Chapter 7: Capital Investment Scenarios

- Highway Capital Investment Scenarios

- Scenarios Selected for Analysis

- Scenario Spending Levels and Sources

- Systemwide Scenario Spending Patterns and Conditions and Performance Projections

- Improve Conditions and Performance Scenario

- Transit Capital Investment Scenarios

- Sustain 2014 Spending Scenario

- State of Good Repair Benchmark

- Low-Growth and High-Growth Scenarios

- Scenario-Impacts-Comparison

Key Takeaways

- Three illustrative 20-year scenarios are considered: Sustain 2014 Spending, Maintain Conditions and Performance, and Improve Conditions and Performance. Each scenario relates to total highway capital spending by all levels of government combined, and the private sector, stated in constant 2014 dollars.

- The Improve Conditions and Performance scenario assumes that $95.9 billion would be provided for all projects that meet or exceed a benefit-cost ratio of 1.0, and that $39.8 billion would be provided for projects not included in the models and that may or may not be cost-beneficial, for an average annual capital investment of $135.7 billion in total.

- Approximately 29 percent of the investment required under the Improve Conditions and Performance scenario would go toward addressing an existing backlog of cost-beneficial investments of $786.4 billion. The rest would address new needs arising from 2015 through 2034.

- The Maintain Conditions and Performance scenario over the 20-year period of analysis would require 2.9 percent less average annual funding than actual 2014 highway capital spending of $105.4 billion.

Highway Capital Investment Scenarios

This section presents future investment scenarios that build on the Chapter 10 analyses of alternative levels of future investment in highways and bridges. Each scenario includes projections for system conditions and performance based on simulations using the Highway Economic Requirements System (HERS) and National Bridge Investment Analysis System (NBIAS). The combined scope of the two models covers system rehabilitation investments for bridges on all roads, system rehabilitation investments for pavements on Federal-aid highways, and system expansion investments on Federal-aid highways. Each scenario scales up the total amount of simulated investment to account for capital improvements (highway and bridge investments) that are outside the scopes of the models, and for which limited information is available on the benefits and costs of individual investments. Such “non-modeled” investments (sometimes called “other” in the exhibits), account for 29.3 percent of the spending in each scenario. Later in this chapter, transit investment scenarios are explored that, like those of this section, start with 2014 as the base year and cover the 20-year period through 2034. All scenarios are illustrative, and none is endorsed as a target level of funding.

Supplemental analyses relating to these scenarios, including comparisons with the investment levels presented for comparable scenarios in previous C&P Reports, are the subject of Chapter 8. A series of sensitivity analyses that explore the implications of alternative technical assumptions for the scenario investment levels is presented in Chapter 9. The introduction to Part II provides essential background information relating to the technical limitations of the analysis, which are discussed further in the appendices.

Scenarios Selected for Analysis

This section examines three spending scenarios based on capital investment by all levels of government combined. The question of what portion should be funded by the Federal government, State governments, local governments, or the private sector is beyond the scope of this report. Analyses were conducted for the entire public road network (titled “Systemwide” in the exhibits). Additional details on the impacts of alternative investment levels on system subsets, including Federal-aid highways, the National Highway System, and the Interstate System, are presented in Chapter 10.

Key Limitations of HERS Model

The HERS model relies on various assumptions about travel behavior and associated travel costs as well as the benefits and costs of infrastructure improvements. Research is conducted on an ongoing basis to assess the accuracy of these assumptions, and when possible the HERS model assumptions are adjusted to more accurately reflect real-world dynamics. Substantial changes in the HERS model assumptions from the 2015 C&P Report are described in Appendix A. In particular, updates to the HERS model for this report include adjustments to improvement costs per mile, pavement condition modeling, value of travel time savings, and highway operation strategies.

