- Potential Highway Capital Investment Impacts

- Types of Capital Spending Projected by HERS and NBIAS

- Alternative Levels of Future Capital Investment Analyzed

- Highway Economic Requirements System

- Impacts of Federal-Aid Highway Investments Modeled by HERS

- Impacts of NHS Investments Modeled by HERS

- Impacts of Interstate System Investments Modeled by HERS

- National Bridge Investment Analysis System

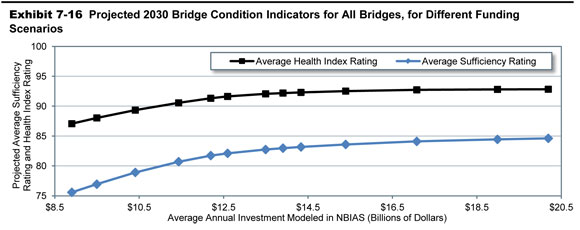

- Impacts of Systemwide Investments Modeled by NBIAS

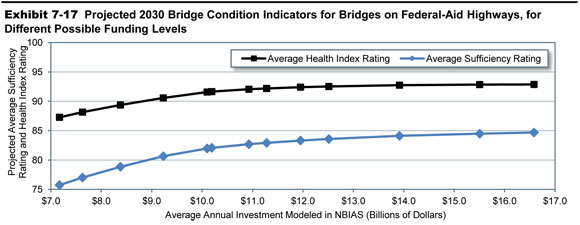

- Impacts of Federal-Aid Highway Investments Modeled by NBIAS

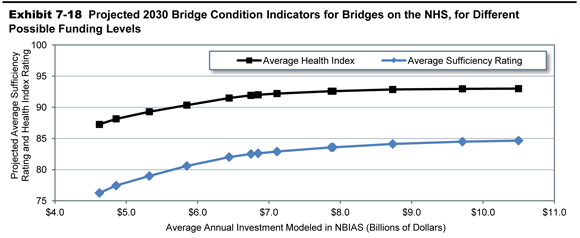

- Impacts of NHS Investments Modeled by NBIAS

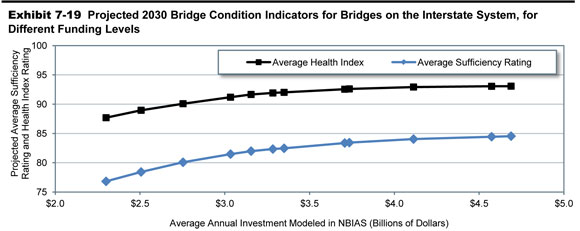

- Impacts of Interstate Investments Modeled by NBIAS

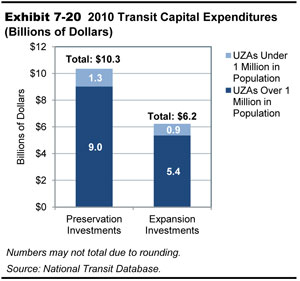

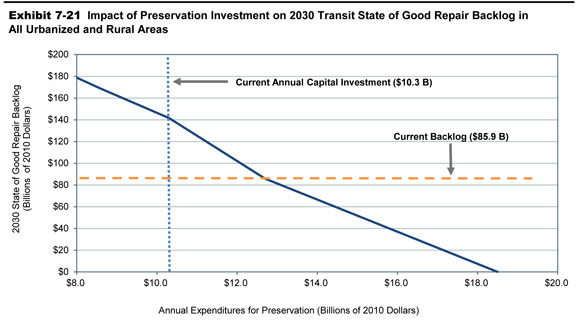

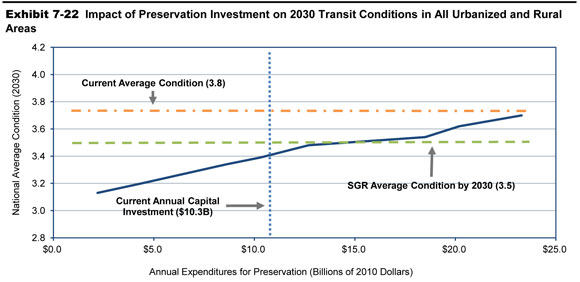

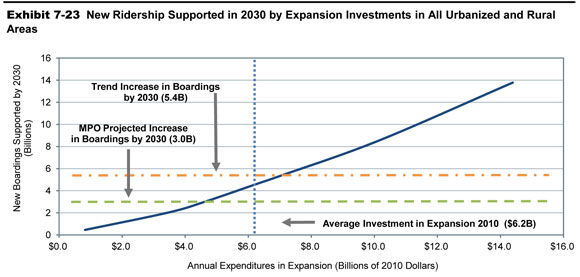

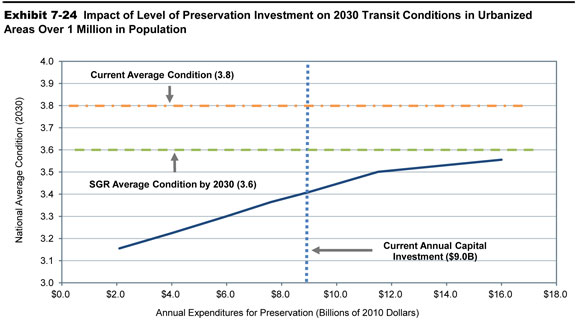

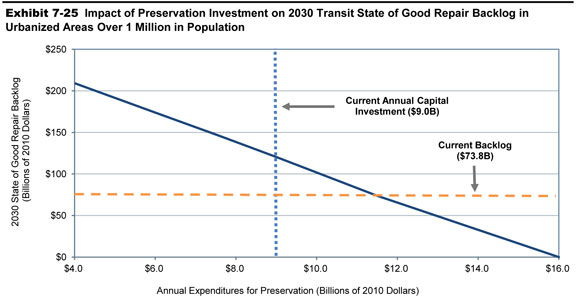

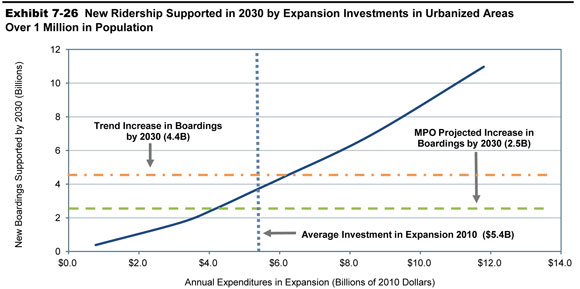

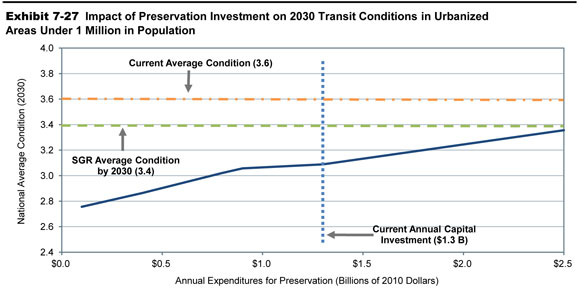

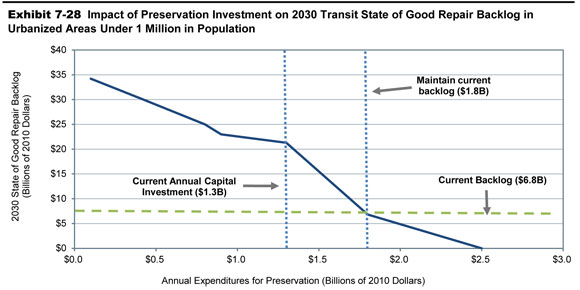

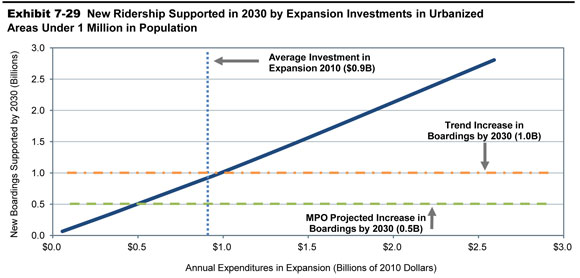

- Potential Transit Capital Investment Impacts

Potential Highway Capital Investment Impacts

The analyses presented in this section use a common set of assumptions to derive relationships between alternative levels of future highway capital investment and various measures of future highway and bridge conditions and performance. A subsequent section within this chapter provides comparable information for different types of potential future transit investments.

The analyses in this section focus on the types of investment within the scopes of the Highway Economic Requirements System (HERS) and the National Bridge Investment Analysis System (NBIAS), and form the building blocks for the capital investment scenarios presented in Chapter 8. The accuracy of the projections in this chapter depends on the validity of the technical assumptions underlying the analysis, some of which are varied in the sensitivity analysis in Chapter 10. The analyses presented in this section do not make any explicit assumptions regarding how future investment in highways might be funded.

Types of Capital Spending Projected by HERS and NBIAS

The types of investments evaluated by HERS and NBIAS can be related to the system of highway functional classification introduced in Chapter 2 and to the broad categories of capital improvements introduced in Chapter 6 (system rehabilitation, system expansion, and system enhancement). NBIAS relies on the NBI database, which covers bridges on all highway functional classes, and evaluates improvements that generally fall within the system rehabilitation category.

HERS evaluates pavement improvements—resurfacing or reconstruction—and highway widening; the types of improvements included in these categories roughly correspond to system rehabilitation and system expansion as described in Chapter 6. In estimating the per-mile costs of widening improvements, HERS recognizes a typical number of bridges and other structures that would need modification. Thus, the estimates from HERS are considered to represent system expansion costs for both highways and bridges. Coverage of the HERS analysis is limited, however, to Federal-aid highways, as the Highway Performance Monitoring System (HPMS) sample does not include data for rural minor collectors, rural local roads, or urban local roads.

The term “non-modeled spending” refers in this report to spending on highway and bridge capital improvements not evaluated in HERS or NBIAS; while these types of spending are absent from the analyses presented in this chapter, the capital investment scenarios presented in Chapter 8 are adjusted to account for them. Non-modeled spending includes capital improvements on highway classes omitted from the HPMS sample and hence the HERS model. Development of future investment scenarios for the highway system as a whole thus requires separate estimation outside the HERS modeling process.

