most transportation funding comes through dedicated highway and mass transit accounts and trust funds, some highway and mass transit-related functions may be funded by a State’s general fund (for example, for an agency other than the State DOT to work on State Park roads, and for the highway law enforcement and safety activities of the State police). Furthermore, the State general fund may support debt service on State obligations issued for highway or mass transit purposes.

If another State agency provides funds to a State DOT for road work, report the revenue as coming from the original source of funding. A general fund is often the source of funds for the other State agency.

This item is for reporting the amount of other State taxes or fees that were dedicated and used for highway and mass transit purposes.

Report the following revenues in this item:

The taxes or fees reported in this item are not classified as highway-user revenues and are not reported in FHWA Form 531, item B.1. or item B.2. Other State taxes or fees transferred to local governments for highways should be reported in this item, even if the funds do not pass through the State DOT.

Record in this item only the share of the taxes and fees that are legislatively allocated or dedicated to highways and mass transit.

This item is for reporting funds transferred from toll facilities to non-toll State accounts for State highways, mass transit, and other activities.

Do not include reimbursements for road work on State toll facilities performed by the State DOT.

Reimbursed expenditures are considered expenditures of the toll facility. If a toll facility report does not specify the work performed on its behalf by the State DOT, the State should submit a supplementary statement showing these amounts.

This item is for reporting the total amount of funds received by the State from FHWA. Report only actual payments, not obligations, earnings, or vouchers submitted but not paid.

Some States maintain separate funds for Federal-county, Federal-State-county, or Federal-city programs. Federal expenditures for projects on roads and streets that are under local jurisdiction should be identified and recorded in the appropriate fund columns on tab 2.

If no separate account or fund has been established, States should still identify and report in separate columns Federal, State, and local funds for work on roads under local jurisdiction. These income items can then be related to the direct State expenditures that are entered in FHWA Form 532, item A.9, or State transfers in item A.10. If there are not enough columns available for these entries, report the transactions in a supplemental statement or in a note.

The Transportation Infrastructure Finance and Innovation Act of 1998 (TIFIA), 23 U.S.C 601 et seq., provides Federal credit assistance to major transportation investment projects of critical national importance. Federal credit assistance takes the form of secured loans, loan guarantees, and standby lines of credit. Amounts received under this program should be identified in a note that also indicates how the funds were used.

Federal funds that are used to capitalize a State Infrastructure Bank (SIB) or infrastructure revolving fund should be identified in a note. The receipt and expenditure of those funds should also be shown in a separate column on FHWA Form 531 and on FHWA Form 532.

Identify Federal funds used on a toll road project in a note.

This item is for reporting the funds received from FHWA for highway purposes. The FHWA distributes funds to every State for highway purposes.

This item is for reporting the funds received from FHWA for transit purposes.

Funds transferred to transit projects administered by the Federal Transit Administration (FTA) from the Surface Transportation Program (STP) and the Congestion Mitigation and Air Quality Improvement (CMAQ) program should be reported here.

Fuels and FASH calculates the total automatically from data in items B.6.a. and B.6.b.

This item is for reporting funds for highways and mass transit received from Federal agencies other than FHWA. Identify the agencies and amounts in a note.

Sometimes, one Federal agency administers funds provided by another Federal agency. In such a case, to the extent possible, identify the amounts as payments from the source agency, not the administering agency. For example, FTA funds administered by FHWA should be identified as payments from FTA to the State.

All Federal funds paid to, shared with, or expended by the State for road purposes should be reported in this item, including Federal funds that were paid to State agencies other than the State DOT or that were paid in the final instance to local governments.

This item is for reporting funds received from FTA to be expended for highway projects. Amounts should be obtained from the State treasurer’s office, accounting office, or revenue office.

This item is for reporting funds received from FTA to be expended for mass transit projects. Amounts should be obtained from the State treasurer’s office, accounting office, or revenue office.

This item is for reporting on funds received from NHTSA to be expended for highway purposes.

Exclude FHWA funds administered by NHTSA under provisions of 23 U.S.C. 402, 403, 405, 406, 407, 408, 410, and 411. Include all other funds administered by NHTSA.

This item is for reporting on funds received by the State from the U.S. Forest Service to be expended for highway purposes.

The National Forest Fund transfers a portion of timber sale receipts to States for roads and schools in counties where forests are located. Many State agencies pass such funds through to county governments rather than to the State DOT. This may make determining the actual amount used for roads difficult. States may report this information in notes indicating the approximate percentage of Forest Service receipts used for roads in the past. Amounts should be obtained from the State treasurer’s office, accounting office, or revenue office.

These items are for reporting all other funds received for highway that were expended for highway purposes. Identify the amount and Federal agency in a note.

This item shows the sum of items B.7.and B.7.o. Fuels and FASH calculates the total automatically.

This item is for reporting the funds provided by local governments for expenditure by the State on highways or mass transit.

If other rural units, such as county road improvement districts, make contributions, add a note providing the specifics.

Funds from local governments that were advanced to the State before expenditure or as a loan should also be recorded in this item. Include unexpended amounts in the balances. Show the repayment of advances by the State in FHWA Form 532, item A.10, but omit loan advances and repayments made in the same year.

The proceeds of local bonds on which the State is responsible for meeting the interest and/or principal payments should be reported in item B.9. instead of in this item.