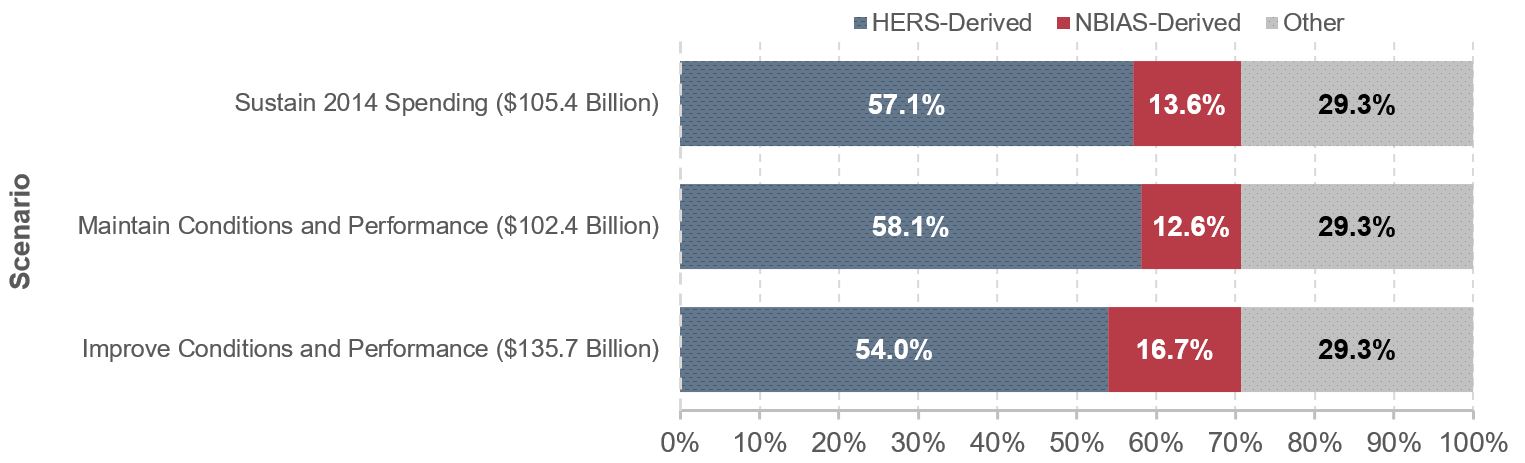

Each scenario pairs an assumed level of total investment in the types of improvements modeled by HERS with an assumed level of investment in the types of improvements modeled by NBIAS; these levels are drawn from those considered in Chapter 10. Together, the scopes of HERS and NBIAS cover spending on highway expansion and pavement improvements on Federal-aid highways (HERS) and spending on bridge rehabilitation on all roads (NBIAS). In the absence of data required for other types of highway and bridge investment (those not modeled in HERS or NBIAS), each scenario simply assumes that the percentage of highway and bridge investment spent on nonmodeled investments remains at the 2014 percentage (29.3 percent).

The objective of the Sustain 2014 Spending scenario is to predict the impact on highway conditions and performance after 20 years, if highway capital spending remains constant (adjusted for inflation) over that period. The Maintain Conditions and Performance scenario seeks to identify the level of investment needed to keep overall system conditions and performance unchanged after 20 years. The Improve Conditions and Performance scenario seeks to identify the level of investment needed to address all potential investments estimated to be cost-beneficial. Exhibit 7-1 describes the derivation of each of these scenarios in greater detail.

Exhibit 7-1: Capital Investment Scenarios for Highways and Bridges and Derivation of Components

| Scenario Component | Sustain 2014 Spending Scenario | Maintain Conditions and Performance Scenario | Improve Conditions and Performance Scenario | State of Good Repair Benchmark |

|---|---|---|---|---|

| HERS-Derived | Sustain spending on types of capital improvements modeled in HERS at 2014 levels in constant dollar terms over next 20 years. | Set spending at the lowest level at which (1) projected average IRI in 2034 matches (or is better than) the value in 2014 and (2) projected average delay per VMT in 2034 matches (or is better than) the value in 2014. | Set spending at the level sufficient to fund all cost-beneficial potential projects (i.e., those with a benefit-cost ratio greater than or equal to 1.0). | Subset of Improve Conditions and Performance scenario; includes spending on system rehabilitation; excludes spending on system capacity. |

| NBIAS-Derived | Sustain spending on types of capital improvements modeled in NBIAS at 2014 levels in constant dollar terms over the next 20 years. | Set spending at the level at which the projected percentage of deck area on bridges in poor condition in 2034 matches that in 2014. | Set spending at the level sufficient to fund all cost-beneficial potential projects. | Includes all NBIAS-derived spending included in the Improve Conditions and Performance scenario. |

| Other (Nonmodeled) | Sustain spending on types of capital improvements not modeled in HERS or NBIAS at 2014 levels in constant dollar terms over the next 20 years. | Set spending at the level necessary so that the nonmodeled share of total highway and bridge investment will remain the same as in 2014. | Set spending at the level necessary so that the nonmodeled share of total highway and bridge investment will remain the same as in 2014. | Subset of Improve Conditions and Performance scenario; includes spending on system rehabilitation; excludes spending on system capacity and system enhancement. |

Exhibit 7-1 also references a critical subset of the Improve Conditions and Performance scenario, the State of Good Repair benchmark. This benchmark represents the level of investment that would be necessary to address all cost-beneficial investments that would improve the physical conditions of existing highway infrastructure assets.