Non-modeled spending also includes types of capital expenditures classified in Chapter 6 as system enhancements, which neither HERS nor NBIAS currently evaluate. Although HERS incorporates assumptions about future operations investments, whose capital components would be classified as system enhancements, the model does not directly evaluate the need for these deployments. In addition, HERS does not identify specific safety-oriented investment opportunities, but instead considers the ancillary safety impacts of capital investments that are directed primarily toward system rehabilitation or capacity expansion. This limitation of the model owes to the HPMS database containing no information on the location of crashes or of safety devices such as guardrails or rumble strips.

| How closely do the types of capital improvements modeled in HERS and NBIAS correspond to the specific capital improvement type categories presented in Chapter 6? | |

|

Exhibit 6-12 in Chapter 6 provides a crosswalk between a series of specific capital improvement types for which data are routinely collected from the States, and three major summary categories: system rehabilitation, system expansion, and system enhancement. The types of improvements covered by the HERS and NBIAS model are assumed to correspond with the system rehabilitation and system expansion categories. As in Exhibit 6-12, HERS splits spending on “reconstruction with added capacity” between these categories.

The assumed correspondence is close overall, but for some of the detailed categories in Exhibit 6-12 not exact. In particular, the extent to which HERS covers construction of new roads and bridges is ambiguous. While not directly modeled in HERS, such investments are often motivated by a desire to alleviate congestion on existing facilities in a corridor, and thus would be captured indirectly by the HERS analysis in the form of additional normal-cost or high-cost lanes. As described in Appendix A, the costs per mile assumed in HERS for high-cost lanes are based on typical costs of tunneling, double-decking, or building parallel routes, depending on the functional class and area population size for the section being analyzed. To the extent that investments in the “new construction” and “new bridge” improvement types identified in Chapter 6 are motivated by desires to encourage economic development or accomplish other goals aside from the reduction of congestion on the existing highway network, such investments would not be captured in the HERS analysis. Some other comparability issues include:

|

|

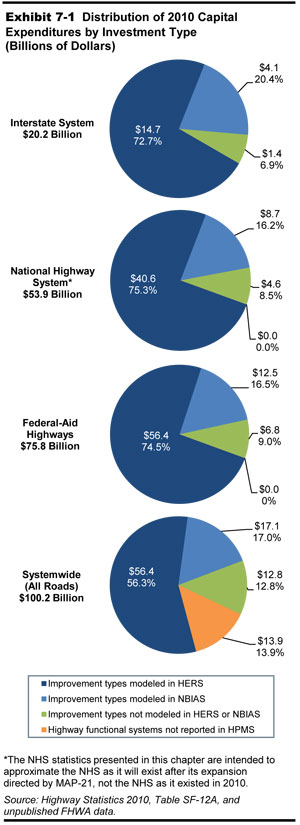

Exhibit 7-1 shows that systemwide in 2010, highway capital spending amounted to $100.2 billion, of which $56.4 billion went for types of improvements modeled in HERS and $17.1 billion for types of improvement modeled in NBIAS. The other $26.7 billion that went for non-modeled highway capital spending was divided fairly evenly between system enhancement expenditures and capital improvements to classes of highways not reported in HPMS.

Because the HPMS sample data are available only for Federal-aid highways, the percentage of capital improvements classified as non-modeled spending is lower for Federal-aid highways than is the case systemwide. Of the $75.8 billion spent by all levels of government on capital improvements to Federal-aid highways in 2010, 74.5 percent fell within the scope of HERS, 16.5 percent fell within the scope of NBIAS, and 9.0 percent was for spending captured by neither model. The percent distribution is similar for the Interstate Highway System.

It should be noted that the statistics presented in this chapter and Chapter 8 relating to future National Highway System (NHS) investment are based on an estimate of what the NHS will look like after it is expanded pursuant to MAP-21, rather than the system as it existed in 2010. As indicated in Chapter 6, combined highway capital spending by all levels of government on the NHS in 2010 totaled $44.4 billion. The $53.9 billion NHS spending figure referenced in Exhibit 7-1 includes amounts spent on other principal arterials, as much of this mileage will be added to the NHS.

|

Treatment of the NHS in 20-Year Projections Pursuant to MAP-21, the NHS will be expanded to include additional principal arterial and connector mileage that was not part of the original system. In light of this change, projecting future NHS investment needs over 20 years based on the system as it existed in 2010 would not produce particularly useful results. Rather than dropping the NHS projections from the C&P report series until such time as the system as the formal NHS re-designation is completed, this report includes projections based on an estimate of what the system would ultimately look like, by adding in principal arterials that are not currently part of the NHS. Once the revised NHS designations have been coded into the HPMS and NBI, future editions of this report will use them for all NHS-based analyses. |

Alternative Levels of Future Capital Investment Analyzed

The HERS and NBIAS analyses presented in this chapter each assumes that capital investment within the scope of the model will grow over the 20 years at a constant annual percentage rate, which could be positive, negative, or zero. The starting point for each analysis is the level of investment in 2010, which includes one-time funding under the American Recovery and Reinvestment Act of 2009 (Recovery Act). Because future levels are measured in constant 2010 dollars, the percent rates of growth are real (inflation-adjusted). This “ramped” approach to analyzing alternative investment levels was introduced in the 2008 C&P Report. Previous editions had either assumed a fixed amount would be spent in each year or set funding levels based on benefit-cost ratios, which tended to front-load the investment within the 20-year analysis period. Chapter 9 includes an analysis of the impacts on conditions and performance of these alternative investment timing patterns, as well as an example of how the ramping approach impacts year-by-year funding levels for some of the highway investment scenarios presented in Chapter 8.

This chapter provides a quantitative picture of potential highway and bridge system outcomes under alternative assumptions about the rate of ramped investment growth. The particular investment levels identified were selected from among the results of a much larger number of model simulations. Each investment level shown corresponds to a particular target outcome, such as funding all potential capital improvements with a benefit-cost ratio above a certain threshold or attaining a certain performance standard for highways or bridges. While each of the particular rates of change selected has some specific analytical significance, the analyses presented in this chapter do not constitute complete investment scenarios, but rather form the building blocks for such scenarios, which are presented in Chapter 8.

Highway Economic Requirements System

Simulations conducted with the HERS model provide the basis for this reports analysis of investment in highway resurfacing and reconstruction as well as for highway and bridge capacity expansion. HERS employs incremental benefit-cost analysis to evaluate highway improvements based on data from the HPMS. The HPMS includes State-supplied information on current roadway characteristics, conditions, and performance and anticipated future travel growth for a nationwide sample of more than 120,000 highway sections. HERS analyzes individual sample sections only as a step toward providing results at the national level; the model does not provide definitive improvement recommendations for individual sections.

Simulations with the HERS model start by evaluating the current state of the highway system using data from the HPMS sample. These data provide information on pavements, roadway geometry, traffic volume and composition (percent trucks), and other characteristics of the sampled highway sections. For sections with one or more deficiencies identified, the model then considers potential improvements, including resurfacing, reconstruction, alignment improvements, and widening or adding travel lanes. HERS selects the improvement (or combination of improvements) with the greatest net benefits, where benefits are defined as reductions in direct highway user costs, agency costs for road maintenance, and societal costs from vehicle emissions of greenhouse gases and other pollutants. (The model uses estimates of emission costs that include damage to property and human health and, in the case of greenhouse gases, certain other potential impacts such as loss of outdoor recreation amenities.) The model allocates investment funding only to the sections where at least one of the potential improvements are projected to produce benefits exceeding construction costs.

| How closely does the HERS model simulate the actual project selection processes of State and local highway agencies? | |

|

While the HERS model is a powerful tool for projecting future investment/performance relationships, the process of project selection in the model differs from reality in several respects. HERS assumes that the allocation of total national spending on highway investment will be “economically efficient,” meaning that the projects selected will be the set that maximizes total benefits to society. The model takes no account of the division of funding authority among States and localities. For example, it could program a large increase in highway investment in a State that lacks the needed budgetary resources. The model does not attempt to simulate the influence on project selection decisions of evaluation criteria other than economic efficiency, such as perceptions of fairness and political considerations. To the extent that these other factors shape the project selection decisions, HERS may underestimate the level of investment needed to achieve a given performance or conditions target, such as maintaining average pavement ride quality.

In addition, HERS lacks access to the full array of information that governments would need to determine what is economically efficient. It relies on the HPMS database, which provides only a limited amount of information on each sampled highway section. For example, while the HPMS includes information regarding the potential for adding lanes to each highway section, and obstacles to further widening, it does not currently include information on the feasibility of alternative approaches to added capacity in a given location (construction of parallel routes, double-decking, tunneling, investments in other transportation modes, etc.). This issue is discussed further in Appendix A. |

|

HERS normally considers highway conditions and performance over a period of 20 years from the base (“current”) year, which is the most recent year for which HPMS data are available. This analysis period is split into four funding periods of equal length. After HERS performs its analysis for the first funding period, it updates the database to reflect the influences of what is predicted to happen during the first period, including the effects of the selected highway improvements. The updated database is the foundation for the analysis of conditions and performance in the second period, and so on through the fourth and last period. Appendix A contains a more detailed description of the project selection and implementation process used by HERS.

HPMS Database

The analyses presented in the 2010 C&P report relied on the 2008 HPMS database. The HPMS has subsequently been significantly modified, incorporating major changes in database structure and data items. These changes emerged from a comprehensive reassessment of how well the database was meeting user and customer needs; for details, see the HPMS Reassessment 2010+ Final Report issued in September 2008.

Changes to the HPMS

The new HPMS structure organizes data into program areas and links them together through a Geographic Information System (GIS) using spatial relationships. The revised procedures include those for creating the statistical population of highway sections from which the HPMS sample is drawn (to better ensure homogeneity over each section’s length with respect to traffic volume, number of through lanes, and other key variables) and those for averaging or summarizing measures from which different values have been estimated over a section’s length (e.g., for pavement roughness). A number of new data items have been added to the HPMS, particularly in regards to pavement characteristics and different types of pavement distresses, which are intended to support more robust analysis of pavement performance in HERS. Another key change from the HERS perspective was the replacement of an old data item regarding widening feasibility with two new items intended to provide more specific information on widening potential in terms of the specific number of lanes that could be added to a given location and obstacles to further widening; these data items are intended to support more robust analysis of widening alternatives. Appendix D discusses possible enhancements to HERS to make use of new data items on highway ramps and on measures of pavement distress other than pavement roughness.