If a portion of the local governments’ share of State highway-user revenues is not paid directly to local governments but is retained by the State and used for the following purposes, the funds were never transferred by the State to the local government and therefore should be treated as if they were generated and expended solely by the State:

In such cases, do not show a transfer of funds in this item or in FHWA Form 532, item A.10.

When funds transferred from local governments are earmarked for a specific purpose, the amounts should be identified in an appropriate column that shows the linkage between the local funds and their object of expenditure.

When local governments provide at least part of the matching funds for State-administered Federal-aid projects, funds for these projects should be recorded in this item, whether the State expenditures occur on State-jurisdiction roads or local-jurisdiction roads.

= FHWA Form 541, Item 9.A.7, Total, Allotment of Proceeds of Sales

This item is for reporting the net proceeds of bonds issued for the construction of highways and mass transit. The net proceeds of obligations issued for the purpose of refunding existing debt should also be included in this item.

The amount reported should agree with FHWA Form 541, item 9.C. Any difference should be explained in a note.

The net proceeds of State bonds issued by the State for local roads and streets should be recorded in a separate column from the proceeds from the financial transactions associated with local bonds assumed by the State.

The proceeds from the issuance of State highway notes or other evidence of indebtedness that will be redeemed within 2 years should not be recorded on FHWA Form 531. Instead, the amount of the temporary indebtedness outstanding at the beginning and the end of the year should be deducted from the beginning-of-year balances in FHWA Form 531, item A, and the end-of-year balances in FHWA Form 532, item C.

The issuance of warrants (if any) for payments on construction or maintenance work should be handled in the same manner: Record transactions on FHWA Form 532 as expenditures during the period in which the warrants were issued, show the cost for the year in which it was incurred, and avoid the need to record the retirement of the warrants.

This item is for reporting types of revenue that cannot be classified under another item on FHWA Form 531. Identify major items in a note for FHWA Form 531.

Do not include transfers from other State agencies to the State DOT in this item. Instead, record them according to the original source of the revenue. The source is often the State general fund, so the amounts transferred by other State agencies would be reported in FHWA Form 531, item B.3.

Revenue from transactions that are, in effect, reductions of expenditures should not appear as income on FHWA Form 531 (or as a balance adjustment) but should be deducted from the appropriate expenditure item or items on FHWA Form 532. For example, proceeds from the sale of right-of-way should be excluded from this item and should instead be deducted from right-of-way costs reported in FHWA Form 532, item A.1.a. Similarly, proceeds from the sale of maps or plans should be deducted from the gross cost of creating these items, which should be reported in FHWA Form 532, item A.4.a.

This item is for reporting the investment income of sinking fund accounts or other accounts specifically established for debt service transactions.

Investment income includes the interest on deposits and investments, plus the net profit or loss from the exchange of cash and investments. This information is needed for States that have established reserves for the retirement of outstanding debt or for the payment of interest and retirement charges on bonds.

This item is for reporting all revenues from interest on deposits and investments and investment income from the net profit or loss from the purchase and sale of investments from all accounts other than bond sinking funds.

This item is for reporting contributions from private sources. Private sector participation in financing highway projects can take the form of cash contributions, transfers of real property, construction of facilities, and services such as engineering. When the value of donated land, facilities, or services is reported in this item, a like amount should be added to FHWA Form 532, items A.1., A.7., or A.9, as appropriate, and should also be identified in a note on FHWA Form 532.

These items are for reporting large items of miscellaneous income. If additional room is needed, this information can be provided in a note.

Fuels and FASH calculates the total automatically from data in items B.10.a through B.10.h.

Fuels and FASH calculates the total automatically from data in items B.1 through B.10.

= FHWA Form 532, Item B, Interfund Transfers Out

This item is for the sum of all interfund transfers within the agency. It is for reporting transfers among funds, in conjunction with FHWA Form 532, item B—such as from State highway funds to the sinking fund, or from the construction fund to the maintenance fund.

Do not include transfers from motor fuel and motor vehicle revenues to the general fund; instead, show these as expenditures in FHWA Form 532, item A.13.a. Similarly, transfers from the State general fund to highway agency funds should be shown in FHWA Form 531 item B.3.

The sum of the entries in item C should equal the sum of the entries in FHWA Form 532, item B. If not, add a note explaining the reason for any difference.

= FHWA Form 532, Item D, Total Funds Accounted For

This item is for the sum of items A.3, B.11, and C. Fuels and FASH calculates this amount automatically.

The entries in item D must equal the entries in FHWA Form 532, item D.

FHWA Form 531 has relationships with several other FHWA 500-Series forms.

Item A, Balances on hand at beginning of year

Item A, Balances on hand at beginning of yearThe current year’s opening balance should agree with the amount reported on the prior-year FHWA Form 532, item C, Unexpended balances at the end of the year. Provide an explanation for any large difference.

The amount reported in item B.1.a on tab 1 should agree with FHWA Form 556, item 8.k. If there is a difference, use FHWA Form 531, items B.1.b through B.1.e to explain it.

The amount reported in item B.1.a on tab 1 should agree with FHWA Form 556, item 8.k. If there is a difference, use FHWA Form 531, items B.1.b through B.1.e to explain it.

The amount reported in item B.2.a, State Motor vehicle, driver license and motor carrier taxes and fees, should agree with the amount in FHWA Form 566, item 8. If there is a difference, use FHWA Form 531, items B.2.b through B.2.e to explain the difference. Common explanations are timing differences, funds in transit, and exclusion of certain funds from FHWA Form 531.