The projections for conditions and performance in each scenario are estimates of what could be achieved with a given level of investment assuming an economically driven approach to project selection. (The project selection method is explained in Chapter 10). The projections do not necessarily represent what would be achieved given current decision-making practices. Consequently, comparing the relative conditions and performance outcomes across the different scenarios might be more illuminating than focusing on the specific projections for each scenario individually.

Changes in Scenario Definitions Relative to the 2015 C&P Report

The key differences between the scenarios presented in this report relative to those in the 2015 C&P Report are:

- As the base year of the analysis for this report is 2014 rather than 2012, the Sustain 2014 Spending scenario replaces the Sustain 2012 Spending scenario analyzed in the 2015 C&P Report.

- The investment pattern assumed for Maintain Conditions and Performance scenario in this report is “flat” (i.e., the same level of investment would occur in each year), rather than “ramped” (i.e., investment would grow at a constant annual percentage). Also, the NBIAS-derived component of the scenario targets the share of total bridge deck area that is on bridges rated as “poor,” rather than the share of bridges rated as structurally deficient or functionally obsolete. (See Chapters 6 and 10.)

- The Improve Conditions and Performance scenario (and the State of Good Repair benchmark) used in this report address cost-beneficial investments immediately, rather than gradually addressing them over 20 years based on ramped investment pattern.

Scenario Spending Levels and Sources

Exhibit 7-2 summarizes capital investment levels associated with each 20-year scenario and benchmark, stated in constant 2014 dollars. The Sustain 2014 Spending scenario fixes average annual investment to actual 2014 levels for each investment period, resulting in annual investment of $105.4 billion, or approximately $2.1 trillion over 20 years.

Exhibit 7-2: Highway Capital Investment Levels, by Scenario

| Scenario and Comparison Parameter | Capital Investment for 2015 through 2034 (Billions of $2014) | Percent Difference Relative to 2014 | Investment Pattern | |

|---|---|---|---|---|

| 20-Year Total | Average Annual | |||

| Sustain 2014 Spending Scenario | $2,108.5 | $105.4 | 0.0% | Flat |

| Maintain Conditions and Performance Scenario | $2,048.0 | $102.4 | -2.9% | Flat |

| Improve Conditions and Performance Scenario | $2,714.9 | $135.7 | 28.8% | Variable |

| State of Good Repair Benchmark* | $1,767.9 | $88.4 | ||

*The estimated spending under this benchmark is a subset of the estimated spending under the Improve Conditions and Performance Scenario.

Sources: Highway Economic Requirements System and National Bridge Investment Analysis System.

The estimated level of annual investment needed to achieve the objectives of the Maintain Conditions and Performance scenario is $102.4 billion, 2.9 percent less than actual 2014 spending. This suggests that current levels of investment would be sufficient to keep overall conditions and performance from worsening over time. However, some individual measures of conditions and performance (aside from those specifically targeted by the scenario definition) would likely improve over 20 years, while others would likely see some deterioration. It should also be noted that, because it is focused on conditions and performance for the overall system, this scenario might sometimes entail improvement and sometimes deterioration in average conditions and performance on subsets of some networks.

Achieving the objectives of the Improve Conditions and Performance scenario would require an estimated average annual spending level of $135.7 billion, which exceeds the 2014 level by 28.8 percent. Because there is an existing backlog of cost-beneficial investments that have not previously been addressed, the Improve Conditions and Performance scenario results in higher levels of investment in the early years of the analysis and lower levels in the latter years. This investment pattern is discussed in greater detail in Chapter 10. The total needed to address both the existing backlog and additional cost-beneficial investments needed to address issues that arise over the next 20 years is estimated to be approximately $2.7 trillion; the backlog is quantified later in this section.

The average annual investment level associated with the State of Good Repair benchmark is $88.4 billion, which is the total amount of investment in pavement and bridge rehabilitation that is projected to be cost-beneficial. This benchmark is the rehabilitation portion of the investment in the Improve Conditions and Performance scenario. In determining the level of investment under this benchmark, HERS and NBIAS screen out through benefit-cost analysis any assets that might have outlived their original purpose, rather than automatically reinvesting in all assets in perpetuity. With national consensus lacking on exactly what constitutes a “state of good repair” for highway assets, alternative benchmarks with different objectives could be equally valid from a technical perspective. (Note that the Transit State of Good Repair Benchmark presented later in this chapter does not apply a benefit-cost screen.)