Assessment of 2010 HPMS Sample Database’s Suitability for HERS

With the data requirements for the C&P report in mind, the initial timetable for the HPMS reassessment implementation called for States to start submitting data in the new format for the 2009 data year, in the hopes that any problems with the changeover could be addressed and resolved in time for the 2010 data submittal. However, the timetable was delayed, and only 15 States reported using the new HPMS format in 2009; for most States, 2010 was the first year in which they submitted data items under the new format.

The initial Federal Highway Administration (FHWA) data reviews conducted on the 2010 HPMS data focused on addressing issues pertaining to the types of statistics on current system characteristics and system conditions that are presented in Chapters 2 and 3. While these national-level data are considered reasonably reliable, subsequent examination of the more detailed HPMS sample data identified a large number of omissions and seemingly implausible coding for some individual items and for some combinations of data reported in different fields. Of particular concern were the large numbers of:

- Blank entries for both the International Roughness Index (IRI) and Present Serviceability Rating (PSR)

- Blank entries for pavement surface type or inconsistent entries relative to what is coded in other fields

- Miscoded responses for widening potential (at most, 20 States coded the field correctly)

- Seemingly implausible entries for the numbers of peak, counterpeak, and total lanes relative to each other

- Missing entries for single unit and combination truck traffic.

The data omissions in particular present a problem for the HERS model, which relies on having a completely populated sample data set for each individual sample record that it analyzes. In order to make use of the 2010 HPMS data, a significant effort was undertaken to impute logical values for some of the omitted data, and to develop additional screens to adjust apparent data outliers. Based on these procedures, a modified data set was then tested in HERS. This testing found anomalies in the pavement performance analysis; this was not wholly unexpected, as this was the first full national-level test of both new pavement data items and new pavement performance models that had been introduced into HERS to take advantage of these data. More puzzling were anomalies in the operational performance analysis, as these aspects of HERS had not been significantly modified, so that the changes in results could be attributed solely to the HPMS data.

In light of these issues, the FHWA has determined that for the purposes of this report, the 2008 HPMS sample data would serve as a better proxy for the “current” conditions and performance of the highway system than would the 2010 HPMS sample data set in its present form. Based on this decision, the analyses presented in this report have been developed using an older version of HERS very similar to that used for the 2010 C&P report, rather than utilizing the newer version of HERS that is customized for use with the new HPMS data format.

The FHWA will be working with the States to address issues with the HPMS sample data reporting to improve its utility for supporting future editions of the C&P report. As States become more familiar with the new HPMS data structure and data fields over time, the completeness and quality of the data should improve. To the extent that the modified HPMS structure facilitates the reporting of better data, some degree of inconsistency with the data reported in previous years can be expected.

Implications of Database Selection

Although this edition uses the same 2008 HPMS database as was used in the 2010 C&P report, other input variables were updated from 2008 to 2010, resulting in significantly different projections than those presented in the 2010 C&P report. Base-year values were updated to 2010 for prices and unit costs, average vehicle fuel efficiency, vehicle emission rates, and the level on highway investment (for runs that assume highway investment to remain at the base-year level in constant dollars). Inputs in the form of projections for fuel efficiency and vehicle emissions rates were updated to the analysis period used throughout Part II of this report, 2011-2030.

On the basis of these updates, this report considers the base year for the HERS analyses to be 2010 and the projection period to be the subsequent two decades through 2030. However, the reliance on the 2008 HPMS database should be borne in mind when interpreting the exhibits in this and following chapters. Except as noted, the base year values reported for conditions and performance indicators are actually HERS-computed values for 2008 serving as proxies for 2010 values.

Operations Strategies

Starting with the 2004 C&P report, the HERS model has considered the impacts of certain types of highway operational improvements, in which intelligent transportation systems (ITS) feature prominently. The types of strategies currently evaluated by HERS include:

- Freeway management (ramp metering, electronic roadway monitoring, variable message signs, integrated corridor management, variable speed limits, queue warning systems, lane controls)

- Incident management (incident detection, verification, and response)

- Arterial management (upgraded signal control, electronic monitoring, variable message signs)

- Traveler information (511 systems and advanced in-vehicle navigation systems with real-time traveler information).

Appendix A describes these strategies in more detail and their treatment in the HERS model. It is important to note that HERS does not subject these types of investments to benefit-cost analysis and does not directly analyze tradeoffs between them and the pavement improvements and widening options also considered by the model. Instead, operations strategies are modeled via a separate preprocessor that estimates their impact on the performance of highway sections where they are deployed. The analyses presented in this chapter assume a package of investments representing the continuation of existing deployment trends, while a sensitivity analysis presented in Chapter 10 considers the impacts of a more aggressive deployment pattern. HERS does not currently model various applications of vehicle-to-vehicle and vehicle-to-infrastructure communications that are under development because it is too early to reliably predict their impacts and patterns of deployment.

| How will Vehicle-to-Vehicle (V2V) and Vehicle-to-Infrastructure (V2I) communications potentially impact future investment needs? | |

|

Cellular, Wi-Fi, and other dedicated short-range communication technologies are expanding the possibilities for a Connected Vehicle Environment. Communications among vehicles on the road (V2V), and between these vehicles and infrastructure (V2I) hold promise for substantial reductions in crashes and vehicle emissions, and enhanced mobility through more efficient transportation systems management and operations. Adding to this potential are rapid advances in vehicle automation. For example, under advanced speed harmonization, vehicle speed would adjust automatically to speed limits that vary based on road, traffic, and weather conditions (an existing V2I application).

Additional examples of connectivity applications include blind spot monitoring/lane change warning, smart parking, forward collision warning, do-not-pass warning, curve speed warning, red light violation warning, transit pedestrian warning, cooperative adaptive cruise control, breaking assist, and dynamic lane closure management. To reach the full potential of connected vehicles will require investment, coordination, and partnership with public and private entities. As development and implementation of connected vehicle applications proceeds, additional information should make possible their representation in HERS. Research efforts by FHWA, FTA, NHTSA, AASHTO and others that will measure benefits and costs of these applications include: (1) Applications for the Environment: Real-Time Information Synthesis (AERIS) Program; (2) AASHTO Connected Vehicle Field Infrastructure Footprint Analysis; (3) Connected and Automated Vehicle Benefit Cost Analysis; and (4) Measuring Local, Regional and Statewide Economic Development Associated with the Connected Vehicle program. |

|

HERS Treatment of Traffic Growth

For each HPMS sample highway section, States provide the actual traffic volume in the base year and a forecast of traffic volume for a future year, based on available information concerning the particular section and the corridor of which it is a part. These forecasts are interpreted by HERS as having been made under the assumption that the average user cost per mile of travel, including costs of travel time, vehicle operation, and crash risk, would remain unchanged over the 20-year analysis period.

Because the present HERS analysis uses the HPMS sample data for 2008, the traffic volumes for the base and forecast years pertain to 2008 and 2028. In the 2008 database, the composite weighted average annual VMT growth rate between the 2008 base year and the forecast year is 1.85 percent. Projected VMT growth in rural areas averages 2.15 percent per year, somewhat higher than the average of 1.70 percent in urban areas.

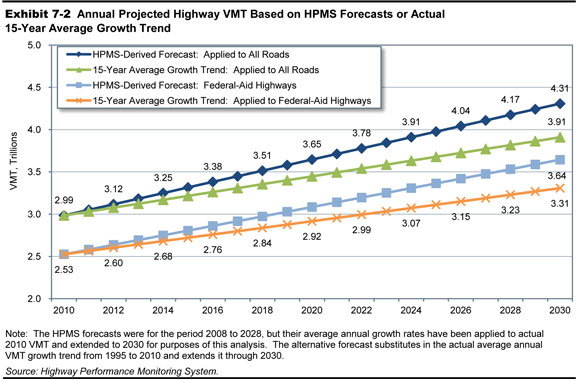

To allow for the possibility that future traffic growth will be lower than forecast in the HPMS, the HERS analysis presented in this report considers an alternative in which VMT grows at the trend rate of 1.36 percent per annum that prevailed from 1985 to 2010. In this case, the section-level forecasts of VMT from the HPMS are reduced in uniform proportion to bring the growth rate of VMT down to this level from the 1.85 percent assumed in the baseline. Exhibit 7-2 applies the alternative forecast growth rates, 1.36 percent and 1.85 percent, to actual Federal-aid highway and systemwide VMT for 2010 to derive year-by-year estimates through 2030. An underlying assumption is that VMT will grow in a linear fashion (so that 1/20th of the additional VMT is added each year), rather than geometrically (growing at a constant annual rate). With linear growth, the annual percent rate of growth gradually declines over the forecast period.

| What are some of the technical limitations associated with the analysis of alternative trend-based travel growth rates included in this section? | |

|

One of the strengths of the State-provided VMT forecasts used in the baseline analysis is their geographic specificity. Separate forecasts are provided for the more than 100,000 HPMS sample sections. The 1.85 percent average annual VMT growth rate referenced as the “forecast VMT growth” in this section reflects a compilation of these forecasts for individual sample sections.