The amount reported in item B.2.a, State Motor vehicle, driver license and motor carrier taxes and fees, should agree with the amount in FHWA Form 566, item 8. If there is a difference, use FHWA Form 531, items B.2.b through B.2.e to explain the difference. Common explanations are timing differences, funds in transit, and exclusion of certain funds from FHWA Form 531.

The amount reported on FHWA Form 531, item B.9, Proceeds of sale of bonds, should agree with the amount reported in FHWA Form 541, item 9.C., Total Allotments. Typically, this also equals FHWA Form 541, item 8.D, Total Net proceeds. A common error is to report the par value of the issue from FHWA Form 541, item 8.A instead of net proceeds.

The amount reported on FHWA Form 531, item B.9, Proceeds of sale of bonds, should agree with the amount reported in FHWA Form 541, item 9.C., Total Allotments. Typically, this also equals FHWA Form 541, item 8.D, Total Net proceeds. A common error is to report the par value of the issue from FHWA Form 541, item 8.A instead of net proceeds.

The amount reported on FHWA Form 531, item C, Interfund Transfers In, must equal the amount in FHWA Form 532, item B, Interfund Transfers Out.

The amount reported on FHWA Form 531, item C, Interfund Transfers In, must equal the amount in FHWA Form 532, item B, Interfund Transfers Out.

The amount reported on FHWA Form 531, item D, Total funds to be accounted for, must equal the amount in FHWA Form 532, item D, Total funds to be accounted for.

The amount reported on FHWA Form 531, item D, Total funds to be accounted for, must equal the amount in FHWA Form 532, item D, Total funds to be accounted for.

FHWA Form 532 should be completed by the State agency that collects expenditure data.

A copy of FHWA Form 532 should be submitted by the preparing agency using the Fuels and FASH application.

Provide the State name, reporting year, notes, the data reporting source, and the name of the preparer of the forms.

Form FHWA 532 has two tabs, tab A and tab B; tab A is for providing a summary of receipts, and tab B is for reporting essential details about receipts. Items in tab A are numbered to correspond with items in tab B.

The columns in tab B (numbered A, B, C, etc.) are for identifying and reporting at least the major funds administered by the State DOT or other reporting agency. The columns may also be used to report data by agency, function, or activity. This structure makes tracing the flow of revenues into and expenditures out of each fund relatively easy.

If additional detail is necessary, provide it in a note for the form.

Each item in the form is explained below.

This item is for reporting the capital outlay for highways, roads, and streets that are part of the State highway system.

Capital outlay includes:

The cost of construction materials and supplies, and if possible, construction machinery and equipment, should be reported. Administrative costs directly assignable to specific capital outlay projects should be included, but other administrative costs should be reported in item A.4.

Do not include capital expenditures for

The classification of highway construction and maintenance expenditures should be consistent with the criteria provided in the American Association of State Highway and Transportation Officials (AASHTO) Maintenance Manual (2007). Exceptions to the rules are provided in the manual. Because not all situations can be anticipated, States should use best judgment in classifying and recording expenditures.

This item is for reporting the cost of acquiring a right-of-way for highways. Include the costs of right-of-way administration; purchase of land, improvements, and easements; and moving and relocating buildings, businesses, and persons.

This item is for reporting the cost of preliminary and construction engineering for highways. Include the costs of field engineering and inspections; surveys, material testing, and borings; preparation of plans, specifications and estimates (PS & E); and traffic and related studies.

This item is for reporting the costs related to the construction of highways. Include expenditures for construction, relocation, resurfacing, restoration, rehabilitation, and reconstruction (3R/4R), widening, safety and capacity improvements, restoration of failed components, and additions and betterments of roads and bridges.

Construction includes the following:

More examples of construction expenditures can be found in FHWA Form 534 Reporting Requirements.

Fuels and FASH calculates this item automatically by summing items A.1.a. through A.1.c.

This item is for reporting expenditures classified as maintenance for highways, roads, and streets that are part of the State highway system.

For purposes of FHWA Form 532, maintenance does not include improvements, additions, or resurfacing, or restoration, rehabilitation, and reconstruction (which should be reported in item A.1), but it does include preventive maintenance. Preventive maintenance extends pavement and bridge service life to at least the design life of the facility. Preventive maintenance involves programs that delay or eliminate the necessity for future resurfacing, restoration, rehabilitation, and reconstruction.

Maintenance of roadways includes routine roadway surface, shoulder, roadside, and drainage maintenance. Maintenance of structures includes repair and maintenance of bridges, tunnels, subways, overhead grade separations, and other structures, including substructure, superstructure, stream bed operations, and bridge painting. Maintenance includes spot patching and crack sealing of roadways and bridge decks, maintenance and repair of highway utilities and safety devices, including repair and painting of route markers, signs, guardrails, fences, signals, and highway lighting. Do not include maintenance expenditures for toll facilities (see section 2.3 for reporting requirements for toll facilities).

Maintenance for the purposes of this item is the function of preserving and keeping the entire highway, including surface, shoulders, roadsides, structures, and traffic control devices, as close as possible to the original condition as designed and constructed. For improved or reconstructed facilities, maintenance ensures continued service as redesigned.