The sources of the estimates of average annual investment levels are presented in Exhibit 7-3. The HERS-derived component, which accounts for most of the total investment in each scenario, represents spending on pavement rehabilitation and capacity expansion on Federal-aid highways.

Exhibit 7-3: Source of Estimates for Highway Capital Investment Scenarios, by Model

Sources: Highway Economic Requirements System and National Bridge Investment Analysis System.

The NBIAS-derived component represents rehabilitation spending on all bridges, including those not on Federal-aid highways. The Other (nonmodeled) spending, which accounted for 29.3 percent of total investment in 2014, is assumed to comprise the same share in all systemwide scenarios. The nonmodeled share includes most expenditures off of Federal-aid highways (the HERS analysis is limited to Federal-aid highways only) and expenditures classified in Chapter 2 as system enhancements (safety enhancements, traffic operation improvements, and environmental enhancements). As discussed in the Introduction to Part II, the nonmodeled share is much lower for major system subsets, such as Federal-aid highways, the NHS, and Interstate highways.

Systemwide Scenario Spending Patterns and Conditions and Performance Projections

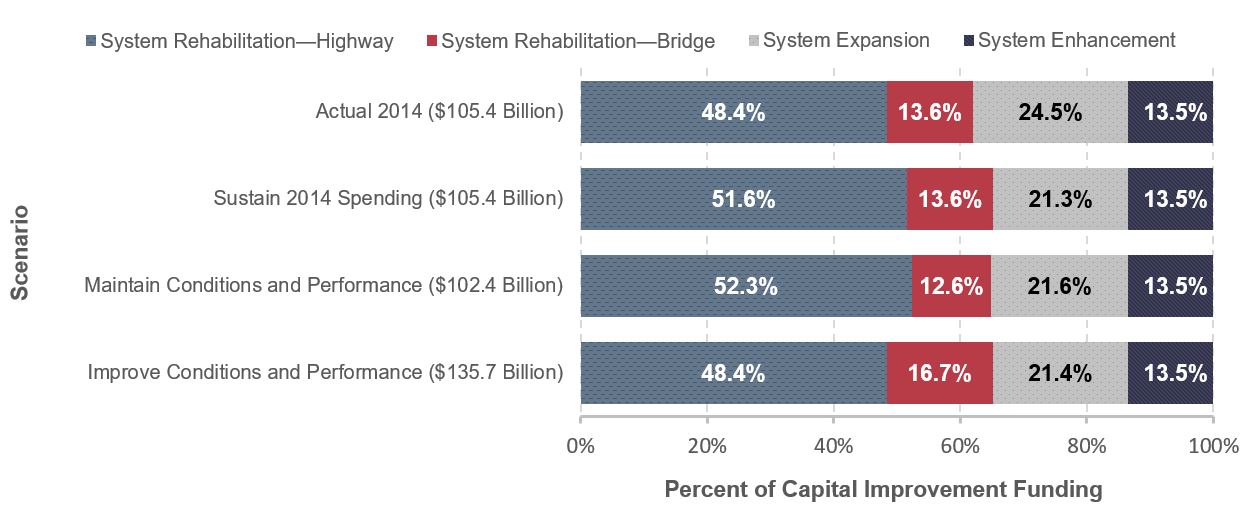

Exhibit 7-4 compares the distributions from each scenario for investment spending by improvement type with the actual distribution of capital spending in 2014. Comparing the Sustain 2014 Spending scenario to the actual 2014 spending distribution, HERS modeling results support less spending on system expansion and more spending on highway rehabilitation than currently occurs. At the higher levels of spending attempted in the Improve Conditions and Performance scenario, the modeling results suggest spending devoting a greater share of investment to bridge system rehabilitation relative to highway system rehabilitation and system expansion.