In forming their section-specific forecasts, States can take account of specific local influences on travel growth and their own long-range planning assumptions about future travel patterns on particular routes or corridors. The inclusion of these section-level forecasts, as opposed to regional or statewide travel estimates, allows for more refined analyses of projected future investment/performance relationships. The analyses based on the alternative “trend VMT growth”, adjust the HPMS-derived forecasts for the next 20 years to match the 15-year trend from 1995 to 2010 when average VMT increased at an average annual rate of 1.36 percent. These analyses use a top-down, rather than a bottom-up approach; while they use the HPMS forecasts for individual highway sections as a starting point, these forecasts are adjusted downward in uniform proportion on a national basis. In reality, if VMT were to grow more slowly than the State projections, these differences would not be uniform, and could be heavily concentrated in particular corridors, regions, or States. Moreover, these differences could significantly impact the level of investment that might be required to achieve particular systemwide performance targets. The assumption of uniformity thus limits the reliability of this section’s analysis of the trend-based alternative VMT growth rates. |

|

Travel Demand Elasticity

One of the key features of the economic analysis in HERS is the influence of the cost of travel on the demand for travel. HERS represents this relationship as a travel demand elasticity that relates demand, measured by VMT, to average user cost per VMT. The model applies this elasticity to the forecasts of future travel (VMT) found in the HPMS sample data, which are interpreted as constant user cost forecasts. Any change that HERS projects in user cost relative to the base-year level will, through the mechanism of the travel demand elasticity, affect the model’s projection for future travel growth. For any highway investment scenario that predicts average user cost to decrease, the projected growth rate will be higher than the baseline rate derived from HPMS. The demand for travel induced by the reduction in cost could arise from various traveler responses in various ways—for example, changing route or mode of travel, or even the total amount of travel undertaken. Conversely, for scenarios in which highway user cost increases, the projected VMT growth rate will tend to be lower than the baseline rate.

HERS also allows the induced demand predicted through the elasticity mechanism to influence the cost of travel to highway users. On congested sections of highway, the initial congestion relief afforded by an increase in capacity will reduce the average user cost per VMT, which in turn will stimulate demand for travel and this increased demand will reverse a portion of the initial congestion relief. The elasticity feature operates likewise with respect to improvements in pavement quality by allowing for induced traffic that adds to pavement wear. (Conversely, an initial increase in user costs can start a causal chain with effects in the opposite direction). By capturing these offsets to initial impacts on highway user costs, HERS is able to estimate the net impacts.

Impacts of Federal-Aid Highway Investments Modeled by HERS

The present HERS analysis starts with an evaluation of the state of Federal-aid highways in the 2010 base year. Exhibit 7-1 showed that capital spending on these highways for the types of improvements modeled in HERS then amounted to $56.4 billion (out of total highway capital spending of $100.2 billion). The analysis next goes on to consider the potential impacts on system performance of raising or lowering the amount of investment within the scope of HERS at various annual rates over 20 years. Spending in any year is measured in constant 2010 dollars, so that spending and its rate of growth are both measured in real rather than nominal terms. Chapter 9 includes an illustration of how future spending levels could be converted from real to nominal dollars levels under alternative assumptions about the future inflation rate.

Selection of Investment Levels for Analysis

Exhibit 7-3 describes the significance of the 10 funding levels selected for presentation in this chapter. Some of these funding levels over the 20-year analysis period are geared toward the attainment of a specific minimum value over that period for the benefit-cost ratio (BCR). As explained in the introduction to Part II of this report, HERS ranks potential projects in order of BCR and implements them until the funding constraint is reached. The lowest BCR among the projects selected, the “marginal BCR” will vary across the four funding periods, and HERS refers to the lowest of these values across the funding periods as the “minimum BCR”. For each minimum BCR target, 1.0 or 1.5, the requisite amount of investment is determined under the alternative baseline assumptions about the future growth rate of VMT: the HPMS forecast rate (1.85 percent per annum) or the historical trend rate (1.36 percent per annum). The highest level of spending shown in Exhibit 7-3 corresponds to the annual growth rate in real spending, 3.95 percent, associated with a minimum BCR of 1.0 in the forecast VMT growth case. The attainment of this minimum BCR can be interpreted as having implemented all potentially cost-beneficial projects (BCR≥1.0). The next highest level of spending shown in Exhibit 7-3 is the estimate of what would achieve this target assuming trend-based VMT growth and averages $70.5 billion per year, which is about 18 percent less than in the forecast-based VMT growth case ($86.9 billion per year).

| HERS-Modeled Capital Investment | Minimum BCR 2 | Funding Level Description Assuming Future VMT Growth Consistent With HPMS Forecast ("Forecast") or Consistent with VMT Growth Trend "(Trend)" | ||||

|---|---|---|---|---|---|---|

| Annual Percent Change in Spending |

Average Annual Spending (Billions of 2010 Dollars) Total 1 | Assuming Forecast VMT Growth3 |

Assuming Trend VMT Growth4 | |||

| 3.95% | $86.9 | 1.00 | – | Minimum BCR=1.0 (Forecast) | ||

| 2.08% | $70.5 | 1.42 | 1.00 | Minimum BCR=1.0 (Trend) | ||

| 1.71% | $67.8 | 1.50 | 1.06 | Minimum BCR=1.5 (Forecast) | ||

| 0.72% | $60.9 | 1.73 | 1.27 | Average Delay per VMT in 2030 Matches 2010 Level (Forecast) | ||

| 0.00% | $56.4 | 1.92 | 1.42 | Constant Dollar Investment Sustained at 2010 Level | ||

| -0.32% | $54.6 | 2.01 | 1.50 | Minimum BCR=1.5 (Trend) | ||

| -0.66% | $52.7 | 2.09 | 1.58 | Average Speed in 2030 Matches 2010 Level (Forecast) | ||

| -0.95% | $51.1 | 2.17 | 1.64 | “Cost to Maintain” (Forecast) 5 | ||

| -2.62% | $43.2 | 2.64 | 2.08 | Average IRI in 2030 Matches 2010 Level (Forecast) | ||

| -4.60% | $35.7 | 2.83 | 2.53 | “Cost to Maintain” (Trend) 5 6 | ||

2 The minimum BCR represents the lowest benefit-cost ratio for any project implemented by HERS during the 20-year analysis period at the level of funding shown.

3 The “Forecast” VMT growth is computed by comparing the current average annual daily traffic (AADT) with the future AADT that are reported by the States for individual HPMS sample sections; nationally this comes out to an average annual growth rate of 1.85% . HERS assumes this represents the VMT that would occur at a constant price (i.e., highway user costs do not increase or decrease), but adjusts the growth for individual sections during its analysis in response to changes in user costs.

4 The average annual growth rate assumed in the “Trend” VMT growth analyses is 1.36%, matching the average growth rate for the 15-year period from 1995 to 2010. To implement this assumption, the future AADT values reported for each HPMS sample section in HPMS were proportionally reduced; the resulting values were assumed to be the VMT that would occur at a constant price.

5 The “Cost to Maintain” represents the average of the investment levels associated with maintaining average delay per VMT and maintaining IRI, and is used in the “Maintain Conditions and Performance” investment scenarios in Chapter 8.

6 Assuming VMT growth follows its 15-Year Trend, the annual percent change in spending at which average delay per VMT in 2030 matches the 2010 level is negative 4.61 percent, while the annual rate of spending change at which average IRI in 2030 matches the 2010 level is negative 4.60 percent. Since these values are so close, their investment levels are not identified separately, and the “Cost to Maintain” is defined around an annual change of negative 4.60 percent.

Other funding levels shown in Exhibit 7-3 are geared toward achieving a specific level of performance for a particular indicator for 2030—average congestion delay per VMT, average speed, or the average IRI. For each such indicator, the requisite amount of investment to maintain the base-year level is shown for the forecast-based VMT growth case. Shown for the cases of both forecast-based and trend-based VMT, growth is the “Cost to Maintain,” which is the average of the investment levels associated with maintaining the congestion delay and pavement roughness indicators. (Separate values are not shown for the investment levels associated with maintaining average delay per VMT and maintaining average IRI in the trend-based VMT growth case, as coincidentally they are virtually identical). In the trend-based VMT growth case, this level of investment averages $35.7 billion per year, the lowest amount shown in Exhibit 7-3, and associated rate with negative 4.3-percent annual growth in investment. (The connections between funding growth rates and performance indicators are identifiable from the exhibits presented later in this section).

The other rate of investment growth in Exhibit 7-3 is zero, for the case where average annual spending over 2010–2030 remains at the actual level of spending in 2010 in constant dollar terms.

| Why are many of the spending growth rates associated with meeting performance targets negative in this report, when they were positive in the 2010 C&P report? | |

|

Actual highway capital investment for capital improvements modeled in HERS rose from $54.7 billion in 2008 (base year for the 2010 C&P report) to $56.4 billion in 2010, a 3 percent increase in nominal dollar terms. However, this coincided with a steep drop in highway construction costs, estimated in this report to have been about 18 percent. Factoring in this price change, real spending within the scope of HERS is estimated to have increased between 2008 and 2010 by almost 26 percent. This does much to explain why the present analysis indicates that maintaining target performance indicators at their base-year levels would be consistent with spending less than in the base year, whereas the analysis presented in the 2010 C&P report indicated that spending more than in the base year would be required.

It should also be noted that 2010 highway capital investment was supplemented by one-time funding under the Recovery Act, which would make it more challenging to sustain this level of investment in the future. |

|

Investment Levels and BCRs by Funding Period

Exhibit 7-4 illustrates how the 10 alternative funding growth rates for Federal-aid highways that were selected for further analysis in this chapter would translate into cumulative spending in 5-year intervals (corresponding to 5-year analysis periods used in HERS), along with the marginal benefit-cost ratios associated with that investment. The marginal BCR is generally higher for earlier than for later subperiods, resulting in the minimum BCR over the entire analysis period, shown in the last column, equaling the marginal BCR in the last subperiod. This pattern reflects the tendency in HERS for implementing the most worthwhile improvements first. The exception to this pattern occurs when funding is assumed to decline at an annual real rate of negative 2.62 percent or more; in this case, the relative scarcity of funding toward the end of the analysis period limits what can be implemented to relatively high-return projects.

| Annual Percent Change in HERS Capital Spending | Spending Modeled in HERS (Billions of 2010 Dollars) | Marginal BCR 2 |

Minimum BCR 20-Year 2011 to 2030 | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Cumulative 5-Year 2011 to 2015 |