The cost of maintenance supplies, materials, and equipment should be included. As with construction expenditures, maintenance expenditures include administrative and engineering costs directly assignable to maintenance projects.

This item is for reporting operational expenditures for

This item is for reporting operational expenditures for the operation of intelligent and other traffic control and surveillance systems that are designed to monitor and control traffic by managing vehicle flow on streets and highways.

The purpose of these systems is to improve transportation performance and safety, vehicle fuel economy, and air quality. These systems include traffic signal control; freeway, tunnel and bridge surveillance and control; electronic message boards; video monitoring; traffic information radio stations; and motorist aid. Also included is the cost of operating toll-free drawbridges, tunnels, and ferries.

Only the operating costs of traffic control facilities should be included in this item. The construction of traffic control facilities is included in item A.1. Maintenance of these facilities is included in item A.2.

This item is for reporting operational expenditures for snow removal from roadway or roadside, sanding and chemical applications, and the erection and removal of snow fences.

This item is for reporting miscellaneous operational expenditures not covered under A.3.a. and A.3.b, such as expenditures for highway beautification, junkyard control, control of outdoor advertising, litter pickup, and mowing. Also include vegetation management, erosion control programs and programs that monitor highway air quality in non-attainment areas. Add a note identifying air quality programs. Expenditures for planning air quality programs should be reported in item A.4.b.

Fuels and FASH calculates the total automatically from items A.3.a. through A.3.c.

This item is for reporting general and miscellaneous expenditures that are not readily distributable to specific construction or maintenance projects.

For FHWA Form 532, costs directly attributable to specific projects should be assigned to the appropriate classification in items A.1, A.2, A.7, or A.9. Expenses for the administration of State mass transit programs are reported in item A.11.c. or item A.12.c.

This item is for reporting expenses for administration, engineering, and miscellaneous expenditures not otherwise classified:

The salaries, wages, related payroll expenses, and fringe benefit costs incurred for the time an employee works on a function or activity should determine the allocation of the cost to capital outlay, maintenance, or administration. Payroll expenses and fringe benefits include employer’s Social Security and pension fund contributions, insurance premiums, and other payroll benefits.

Expenses for administrators who carry out general administration, supervision, and overhead for management, supervision, and control of the State DOT should not be allocated to capital outlay and maintenance. Such administrative costs are for the directors, department heads, other transportation and management officials, legal departments, accounting sections, budget administrations, personnel functions, and procurement operations.

Likewise, do not include in this item the administrative costs for motor fuel and motor vehicle revenue collection. These amounts are reported on FHWA Form 556, FHWA Form 566, or FHWA Form 531, items B.1.c and B.2.c.

If your State has a secondary-road division for administering State and Local programs, to the extent that the division’s spending is limited to improving State and Local roads, the administrative costs should be reported in item A.7.c or item A.9.c, not in this item.

This item is for reporting expenditures for highway planning, research, and investigation. Enter all such expenditures, including those for laboratory and field research in road and bridge materials and design, traffic research, technical and financial studies, and similar investigations by the State highway planning division or equivalent. Include expenditures for activities funded by the State Planning and Research Program with SPR funds from FHWA.

Fuels and FASH calculates this item automatically by summing items A.4.a. and A.4.b.

This item is for reporting highway law enforcement and safety expenditures by the State DOT, State police, department of public safety, traffic safety commission, and other law enforcement and safety agencies.

Law enforcement and safety expenditures are classified as

The highway law enforcement activities of other State agencies funded independently of the State DOT should be reported in a separate column on FHWA Form 531 and FHWA Form 532. If a supplement is provided, it should use the same classification of expenditures as shown in item A.5 and show the revenue source for the highway law enforcement and safety expenditures (often the State general fund for highway patrol, police, or department of public safety).

Highway safety expenditures should include, to the extent possible, the Federal safety programs such as those provided by 23 U.S.C. 402, 403, 405, 406, 407, 408, 410, and 411 by NHTSA and the Motor Carrier Safety Assistance Program.

Highway safety construction expenditures should be reported in FHWA Form 532, item A.1.c.

This item is for reporting the expenses of the State highway patrol or similar agency for providing traffic supervision and patrolling the highways.

Traffic supervision includes:

Report the cost of salaries, benefits, pensions, and equipment costs of officers engaged in these activities.

Costs of criminal investigations and other general policing activities should not be shown in item A.5. If they are financed from highway revenues, they should be reported in item A.13.

This item is for reporting expenses related to safety programs and similar activities. Enter expenses of safety programs and similar activities relating to the promotion of highway safety and traffic accident prevention, whether conducted by the State DOT, the highway patrol, a traffic safety commission, or other State agency.

Highway safety programs include:

Enter the cost of job safety and accident prevention programs for State employees and highway safety research programs in item A.4.

This item is for reporting expenses related to vehicle inspections. Enter the expenses of inspecting vehicles, operating inspection stations, and other activities related to periodic motor vehicle inspection programs, including motor vehicle emissions inspection and motor carrier safety inspection.

This item is for reporting expenses for enforcement of vehicle size and weight. Enter expenditures for installing, maintaining, and operating truck weighing stations and other devices involved in the enforcement of vehicle equipment and size and weight limitations on highways. Costs of installing and operating ports-of-entry should be included here if the ports are primarily used as weighing stations. If the ports are used also as information centers, quarantine stations, tax collection points, and so forth, the costs charged to highway funds should be distributed to the other activities as appropriate. Include vehicle weight enforcement facilities eligible for Federal-aid highway funding.

Fuels and FASH calculates this total automatically by summing items A.5.a. through A.5.d.

This item is for reporting interest and redemption payments for bonds that were issued for highway purposes. Debt service also includes expenditures incidental to the sale and retirement of highway debt.

When transfers are made from the highway fund to a debt service fund or sinking fund outside the highway fund or agency, enter the payment in FHWA Form 532, item B as a transfer from the highway fund column and in FHWA Form 531, item C as a receipt to the debt service fund.

Set up separate columns on FHWA Form 531 and FHWA Form 532 to report allocations of debt service funds and debt service expenditures, including the transactions of highway debt sinking funds.

Debt service on obligations not maintained by the highway agency may involve revenues not included in the highway fund. States should report these amounts in the separate columns for highway debt on FHWA Form 531 and FHWA Form 532.

Report payments of interest and redemption charges on State bonds issued for the construction of local roads and streets in item A.6 and post in a separate column established for that purpose or provide details in a note. Debt service for toll facilities should be reported separately from highway debt. Debt service on mass transit issues is reported in item A.12.d.

This item is for reporting debt-related administrative expenses. Enter all such expenses, including the costs of preparing and issuing bonds, fiduciary fees, and bond handling charges.

This item is for reporting interest paid, including accrued interest received on the sale of bonds or paid on redemptions in advance of maturity. Interest paid on short-term notes or warrants should be included, although the proceeds and redemption of short-term loans that will be redeemed within 2 years are not included (see FHWA Form 531, item B.10).

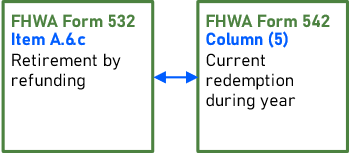

= FHWA Form 542, Column 5, Current redemption during year (par value)

This item is for reporting the amount of net redemption payments for highway debt that were funded by current income or sinking funds.

Net redemptions are the funds expended to retire or redeem outstanding obligations. They consist of the par value of bonds redeemed, as reported on FHWA Form 542, column 5, plus any premiums, or less any discounts. Such premiums or discounts may occur if bonds are purchased on the open market before they normally would have been redeemed. Any large difference between the net amount reported in this item, and the par issuance amount reported on FHWA Form 542, column 5, should be explained in a note.

= FHWA Form 542, Column 6, Refunding redemption during year (par value)

This item is for reporting the amount of net redemption payments for highway debt that were funded by the proceeds of refunding bonds.

Net redemptions are the amount of funds expended to retire or redeem outstanding obligations and consist of the par value of bonds redeemed by refunding issues, as reported on FHWA Form 542, column 6, plus any premiums or less any discounts. In many cases, a premium must be paid to retire bonds before their maturity.

Also enter the net amount of outstanding bonds that were refunded through the deposit of refunding bond proceeds into escrow accounts that use those proceeds and investment income to make bond administrative costs, and all remaining principal and interest payments.

This item is for reporting direct expenditures and allocations made by State agencies for capital outlay, maintenance, and administration of highways, roads, and bridges that are under State jurisdiction but are not on the State system, such as roads in State parks, forests, reservations, and institutions. In many States, such roads are not under the control of the State DOT. Data for expenditures on these roads and the revenues that funded them have to be obtained from the responsible State agencies.

If the State DOT is responsible for all State jurisdiction roads, including those in parks, forests, reservations, and institutions, then the amounts spent on State roads on and off the State system may not be separable. In this case, the State may leave this item blank, report the combined amounts in items A.1 through A.4, and add a note explaining that it reports combined amounts.

The general instructions and classification criteria for items A.1 through A.4. (State highway capital outlay, maintenance, operations, and administration, respectively) also apply to items A.7.a through A.7.c.

This item is for reporting the State capital outlay for roads and streets that are under State jurisdiction but are not on the State system.

This item is for reporting expenditures for State maintenance and for highway and traffic services for State roads and streets that are not on the State system.

This item is for reporting administrative costs directly attributable to State work on State roads and streets that are off the State system.

Fuels and FASH calculates the total of expenditures on other State roads not on the State system automatically from items A.7.a through A.7.c.

This item is for reporting State subsidies of or payments to toll facilities. State direct expenditures on State toll facilities should be reported with the transactions of the toll facility. They should be included and noted in this item as if they were a subsidy. See section 2.3 for data reporting requirements for toll facilities.

This item is for reporting State expenditures for work contracted or performed on highways, roads, and streets that are under the jurisdiction of local governments.

Use a separate column in tab B on FHWA Form 531 and FHWA Form 532 to identify the receipts, expenditures, and balances applicable to direct State work on local roads and streets.

Federal laws permit the expenditure of Federal-aid highway funds (and other funds) on roads off the State highway systems. Expenditures by the State on such projects involving Federal funds and local matching funds should be included in this item. The amount of local matching funds should be identified in FHWA Form 531, item B.9.

The general instructions and classification criteria for items A.1 through A.4 (State highway capital outlay, maintenance, highway and traffic services, and administration, respectively) apply as well to expenditures reported in items A.9.a through A.9.c.

State DOT expenditures for machinery and equipment used on local road work should be included in this item if identifiable and separable from other equipment expenditures. State capital outlay on local roads and streets as a part of co-supported projects should be reported in these items. State capital outlay on State highways as a part of co-supported projects should be reported in item A.1.