Cumulative 5-Year 2016 to 2020 |

Cumulative 5-Year 2021 to 2025 |

Cumulative 5-Year 2026 to 2030 |

Cumulative 5-Year 2011 to 2030 | Average Annual Spending Over 20 Years 1 | 5-Year 2011 to 2015 | 5-Year 2016 to 2020 | 5-Year 2021 to 2025 | 5-Year 2026 to 2030 | ||

| Assuming Forecast VMT Growth | |||||||||||

| 3.95% | $317 | $385 | $468 | $568 | $1,738 | $86.9 | 2.30 | 1.73 | 1.30 | 1.00 | 1.00 |

| 2.08% | $300 | $333 | $369 | $409 | $1,411 | $70.5 | 2.40 | 1.97 | 1.63 | 1.42 | 1.42 |

| 1.71% | $297 | $323 | $352 | $383 | $1,355 | $67.8 | 2.42 | 2.03 | 1.70 | 1.50 | 1.50 |

| 0.72% | $288 | $299 | $310 | $321 | $1,218 | $60.9 | 2.47 | 2.17 | 1.89 | 1.73 | 1.73 |

| 0.00% | $282 | $282 | $282 | $282 | $1,129 | $56.4 | 2.51 | 2.28 | 2.04 | 1.92 | 1.92 |

| -0.32% | $279 | $275 | $271 | $266 | $1,092 | $54.6 | 2.54 | 2.33 | 2.10 | 2.01 | 2.01 |

| -0.66% | $277 | $268 | $259 | $250 | $1,054 | $52.7 | 2.56 | 2.39 | 2.17 | 2.09 | 2.09 |

| -0.95% | $274 | $261 | $249 | $238 | $1,023 | $51.1 | 2.58 | 2.43 | 2.24 | 2.17 | 2.17 |

| -2.62% | $261 | $228 | $200 | $175 | $864 | $43.2 | 2.68 | 2.72 | 2.64 | 2.72 | 2.64 |

| -4.60% | $246 | $194 | $153 | $121 | $714 | $35.7 | 2.83 | 3.12 | 3.18 | 3.38 | 2.83 |

| Assuming Trend VMT Growth | |||||||||||

| 2.08% | $300 | $333 | $369 | $409 | $1,411 | $70.5 | 2.18 | 1.66 | 1.22 | 1.00 | 1.00 |

| 1.71% | $297 | $323 | $352 | $383 | $1,355 | $67.8 | 2.20 | 1.71 | 1.28 | 1.06 | 1.06 |

| 0.72% | $288 | $299 | $310 | $321 | $1,218 | $60.9 | 2.27 | 1.84 | 1.44 | 1.27 | 1.27 |

| 0.00% | $282 | $282 | $282 | $282 | $1,129 | $56.4 | 2.32 | 1.93 | 1.57 | 1.42 | 1.42 |

| -0.32% | $279 | $275 | $271 | $266 | $1,092 | $54.6 | 2.34 | 1.98 | 1.64 | 1.50 | 1.50 |

| -0.66% | $277 | $268 | $259 | $250 | $1,054 | $52.7 | 2.36 | 2.03 | 1.70 | 1.58 | 1.58 |

| -0.95% | $274 | $261 | $249 | $238 | $1,023 | $51.1 | 2.38 | 2.07 | 1.75 | 1.64 | 1.64 |

| -2.62% | $261 | $228 | $200 | $175 | $864 | $43.2 | 2.49 | 2.33 | 2.10 | 2.08 | 2.08 |

| -4.60% | $246 | $194 | $153 | $121 | $714 | $35.7 | 2.62 | 2.67 | 2.53 | 2.63 | 2.53 |

2 The marginal BCR represents the lowest benefit-cost ratio for any project implemented during the period identified at the level of funding shown. The minimum BCRs, indicated by bold font and also shown in the last column, are the smallest of the marginal BCRs across the funding periods.

As shown in Exhibit 7-4, achieving a minimum BCR of 1.0 is estimated to require $1.738 trillion over the analysis period when forecast VMT growth is assumed and about $1.411 trillion when trend VMT growth is assumed. Applying the more restrictive minimum BCR target of 1.50 would require, respectively, 15 percent and 20 percent less than these amounts ($1.355 trillion and $1.092 trillion over the analysis period).

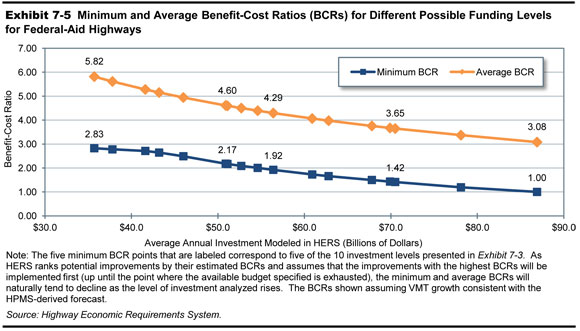

Further evident in Exhibits 7-3 and 7-4 is the inverse relationship described in the introduction to Part II between the minimum BCR and the level of investment. Exhibit 7-5 graphs this inverse relationship, as well as that between the average BCR and the level of investment. At any given level of average annual investment, the average BCR always exceeds the marginal BCR. For example, at the lowest level of investment considered, $714 billion over 20 years, the average BCR of 5.82 exceeds the minimum BCR of 2.83, assume forecast VMT growth.

Impact of Future Investment on Highway Pavement Ride Quality

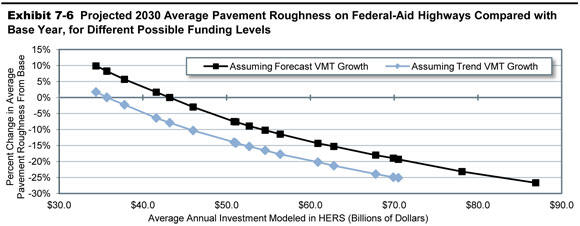

The primary measure in HPMS of highway physical condition is pavement ride quality as measured by the IRI index of pavement roughness (defined in Chapter 3). The HERS analysis presented in this report focuses on VMT-weighted IRI values; the average IRI values shown thus reflect the pavement ride quality experienced on a typical mile of travel. Exhibit 7-6 shows how the projection for the average IRI on Federal-aid highways in 2030 varies with the total amount of HERS-modeled investment and between the assumptions regarding VMT growth. Also shown is the portion of investment that HERS allocates to system rehabilitation, which is more significant than investment in system expansion in influencing average pavement ride quality.

| HERS-Modeled Capital Investment | Projected Impacts on Federal-Aid Highways 3 Average IRI (VMT-Weighted) | |||||||

|---|---|---|---|---|---|---|---|---|

| Annual Percent Change in Spending |

Average Annual Spending (Billions of 2010 Dollars) Total 1 | Average Annual Spending (Billions of 2010 Dollars) System Rehabilitation 2 If Forecast VMT Growth |

Average Annual Spending (Billions of 2010 Dollars) System Rehabilitation 2 |

Projected 2030 Level If Forecast VMT Growth |

Projected 2030 Level If Trend VMT Growth | Percent Change Relative to Base Year If Forecast VMT Growth | Percent Change Relative to Base Year If Trend VMT Growth |

|

| 3.95% | $86.9 | $43.9 | – | 83.9 | – | -26.7% | – | |

| 2.08% | $70.5 | $36.7 | $40.6 | 92.3 | 85.7 | -19.3% | -25.1% | |

| 1.71% | $67.8 | $35.6 | $39.3 | 93.8 | 87.0 | -18.0% | -24.0% | |

| 0.72% | $60.9 | $32.6 | $35.8 | 98.0 | 91.3 | -14.3% | -20.2% | |

| 0.00% | $56.4 | $30.6 | $33.6 | 101.3 | 94.1 | -11.5% | -17.7% | |

| -0.32% | $54.6 | $29.7 | $32.6 | 102.7 | 95.5 | -10.2% | -16.5% | |

| -0.66% | $52.7 | $28.9 | $31.6 | 104.2 | 96.9 | -8.9% | -15.3% | |

| -0.95% | $51.1 | $28.1 | $30.8 | 105.7 | 98.1 | -7.6% | -14.2% | |

| -2.62% | $43.2 | $24.2 | $26.6 | 114.4 | 105.4 | 0.0% | -7.9% | |

| -4.60% | $35.7 | $20.6 | $22.6 | 123.8 | 114.4 | 8.2% | 0.0% | |

| Base Year Value: | 114.4 | |||||||

2 The amounts shown represent the portion of HERS-modeled spending directed toward system rehabilitation, rather than system expansion, which is influenced by the assumption made about future VMT growth rates.

3 The HERS model relies on information from the HPMS sample section database, which is limited to those portions of the road network that are generally eligible for Federal funding (i.e., “Federal-aid highways”) and excludes roads classified as rural minor collectors, rural local, and urban local.

For each of the funding levels analyzed, HERS would direct a greater share of total spending toward system rehabilitation assuming the trend rate of VMT growth (1.36 percent per annum) rather than the forecast rate of VMT growth (1.85 percent per annum). The lower VMT under the trend growth case also results in less pavement damage from traffic. Consequently, for any given level of investment in Federal-aid highways, Exhibit 7-6 indicates the average IRI projected for 2030 to be lower in the trend than in the forecast case. For example, assuming that real investment in highways remains at the 2010 base year level of $56.4 billion, the projection is for the average IRI to decline by 17.7 percent to 94.1 in the trend VMT growth case, while it would only decline by 11.5 percent to 101.3 for the forecast VMT growth case.

For almost all combinations of investment level and traffic growth that Exhibit 7-6 presents, pavements on Federal-aid highways are projected to be smoother on average in 2030 than in 2010. The exception combines spending declining at an average annual rate of 4.6 percent with traffic growing at the forecast rate (1.85 percent per annum). For those circumstances, HERS projects an 8.2-percent increase in average pavement roughness. The same rate of decline in spending combined with the trend rate of traffic growth (1.36 percent per annum) is projected to maintain the average IRI at the base year level. The rate of spending growth that would maintain average IRI at the 2010 level case is higher when traffic is assumed to grow at the forecast rate, but still negative (-2.62 percent per annum).