This item is for reporting expenditures on highways, roads and streets that are under local jurisdiction made directly by the State or under State supervision.

Any expenditure for acquisition of right-of-way or for preliminary and construction engineering should be identified in a note.

This item is for reporting State expenditures for maintenance and highway and traffic services on local roads and streets. Expenditures for highway and traffic services should be described in a note.

This item is for reporting State administrative expenses that can be allocated specifically to managing State work on local roads and streets or assisting local governments in their road programs.

Fuels and FASH calculates the total automatically from items A.9.a through A.9.c.

This item is for reporting funds paid as grants-in-aid or otherwise transferred to local governments or local road improvement districts. If the revenue sources for State grants to local governments are separately identified from those for direct State expenditures, use separate columns to account for these transactions. This would clearly show the expenditures and the specific revenues and revenue sources that funded them.

Federal-aid highway funds and other Federal funds passed through to local governments should be included in this item and should be separately identified. These funds should be identified either in a separate column on the FHWA Form 531 and FHWA Form 532, or in a note showing the amount of Federal funds transferred and the Federal agency.

The statutory allocations of highway-user revenues to local governments should be reported in this item. However, when the State withholds a portion of the funds as reimbursement for prior expenditures or advances, or as local matching funds for State-local projects, the amounts withheld should be excluded from FHWA Form 532 and from item B.9 on FHWA Form 531. This avoids the double-counting of these funds as income and expenditure for two levels of government.

Do not include in this item payments to counties or other local units under contract to the State for maintenance or construction of State highways. These payments are considered State expenditures and should be shown in item A.1 or item A.2. Such expenditures should also not be included on FHWA Form 536. Payments on obligations assumed as reimbursement for local roads added to the State system are recorded in FHWA Form 532, item A.6.

Any amount reported in this item should be included in the State and Federal receipts shown in FHWA Form 536, items I.C and I.D.

This item is for reporting direct expenditures by the State for mass transit purposes.

The amounts reported should be limited to State-wide mass transit programs and should not include the direct expenditures of State-owned mass transit operators. State-wide programs may include carpools, van pools, specialized transit for the elderly or handicapped, park-and-ride lots, and other mass transit programs not tied to specific mass transit operators.

Information on the receipts and expenditures of mass transit operators are reported through the FTA Section 15 program. Include only mass transit activities that are not included in FTA’s Section 15 reports.

For the purpose of providing balanced statements, a separate column or columns on tab B of FHWA Form 531 and FHWA Form 532 should be used to record income (including Federal aid and other Federal funds), expenditures, and fund balances for direct mass transit activities.

Federal funding for mass transit activities comes primarily from FTA, but other Federal agencies and programs provide some support for mass transit. Report funds for mass transit provided by

This item is for reporting all direct capital expenditures of the State for mass transit.

This includes expenditures for

For example, State spending on bus lanes and on buying specialized vehicles for the transportation of handicapped individuals should be reported here.

This item is for reporting direct State payments for the operational expenses of mass transit programs.

For example, State expenditures for operating State-sponsored van pool services, including vehicle leases, maintenance, driver salaries, fuel, tires, insurance, and marketing, should be reported here.

This item is for reporting expenditures associated with program administration, technical studies, planning and research, and demonstration of mass transit programs and project.

This item is for reporting the interest and redemption payments for State obligations issued for mass transit purposes. This includes expenditures incidental to the sale and retirement of the bonds.

Fuels and FASH calculates the total automatically from data in items A.11.a through A.11.d.

This item is for reporting all funds paid as grants-in-aid, subsidies, or otherwise transferred to State, local, and private mass transit operators.

Include amounts transferred to local governments or regional authorities for mass transit purposes. Transfers to mass transit operators reported in this item should be consistent with information on State funding of mass transit as reported by mass transit operators through the FTA Section 15 program. If funds are transferred to local governments, regional authorities, or other governmental entities that do not provide data to FTA, report the amount of those funds in a note.

To ensure balanced statements, FHWA Form 531 and FHWA Form 532 should each have a separate column or columns on Tab B to record income, expenditures, and fund balances for mass transit grants-in-aid.

Include Federal funds passed through the State to mass transit operators or local governments for mass transit purposes and identify them separately but do not include amounts transferred by Federal agencies directly to mass transit operators.

This item is for reporting State capital assistance payments (including Federal funds) to local governments, regional planning organizations, and State, local, or private mass transit operators. Capital assistance payments can be for the purchase of buses, rail cars, or other capital activities described in item A.11.a.

This item is for reporting State operating assistance payments (including Federal funds) to local governments, regional planning organizations, and State, local, or private mass transit operators.

Operating assistance payments can be for reduced fares for elderly or handicapped or for operating activities described in item A.11.b or item A.12.c. Enter State mass transit planning and research payments (including Federal funds) to local governments, regional planning organizations, and State, local, or private mass transit operators.

Fuels and FASH calculates the total automatically from items A.12.a through A.12.c.

This item is for reporting expenditures for purposes not related to highways or mass transit that were funded by revenues reported on FHWA Form 531.

Expenditures reported here include:

This item is for reporting any amount transferred to the State general fund for general purposes. Include motor fuel and motor vehicle revenues dedicated to the State general fund. Also include any surplus revenue that reverts to the general fund.