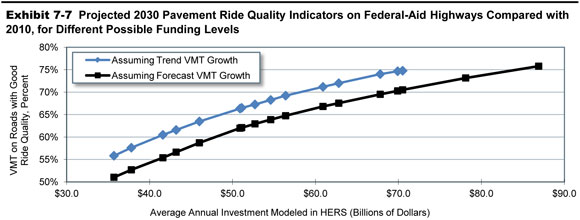

Exhibit 7-7 shows the HERS projections for the percentage of travel occurring on pavements with ride quality that would be rated good or acceptable based on the IRI thresholds set in Chapter 3. Under all circumstances represented in the exhibit, the 2030 projection for the percent of travel occurring on pavements with good ride quality exceeds the 50.6 percent that occurred in 2010. With traffic assumed to grow at the forecast rate, the projection for 2030 ranges from 75.8 percent at the highest level of investment modeled, which implements all projects with BCR≥1.0, to 51.0 percent at the lowest level, which would reduce investment at an average annual rate of 4.6 percent. When zero change from the 2010 level of investment is modeled, the projections for 2030 in the forecast growth case are for pavements with good ride quality to carry 64.7 percent of travel. In the trend traffic case, the corresponding projections are 4 to 5 percentage points higher, reflecting the greater share of investment directed toward system rehabilitation.

| HERS-Modeled Capital Investment | Projected Impacts on Federal-Aid Highways | ||||||

|---|---|---|---|---|---|---|---|

| Annual Percent Change in Spending | Average Annual Spending (Billions of 2010 Dollars) Total | Average Annual Spending (Billions of 2010 Dollars) System Rehabilitation If Forecast VMT Growth | Average Annual Spending (Billions of 2010 Dollars) System Rehabilitation If Trend VMT Growth |

Percent of 2030 VMT on Roads With IRI<95 (Good Ride Quality)1 If Forecast VMT Growth |

Percent of 2030 VMT on Roads With IRI<95 (Good Ride Quality)1 If Trend VMT Growth |

Percent of 2030 VMT on Roads With IRI<170 (Acceptable Ride Quality)1 If Forecast VMT Growth | Percent of 2030 VMT on Roads With IRI<170 (Acceptable Ride Quality)1 If Trend VMT Growth |

| 3.95% | $86.9 | $43.9 | – | 75.8% | – | 93.4% | – |

| 2.08% | $70.5 | $36.7 | $40.6 | 70.5% | 74.8% | 90.8% | 93.1% |

| 1.71% | $67.8 | $35.6 | $39.3 | 69.5% | 74.0% | 90.4% | 92.6% |

| 0.72% | $60.9 | $32.6 | $35.8 | 66.8% | 71.2% | 89.1% | 91.3% |

| 0.00% | $56.4 | $30.6 | $33.6 | 64.7% | 69.2% | 88.1% | 90.3% |

| -0.32% | $54.6 | $29.7 | $32.6 | 63.9% | 68.3% | 87.6% | 89.9% |

| -0.66% | $52.7 | $28.9 | $31.6 | 62.9% | 67.3% | 87.2% | 89.5% |

| -0.95% | $51.1 | $28.1 | $30.8 | 62.1% | 66.5% | 86.7% | 89.1% |

| -2.62% | $43.2 | $24.2 | $26.6 | 56.6% | 61.6% | 84.0% | 86.8% |

| -4.60% | $35.7 | $20.6 | $22.6 | 51.0% | 55.8% | 81.5% | 84.0% |

| Base Year Values 2: | 50.6% | 82.0% | |||||

2 Base Year values shown are 2010 values reported in Chapter 3, rather than those reflected in the 2008 HPMS sample dataset.

In almost all the circumstances considered, Exhibit 7-7 also shows increases relative to the base year level of 82.0 percent in the proportion of travel occurring on pavements with ride quality rated as acceptable. With traffic assumed to grow at the forecast rate, the projection for 2030 ranges from 93.4 percent at the highest level of investment modeled to 81.5 percent at the lowest. When no change from the 2010 level of investment is modeled, 88.1 percent of travel in 2030 in the forecast traffic growth case is projected to occur on pavements with acceptable ride quality. In the trend traffic growth case, the corresponding projections are 2 to 3 percentage points higher. As noted in Chapter 3, the IRI threshold of 170 used to identify acceptable ride quality was originally set to measure performance on the NHS and may not be fully applicable to non-NHS routes, which tend to have lower travel volumes and speeds.

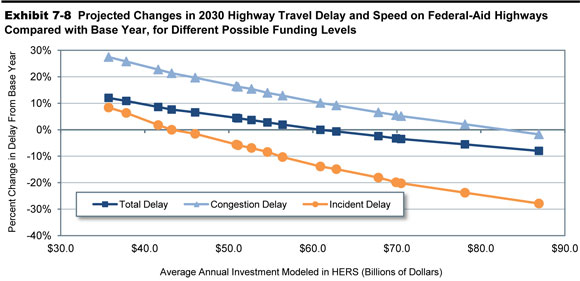

Impact of Future Investment on Highway Operational Performance

Exhibit 7-8 shows the HERS projections for travel time-related indicators of highway performance for the case where traffic grows as forecast in the HPMS. As noted above, HERS assumes the continuation of existing trends in the deployment of certain system management and operations strategies. Among these strategies are several, such as freeway incident management programs, that can be expected to mitigate delay associated with isolated incidents more than the delay associated with recurring congestion (“congestion delay”). In line with this, Exhibit 7-8 shows the amount of incident delay decreasing relative to congestion delay over the period 2010-2030. Assuming that investment within the scope of HERS remains in real terms at its 2010 level, the model projects incident delay per VMT on Federal-aid highways to decrease 10.3 percent between 2010 and 2030, and congestion delay to increase 12.9 percent.

| HERS-Modeled Capital Investment | Projected Impacts on Federal-Aid Highways1 | ||||||

|---|---|---|---|---|---|---|---|

| Annual Percent Change in Spending | Average Annual Spending (Billions of 2010 Dollars) Total2 |

Average Annual Spending (Billions of 2010 Dollars) System Expansion3 |

Annual Hours of Delay per Vehicle4 |

Percent Change Relative to Baseline Total Delay per VMT |

Percent Change Relative to Baseline Congestion Delay per VMT |

Percent Change Relative to Baseline Incident Delay per VMT | Average Speed in 2030 (mph) |

| 3.95% | $86.9 | $43.0 | 47.3 | -8.0% | -1.7% | -27.9% | 44.3 |

| 2.08% | $70.5 | $33.9 | 49.6 | -3.5% | 5.2% | -20.2% | 43.8 |

| 1.71% | $67.8 | $32.2 | 50.2 | -2.4% | 6.6% | -18.1% | 43.7 |

| 0.72% | $60.9 | $28.3 | 51.4 | 0.0% | 10.1% | -13.9% | 43.5 |

| 0.00% | $56.4 | $25.9 | 52.4 | 1.9% | 12.9% | -10.3% | 43.3 |

| -0.32% | $54.6 | $24.9 | 52.8 | 2.8% | 14.0% | -8.4% | 43.3 |

| -0.66% | $52.7 | $23.8 | 53.3 | 3.7% | 15.4% | -6.9% | 43.2 |

| -0.95% | $51.1 | $23.0 | 53.6 | 4.3% | 16.2% | -5.9% | 43.1 |

| -2.62% | $43.2 | $19.0 | 55.3 | 7.6% | 21.4% | 0.0% | 42.8 |

| -4.60% | $35.7 | $15.1 | 57.6 | 12.0% | 27.5% | 8.4% | 42.3 |

| Base Year Values: | 51.4 | 43.2 | |||||

2 The amounts shown represent the average annual investment over 20 years by all levels of government combined that would occur if such spending grows annually in constant dollar terms by the percentage shown in each row of the first column.

3 The amounts shown represent the portion of HERS-modeled spending directed toward system expansion, rather than system rehabilitation, which is influenced by the assumption made about future VMT growth rates.

4 The values shown were computed by multiplying HERS estimates of average delay per VMT by 11,853, the average VMT per registered vehicle in 2010. HERS does not forecast changes in VMT per vehicle over time. The HERS delay figures include delay attributable to stop signs and signals, as well as delay resulting from congestion and incidents.

The results in Exhibit 7-8 also reveal investment within the scope of HERS to be a potent instrument for reducing congestion delay. Exhibit 7-8 splits out the portion of that investment that HERS programs for system expansion (such as the widening of existing highways or building new routes in existing corridors), which will tend to reduce congestion delay more than spending on system rehabilitation.

When average annual total investment is assumed to be sustained at the 2010 level of $56.4 billion, total delay per VMT in 2030 is projected to be 1.9 percent higher than in 2010. If instead annual total investment is assumed to average the $86.9 billion that HERS estimates would be needed to fund all improvements with BCR≥1.0, the projected change in total delay per VMT is a reduction of 8.0 percent from the 2010 level. For annual congestion delay per vehicle in 2030, the projections indicate that the effect of this difference in investment levels is to save 5.1 hours (47.1 hours assuming $86.9 billion per year versus 52.4 hours at actual 2010 spending). In contrast, at assumed investment levels much lower than what was spent in 2010, the projections are for significant increases in congestion delay per VMT—12.0 percent at the lowest level of investment considered, an annual average of $35.7 billion.

| How large is the investment backlog estimated by HERS? | |

|

The investment backlog represents all improvements that could be economically justified for immediate implementation, based solely on the current conditions and operational performance of the highway system (without regard to potential future increases in VMT or potential future physical deterioration of pavements).

The HERS model does not routinely produce rolling backlog figures over time as an output, but is equipped to do special analyses to identify the base year backlog. To determine which action items to include in the backlog, HERS evaluates the current state of each highway section before projecting the effects of future travel growth on congestion and pavement deterioration. Any potential improvement that would correct an existing pavement or capacity deficiency and that has a BCR greater than or equal to 1.0 is considered part of the current highway investment backlog. HERS estimates the size of the backlog as $486.6 billion for Federal-aid highways, stated in constant 2010 dollars. The estimated backlog for the Interstate System is $145.9 billion; adding in other principal arterials produces an estimated backlog of $344.8 billion for the expanded NHS. The investment levels associated with a minimum BCR of 1.0 presented in this chapter would fully eliminate this backlog, as well as addressing other deficiencies that arise over the next 20 years, when it is cost beneficial to do so. It should be noted that these figures reflect only a subset of the total highway investment backlog; they do not include the types of capital improvements modeled in NBIAS (presented later in this chapter) or the types of capital improvements not currently modeled in HERS or NBIAS. Chapter 8 presents an estimate of the combined backlog for all types of improvements. |

|

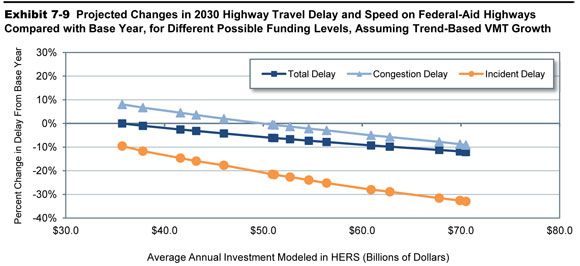

Exhibit 7-9 presents results from HERS simulations in which the baseline VMT growth conforms to 15-year historical trend rather than the HPMS forecasts. Because this reduces the rate of VMT growth, the projections of delay for 2030 are lower than in Exhibit 7-8. For the case where spending continues at the 2010 level, annual delay per vehicle is projected at 47.4 hours versus the 52.4 hours that was projected in Exhibit 7-8 when forecast traffic growth was assumed. The impacts on delay of varying the level of investment are somewhat smaller, as well. For example, increasing average annual investment from the 2010 level to $68.4 billion reduces the 2030 projection of annual delay per vehicle by 1.8 hours (from 47.4 to 45.6), whereas the corresponding reduction in Exhibit 7-8 was 2.2 hours.

| HERS-Modeled Capital Investment | Projected Impacts on Federal-Aid Highways1 | ||||||

|---|---|---|---|---|---|---|---|

| Annual Percent Change in Spending | Average Annual Spending (Billions of 2010 Dollars) Total2 |

Average Annual Spending (Billions of 2010 Dollars) System Expansion 3 |

Annual Hours of Delay per Vehicle 4 |

Percent Change Relative to Baseline Total Delay per VMT |

Percent Change Relative to Baseline Congestion Delay per VMT |

Percent Change Relative to Baseline Incident Delay per VMT | Average Speed in 2030 (mph) |

| 2.08% | $70.5 | $30.0 | 45.2 | -12.1% | -9.1% | -33.0% | 44.6 |

| 1.71% | $67.8 | $28.5 | 45.6 | -11.2% | -7.8% | -31.6% | 44.5 |

| 0.72% | $60.9 | $25.1 | 46.6 | -9.3% | -5.0% | -28.0% | 44.3 |

| 0.00% | $56.4 | $22.8 | 47.4 | -7.8% | -2.9% | -25.2% | 44.2 |

| -0.32% | $54.6 | $22.0 | 47.6 | -7.3% | -2.2% | -23.9% | 44.2 |

| -0.66% | $52.7 | $21.1 | 48.0 | -6.7% | -1.3% | -22.6% | 44.1 |

| -0.95% | $51.1 | $20.3 | 48.2 | -6.2% | -0.7% | -21.6% | 44.0 |

| -2.62% | $43.2 | $16.6 | 49.7 | -3.2% | 3.6% | -15.9% | 43.8 |

| -4.60% | $35.7 | $13.1 | 51.4 | 0.0% | 8.0% | -9.5% | 43.4 |

| Base Year Values: | 51.4 | 43.2 | |||||

2 The amounts shown represent the average annual investment over 20 years by all levels of government combined that would occur if such spending grows annually in constant dollar terms by the percentage shown in each row of the first column.

3 The amounts shown represent the portion of HERS-modeled spending directed toward system expansion, rather than system rehabilitation, which is influenced by the assumption made about future VMT growth rates.

4 The values shown were computed by multiplying HERS estimates of average delay per VMT by 11,853, the average VMT per registered vehicle in 2010. HERS does not forecast changes in VMT per vehicle over time. The HERS delay figures include delay attributable to stop signs and signals, as well as delay resulting from congestion and incidents.

Whichever the traffic growth assumption, forecast or trend, it is important to bear in mind some traffic basics when interpreting these results. In addition to congestion and incident delay, some delay inevitably results from traffic control devices. For this reason, and because traffic congestion occurs only at certain places and times, Exhibits 7-8 and 7-9 show the variation in the level of investment as having less of an impact on projections for total delay and average speed than on the projections for congestion and incident delay. In addition, while the impacts of additional investment on average speed are proportionally small—when trend traffic growth is assumed, investing enough to implement all cost beneficial projects rather than at the 2010 level increases average speed projected for 2030 from 44.2 mph to 44.6 mph—these impacts apply to a vast amount of travel, so that the associated savings in user cost are not necessarily small relative to the cost of the investment.

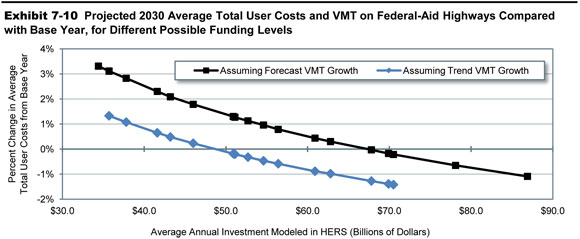

Impact of Future Investment on Highway User Costs

In the HERS model, the benefits from highway improvements are the reductions in highway user costs, agency costs, and societal costs of vehicle emissions. In measuring the highway user costs, the model includes the costs of travel time, vehicle operation, and crashes, but excludes from vehicle operating costs taxes imposed on highway users (such as motor fuel taxes and vehicle registration fees). As discussed in the Introduction to Part II, the exclusion of these taxes conforms with the principle in benefit-cost analysis of measuring the costs of transportation inputs as their opportunity cost to society. The exclusion also makes the measure of user costs more of an indicator of highway conditions and performance, of which the amount paid in highway-user taxes provides no indication.

Impact on Overall User Cost

For Federal-aid highways, HERS estimates that user costs—the costs of travel time, vehicle operation, and crashes—averaged $1.030 per mile of travel in the base year (Exhibit 7-10). When baseline traffic is assumed to grow as forecast, the average user cost is generally higher in the 2030 projection than in the base year estimate. Average user cost is projected to increase between 2010 and 2030 by 0.8 percent and by 2.1 percent under the assumptions that real annual spending remains at the base year level or, alternatively, decreases annually at the rate geared toward maintaining average pavement roughness (2.62 percent). Decreases in average user cost are projected for the two highest levels of spending considered. At the level HERS indicates would be needed to fund all cost-beneficial projects (averaging $86.9 billion annually), average user cost per mile of travel in 2030 is projected to be $1.018, or 1.1 percent less than in the base year. Exhibit 7-10 also reveals that assuming baseline traffic growth to follow trend rather than the HPMS forecasts reduces the projections of average user cost at a given level of investment by 1 to 2 percent.

| HERS-Modeled Capital Investment | Projected Impacts on Federal-Aid Highways* | ||||||

|---|---|---|---|---|---|---|---|

| Annual Percent Change in Spending |

Average Annual Spending (Billions of 2010 Dollars) |

Average Total User Costs ($/VMT) If Forecast VMT Growth |

Average Total User Costs ($/VMT) If Trend VMT Growth |

Percent Change in User Costs per VMT, Relative to Base Year If Forecast VMT Growth |

Percent Change in User Costs per VMT, Relative to Base Year If Trend VMT Growth |

Projected 2030 VMT on Federal-aid Highways (Trillions of VMT)* If Forecast VMT Growth |

Projected 2030 VMT on Federal-aid Highways (Trillions of VMT)* If Trend VMT Growth |

| 3.95% | $86.9 | $1.018 | – | -1.1% | – | 3.629 | – |

| 2.08% | $70.5 | $1.027 | $1.015 | -0.2% | -1.4% | 3.612 | 3.303 |

| 1.71% | $67.8 | $1.029 | $1.017 | 0.0% | -1.3% | 3.608 | 3.300 |

| 0.72% | $60.9 | $1.034 | $1.021 | 0.4% | -0.9% | 3.599 | 3.293 |

| 0.00% | $56.4 | $1.038 | $1.024 | 0.8% | -0.6% | 3.592 | 3.287 |

| -0.32% | $54.6 | $1.040 | $1.025 | 1.0% | -0.5% | 3.589 | 3.285 |

| -0.66% | $52.7 | $1.041 | $1.026 | 1.1% | -0.3% | 3.586 | 3.282 |

| -0.95% | $51.1 | $1.043 | $1.028 | 1.3% | -0.2% | 3.584 | 3.280 |

| -2.62% | $43.2 | $1.051 | $1.035 | 2.1% | 0.5% | 3.568 | 3.268 |

| -4.60% | $35.7 | $1.062 | $1.043 | 3.1% | 1.3% | 3.550 | 3.253 |

| Base Year Values: | $1.030 | 2.520 | |||||

| How much does HERS modify the baseline projections of VMT? | |

|

The modification is largest at the lowest investment level presented in Exhibit 7-10, which averages $35.7 billion per year and corresponds to negative 4.6 percent annual growth in spending. At this investment level, average user costs are projected to increase between 2010 and 2030 by 3.1 percent when the baseline traffic growth is assumed to be as forecast in HPMS. The projected increase in average user cost operates through the HERS elasticity mechanism to reduce the VMT projection for 2030. The increase from 2.520 trillion VMT in the base year to 3.550 trillion VMT in 2030 translates into an average annual VMT growth rate of 1.73 percent, which falls below the 1.85 percent growth rate forecast in HPMS.

Similarly, when traffic growth is assumed to follow the 15-year trend, average user costs per VMT are projected to increase by 1.3 percent; the increase from 2.520 trillion VMT to 3.253 trillion VMT translates into an average annual VMT growth rate of 1.28 percent, rather than the 1.36 percent annual growth rate assumed if user costs remained constant. In the present analysis, the percent changes in average user cost are relatively small. For this reason, and because HERS incorporates the indications from available evidence that travel demand is not highly sensitive to price, HERS only slightly modifies the baseline projection of VMT. |

|

The projections in Exhibit 7-10 for VMT on Federal-aid highways incorporate the effects on travel demand of changes in average user cost. These outputs from the HERS analysis differ from the “trend” and “forecast” projections of VMT on Federal-aid highways that are inputs to the analysis. The input projections, which were shown in Exhibit 7-2, are interpreted as representing the baseline levels of traffic in the absence of any change in average user cost from the 2010 level. The 2030 traffic levels presented in Exhibit 7-10 are thus higher or lower than these baseline levels according to whether average user cost is projected to decrease or increase.