Amounts transferred to the State general fund for a specific non-highway purpose should be excluded from this item and instead reported in items A.13.b through A.13.f.

These items are for reporting expenditures for non-transportation purposes. Specify the amount, funding source, and purpose of other non-transportation expenditures.

Fuels and FASH calculates the total automatically by summing items A.13.a through A.13.f.

This item shows the sum of items A.1. through A.13. Fuels and FASH calculates the total automatically.

This item is used in conjunction with FHWA Form 531, item C, and records the transfers among the funds reported on the two forms. Transfers for non-highway purposes or to the State general fund should be recorded in item A.13. The sum of the entries in item B must equal the sum of the entries in FHWA Form 531, item C. Any difference should be explained in a note.

This item is for reporting the balances remaining at the end of the reporting year for all funds identified on FHWA Form 531 and FHWA Form 532.

The discussion of balances presented in connection with FHWA Form 531, item A is applicable to FHWA Form 532, item C.

Fuels and FASH calculates the total automatically from items A.14, B, and C.

FHWA Form 532 has relationships with several FHWA 500-Series forms.

This item should report at least as much as FHWA Form 531, item B.6, Funds from FHWA.

The sum of these three items for capital outlay (item A.1, Capital outlay on State system; item A.7.a, Capital outlay on other State roads not on State system; and item A.9.a, Capital outlay on local administered roads) should be greater than or equal to the sum of item I.D. (Sum Total for Capital Outlay for System Enhancement and Operations) on all State government FHWA Form 534 reports.

The sum of these three items for capital outlay (item A.1, Capital outlay on State system; item A.7.a, Capital outlay on other State roads not on State system; and item A.9.a, Capital outlay on local administered roads) should be greater than or equal to the sum of item I.D. (Sum Total for Capital Outlay for System Enhancement and Operations) on all State government FHWA Form 534 reports.

Item A.2, item A.7.b, and item A.9.b

Item A.2, item A.7.b, and item A.9.bThe sum of these three items for maintenance (item A.2, Maintenance of State system; item A.7.b, Maintenance expenditures on other State roads not on State system; and item A.9.b, Maintenance expenditures on local roads and streets) should be greater than or equal to the sum of all State government FHWA Form 534s, items II, Expenditures for maintenance.

The amount reported in item A.6.c, Retirement by refunding, should equal the amount reported in FHWA Form 542, Column (5), Current redemption during year, unless the State paid a premium or discount.

The amount reported in item A.6.c, Retirement by refunding, should equal the amount reported in FHWA Form 542, Column (5), Current redemption during year, unless the State paid a premium or discount.

The amount reported in item A.6.d, Debt service on State obligations for highways—retirement by current income, should agree with the amount reported on FHWA Form 542, column (6), Total funds to be accounted for, unless the State paid a premium or discount. If the State paid something other than the par value, show the amount of the premium or discount in a note. A common error is to include debt service expenditures on State obligations for mass transit, which should be reported in FHWA Form 532, item A.11.d.

The amount reported in item A.6.d, Debt service on State obligations for highways—retirement by current income, should agree with the amount reported on FHWA Form 542, column (6), Total funds to be accounted for, unless the State paid a premium or discount. If the State paid something other than the par value, show the amount of the premium or discount in a note. A common error is to include debt service expenditures on State obligations for mass transit, which should be reported in FHWA Form 532, item A.11.d.

The amount reported in item B, Interfund transfers out, must equal the amount reported in FHWA Form 531, item C, Interfund transfers in.

The amount reported in item B, Interfund transfers out, must equal the amount reported in FHWA Form 531, item C, Interfund transfers in.

The amount shown in item D, Total funds to be accounted for, must equal the amount shown in in FHWA Form 531, item D, Total funds to be accounted for.

The amount shown in item D, Total funds to be accounted for, must equal the amount shown in in FHWA Form 531, item D, Total funds to be accounted for.

This section provides instructions on preparing two forms that focus on State transportation debt activities:

FHWA uses State-reported data to support the annual processing, compilation, development, and certification of national datasets, which are used to perform analysis of highway system investment needs and levels of investment, highway system user activities and revenue sources, and HTF transactions, including Federal-aid Highway Program funding apportionments to States.

FHWA also uses data from FHWA Form 541 and FHWA Form 542 to compile tables for the annual Highway Statistics publication. FHWA analysts and other analysts at the national and State levels use the data to forecast tax revenue, highway deterioration, and fuel consumption, to determine conformance with air quality standards, and to conduct multimodal design analysis and roadway safety analysis. FHWA Form 541 and FHWA Form 542 provide information about the amount and nature of annual bond financing for highways and mass transit, and on the change in debt during the year.

Highway finance tables are the basis of summaries that FHWA, the Department of Transportation (DOT), the Office of Management and Budget (OMB), Congress, and others rely on to develop national transportation policy and programs. For example, highway finance data is used in the report Status of the Nation’s Highways, Bridges and Transit: Conditions and Performance that the Secretary of Transportation is required to prepare and submit to Congress biennially (see 23 U.S.C. 502(g)).

Debt service payments for bond interest, redemption, allied costs, and the associated revenue are reported on FHWA Form 531 and FHWA Form 532 (see section 2.1 for instructions).

Instructions for FHWA Form 531 and FHWA Form 532 indicate that transactions relating to the refunding of obligations should be included and specifically noted. Refunding involves the replacement of one bond issue by another (see section 2.1).

Outstanding bonds are retired through refunding in one of two ways. In one method, a call notice is issued to redeem the outstanding bonds immediately. In another method, refunding bond proceeds are escrowed and invested to provide sufficient monies to make all remaining interest payments on the outstanding bonds and to retire them at their stated maturities. By either method, a refunded issue is assumed to have been retired during the current time period. Complete details of all refunding transactions should be given on the bond reports.

Obligations issued for a term of two or more years should be reported. Obligations for shorter terms should not be reported unless they are part of a regular bond issue, such as serial bonds for which the maturities begin the first year after issue.

Ordinary outstanding warrants and claims should not be reported as State transportation obligations, but interest on stamped warrants or similar obligations should be reported on FHWA Form 532 as debt service payments. When warrants, claims, or other short-term notes are funded, the obligations that replace them should be reported if they have been issued for a term of two or more years.

For zero-coupon or capital appreciation bonds, the par value of the bond reported on FHWA Form 541 and FHWA Form 542 should be the amount that the State will pay at maturity to retire the bonds. Zero coupon bonds pay no direct interest. Instead, they provide their return to investors by being sold at a large discount. The interest rate on the bonds is implied by the size of the discount and the term of the bond. Because FHWA Form 532 is prepared on a cash basis, rather than on an accrual basis, no interest expenditure is shown for a zero-coupon bond. The full amount of debt service on a zero-coupon bond will appear as a redemption expenditure. Therefore, the full amount that the State will have to pay to retire the bond at maturity should be reported on FHWA Form 542 as outstanding transportation debt.

Bonds should be classified and reported according to (1) the purpose of issue (such as highway, mass transit, or refunding) and (2) the type of security, as defined below:

Some States issue bonds to provide funds for multimodal capital projects. Because FHWA Form 531 and FHWA Form 532 include the financial transactions of State involvement in mass transit, bond transactions for such activities should be included on the bond reports. If specific allocations between highways and mass transit projects have not been made, estimates will suffice. These percentages should then be used to determine the amount of debt service payments to be assigned to highways and the amount to be assigned to mass transit. As subsequent issues are sold, the percentages should be revised to represent the totals assigned to highways and to mass transit, respectively. This approach will require fewer computations than using a separate percentage for each bond issue.

In multimodal issues with highway and other transportation allocations, the other transportation allotments, such as for airports, railroad, and marine, should be included in FHWA Form 541, item 9.B.

Airport, railroad, and marine bond issues are usually not considered highway or mass transit issues and are usually not reported on FHWA Form 541. For example, an airport bond that is for the construction of an airport tower and hangars should not be reported on FHWA Form 541. But when an airport, railroad, or marine bond issue funds a highway or mass transit project, that bond issue should be reported on FHWA Form 541. For example, an airport bond may fund highway and access improvements into the airport and an intermodal linkage to a mass transit system. However, only information for the allocation of proceeds to highways and mass transit should be reported on FHWA Form 531 and FHWA Form 532.

When special highway authorities, bond commissions, and so forth publish annual reports and audits, the reports usually contain enough data to identify transportation-related debt transactions and the amount of outstanding debt. Include these reports as supplementary debt service information when submitting 500-Series forms.

FHWA Form 541 is for reporting bond issues whose proceeds were used, in whole or in part, for highway and mass transit purposes. In general, bond issues sold during the year should be listed separately when issued under separate authorizations and statutory provisions or when carrying different issue dates.

FHWA Form 541 provides columns for States to identify and report transportation obligations issued by the State DOT or other reporting agency. The columns may also be used to report data by agency, function, or activity. If additional space is needed to account for more bonds, additional columns can be added to the form.

An explanation of each item in the form is provided in the following section.

This item is for identifying the legislation authorizing the issuance of the bond. Enter in each column the chapter, section number, and year of the law authorizing the bond issue.

This item is for reporting the total amount of dollars authorized under the statute. Record the total amount in dollars of bonds authorized under the statute, even when the entire amount has not been sold at the end of the current year. But if a State DOT does not receive the total amount authorized, the cumulative amount will show as smaller than total bonds authorized.

This item is for reporting the total cumulative amount of bonds sold to the end of the current year. Record the total cumulative amount of bonds sold to the end of the current year.

This item is for reporting the percentage of interest printed on the bonds. Record the rate or percentages of interest printed on the bonds.

This item identifies the source of funds for payment of debt service. Report the source of funds for payment of debt service. Sources of funds for debt service might include:

If a bond issue is secured by a pledge of full faith and credit of the State, even though debt service may be payable out of specific revenues, the issue should also be identified by the term "G.O.," for “general obligation.” When Federal funds are shown as the source of funds for debt service, the agency and amount of funds should be provided in a note.

This item is for reporting the date of issuance of a bond. Enter the nominal or official date of issuance of a bond. This is the date stated on the face of the bond. If the bond begins to bear interest on other than the nominal issuance date, information about when interest accrues should be provided in a note.

This item is for reporting the date of the bond sale. Record the actual date of sale. If bonds having one nominal date of issue are sold over a period of time, the word "various" should also be entered in item 7.

This item is for reporting the amount in dollars of proceeds from each bond sale. Record in this item the transaction information on each bond sale.

This item is for reporting the par value of each bond sold. The par value is the principal amount or amount found on the face of the bond.