Impact on User Cost Components

Exhibit 7-11 shows the projected changes from 2010 to 2030 in average user cost of travel on Federal-aid highways by cost component. The cost of crashes is the component least sensitive to the assumed level of highway investment, which as an annual average varies between $35.7 billion and $86.9 billion or $70.5 billion depending on whether baseline VMT growth is assumed to follow the HPMS forecast or the 15-year trend. Compared with the lowest level, the highest level of spending reduces the crash cost per VMT by 0.7 percent (forecast case) or 0.1 percent (trend case). These levels of spending are limited to the types of improvements that HERS evaluates, which are basically system rehabilitation and expansion. Because the HPMS lacks detailed information on the current location and characteristics of safety-related features (e.g., guardrail, rumble strips, roundabouts, yellow change intervals at signals), safety-focused investments are not evaluated. Thus, the findings presented in Exhibit 7-11 establish nothing about how such investments affect highway safety.

| HERS-Modeled Capital Investment | Projected Impacts on Federal-Aid Highways Percent Change in User Costs per VMT in 2030, Relative to Base Year | ||||||

|---|---|---|---|---|---|---|---|

| Annual Percent Change in Spending |

Average Annual Spending (Billions of 2010 Dollars) |

Travel Time Costs If Forecast VMT Growth |

Travel Time Costs If Trend VMT Growth |

Vehicle Operating Costs1 If Forecast VMT Growth |

Vehicle Operating Costs 1 If Trend VMT Growth |

Crash Costs 2 If Forecast VMT Growth |

Crash Costs 2 If Trend VMT Growth |

| 3.95% | $86.9 | -3.0% | – | 0.2% | – | 1.1% | – |

| 2.08% | $70.5 | -1.8% | -3.9% | 1.0% | 0.8% | 1.3% | 0.1% |

| 1.71% | $67.8 | -1.6% | -3.7% | 1.1% | 0.9% | 1.3% | 0.1% |

| 0.72% | $60.9 | -0.9% | -3.2% | 1.6% | 1.3% | 1.4% | 0.2% |

| 0.00% | $56.4 | -0.4% | -2.8% | 1.8% | 1.5% | 1.5% | 0.3% |

| -0.32% | $54.6 | -0.2% | -2.7% | 2.0% | 1.7% | 1.5% | 0.3% |

| -0.66% | $52.7 | 0.1% | -2.5% | 2.1% | 1.8% | 1.5% | 0.4% |

| -0.95% | $51.1 | 0.2% | -2.4% | 2.3% | 1.9% | 1.6% | 0.4% |

| -2.62% | $43.2 | 1.2% | -1.5% | 3.2% | 2.7% | 1.6% | 0.4% |

| -4.60% | $35.7 | 2.5% | -0.6% | 4.1% | 3.7% | 1.8% | 0.6% |

2 The HPMS does not contain the type of detail that would be needed to conduct an analysis of targeted safety enhancements. The crash costs estimated by the HERS model represent ancillary impacts associated with pavement and capacity improvements and are heavily influenced by traffic volume and speed.

Crash costs also form the smallest of the three components of highway user costs. For 2010 travel on Federal-aid highways, HERS estimates the breakdown by cost component to be crash cost, 13.6 percent; travel time cost, 44.9 percent, and vehicle operating cost, 41.5 percent. Research under way to update the vehicle operating cost equations in HERS (see Appendix D) may somewhat alter the split among these costs, but crash costs will remain a small component. Although highway trips always consume traveler time and resources for vehicle operation, only a small fraction involve crashes. In addition, most crashes are non-catastrophic: particularly on urban highways, many involve only damage to property without anyone being injured.

The projections for the travel time costs are somewhat more sensitive to the assumed level of investment than are the projections for vehicle operating costs. When baseline VMT growth is based on HPMS forecasts, the projected 2010-2030 change in travel cost per VMT ranges from a decrease of 3.5 percent at the highest level of assumed investment to an increase of 2.5 percent at the lowest. This implies that investing at the highest rather than the lowest level would reduce the per VMT cost of travel in 2030 by 5.4 percent (= (035+.025)/(1-.025)). For vehicle operating cost, the corresponding estimate is a reduction of 3.3 percent. When VMT growth is based on trend rather than forecasts, the projections of travel time and vehicle operating cost are lower and less sensitive to variation in the assumed investment level. Investing at the highest level shown for the trend forecast case rather than at the lowest level reduces the projected time cost of travel in 2030 by 3.7 percent and the projected vehicle operating cost by 2.8 percent.

For vehicle operating costs per VMT, all the projections in Exhibit 7-11 show levels in 2030 to exceed those for 2010. This uniformity contrasts with the mixed pattern in the projections for travel time cost and reflects the assumption of future increases in motor fuel prices. For these prices and for vehicle fuel economy, the assumptions are based on projections from the Energy Information Administration (EIA) Annual Energy Outlook 2012. The weighted average price of gasoline and diesel fuel is assumed to increase between 2010 and 2030 by 45 percent more than the consumer price index. This increase outweighs the fuel cost savings that would result from the improvements in vehicle energy efficiency that the EIA projects for this same period; these equate to increases in average MPG of 32.8 percent for light-duty vehicles, 30.0 percent for two-axle trucks, and 19.4 percent for 3+ axle trucks. These projections incorporate the effect of increases in Corporate Average Fuel Economy (CAFE) standards and U.S. Environmental Protection Agency (EPA) standards for emissions of greenhouse gases by automobiles and light trucks through model year 2016, as well as new standards for fuel efficiency and greenhouse gas emissions for medium- and heavy-duty trucks through model year 2018 adopted by U.S. Department of Transportation (DOT) and EPA.

| What changes in CAFE standards have recently been adopted, and what impacts are these changes expected to have? | |

|

On May 7, 2010, NHTSA and EPA jointly adopted Corporate Average Fuel Economy (CAFE) and carbon dioxide (CO2) emission standards for cars and light trucks produced during model years 2012 through 2016. In combination with NHTSA’s previous actions, this rule raised required fuel economy levels for cars from 27.5 miles per gallon (mpg) in model year 2010 to 37.8 mpg for model year 2016, and those for light trucks from 23.5 mpg in 2010 to 28.8 mpg for 2016. On August 28, 2012, the two agencies adopted new rules that further increased CAFE standards for model year 2021 to 46.1 to 46.8 mpg for automobiles and to 32.6 to 33.3 mpg for light trucks; this most recent action also established tentative CAFE standards for model year 2025 of 55.3 to 56.2 mpg for cars and 39.3 to 40.3 mpg for light trucks.

The impacts of these standards on the fuel economy of the overall vehicle fleet will continue to grow for many years beyond 2025, as new vehicles meeting the higher fuel economy requirements gradually replace older, less-fuel-efficient vehicles. In announcing the most recent increases in CAFE standards, NHTSA estimated that the cumulative effects of its actions would be to save more than 500 billion gallons of fuel and reduce carbon dioxide emissions by 6 billion metric tons over the lifetimes of cars and light trucks produced in 2011 through 2025. The agency also estimated that its standards would save the Nation’s drivers more than $1.7 trillion in fuel costs over these vehicles’ lifetimes. In 2011, NHTSA and EPA also established new fuel efficiency and CO2 emission standards for medium- and heavy-duty trucks produced from 2014 through 2018. These standards are expected to reduce fuel consumption by an additional 22 billion gallons, while further reducing CO2 emissions by nearly 270 million metric tons. |

|

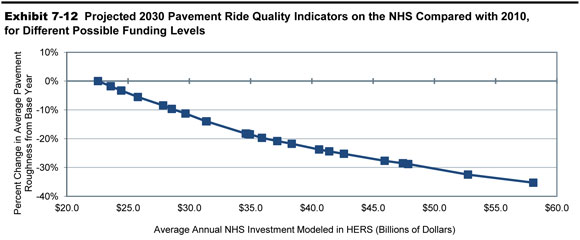

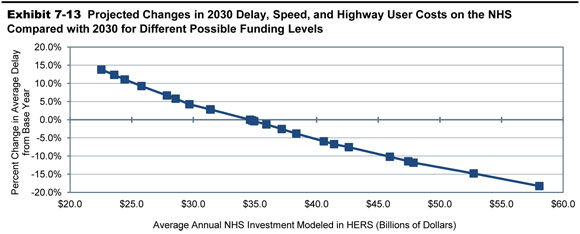

Impacts of NHS Investments Modeled by HERS

As described in Chapter 2, the NHS includes the Interstate System as well as other routes most critical to national defense, mobility, and commerce. As noted earlier, the NHS analyses presented in this chapter are based on an estimate of what the NHS will look like after it is expanded pursuant to MAP-21, rather than the actual system as it existed in 2010.

This section examines the total spending modeled in HERS, identifying the portion of this investment that is directed by the model to the NHS, and the impacts that such investment could have on future NHS conditions and performance. For Federal-aid highways, the preceding analysis in this chapter examined the effect on the HERS projections of replacing the HPMS traffic forecasts with trend traffic growth. In analyzing investments in the NHS portion of Federal-aid highways, this section assumes traffic growth as forecast in the HPMS.

HERS allocates a portion of future investment in Federal-aid highways to the NHS based on the model’s engineering and economic criteria, which give funding priority to high-BCR projects. The levels of future investment in Federal-aid highways considered in this section’s analysis are either identical to or counterparts of levels considered in this chapter’s preceding sections. Carried over from the preceding analysis are the investment levels tied to a specific minimum BCR among all improvements to the Federal-aid highways that HERS programs over the analysis period. Also included are levels of investment in Federal-aid highways tied to one of the goals considered in the preceding analysis, such as maintaining average pavement roughness at the base year level, except that the goals are now limited to the NHS. In the simulations with these investment levels, HERS allocates to the NHS the amount needed to achieve the goal for the NHS without regard to whether or not the same goal is met for other Federal-aid highways.

| How were the seven NHS investment levels presented in Exhibits 7-12 and 7-13 selected? | |

|

As MAP-21 directs that the NHS be expanded, the 20-year NHS projections presented in this report were based on all sections coded in HPMS as being on the NHS, plus those other principal arterials that are not currently part of the NHS. While this will not exactly match the scope of the NHS in the future (some sections currently coded as principal arterials may not be ultimately be included in the NHS, and some additional connector mileage may be included), it represents a reasonably close approximation for purposes of the types of analyses presented.