Exhibit 7-4: Systemwide Highway Capital Investment Scenarios for 2015 Through 2034: Distribution by Capital Improvement Type Compared with Actual 2014 Spending

| Average Annual Distribution by Capital Improvement Type (Billions of 2014 Dollars) | ||||

|---|---|---|---|---|

| Capital Improvement Type | Actual 2014 Spending Distribution | Sustain 2014 Spending Scenario | Maintain Conditions & Performance Scenario | Improve Conditions & Performance Scenario |

| System Rehabilitation—Highway | $51.0 | $54.4 | $53.6 | $65.7 |

| System Rehabilitation—Bridge | $14.4 | $14.4 | $12.9 | $22.7 |

| System Rehabilitation—Total | $65.4 | $68.8 | $66.5 | $88.4 |

| System Expansion | $25.9 | $22.5 | $22.1 | $29.1 |

| System Enhancement | $14.2 | $14.2 | $13.8 | $18.3 |

| Total, All Improvement Types | $105.4 | $105.4 | $102.4 | $135.7 |

Sources: Highway Economic Requirements System and National Bridge Investment Analysis System.

In the Improve Conditions and Performance scenario, annual spending on highway and bridge rehabilitation averages $88.4 billion, considerably more than the $65.4 billion of such spending in 2014. This result suggests that achieving a state of good repair on the Nation’s highways by implementing all cost-beneficial system rehabilitation improvements would require either a significant increase in overall highway and bridge investment or a significant redirection of investment from other types of improvements toward system rehabilitation (the latter of which could involve prioritizing less cost-beneficial rehabilitation improvements over more cost-beneficial expansion investments).

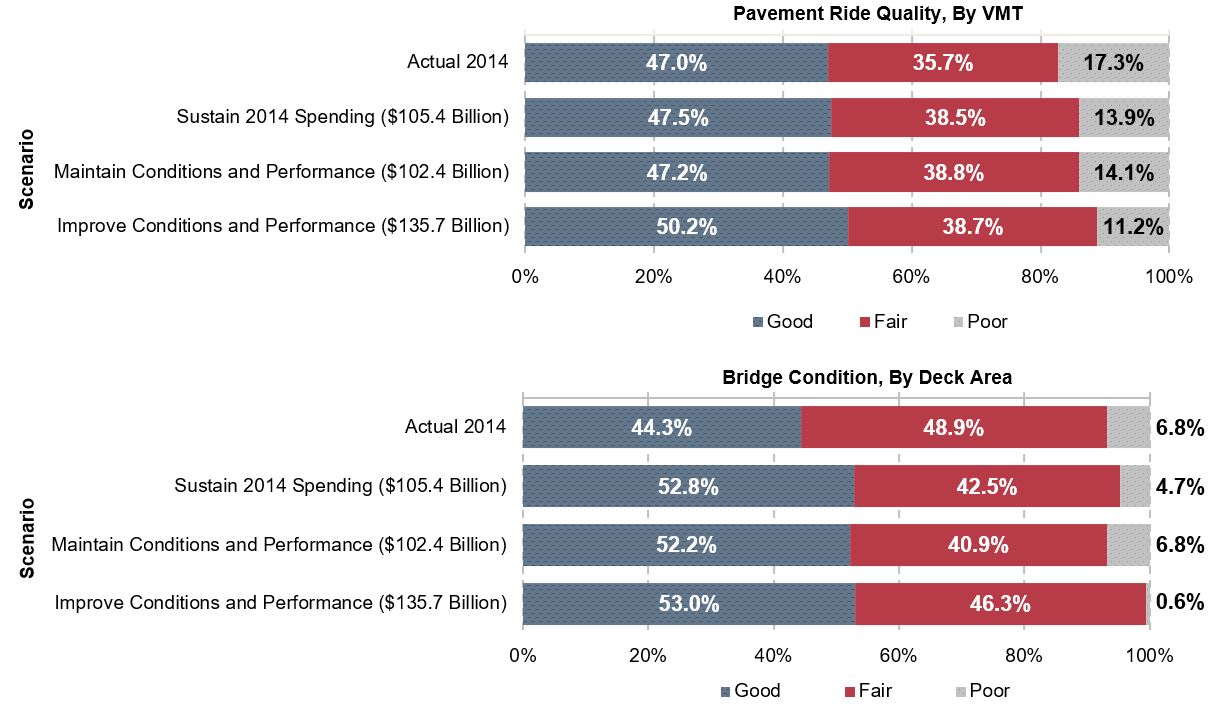

Exhibit 7-5 presents conditions and performance indicators for all systemwide scenarios. This information can also be found in various tables in Chapter 10. Because HERS considers only Federal-aid highways, the indicators for the Federal-aid highway scenarios are presented in place of indicators for all roads in Exhibit 7-5. In contrast, NBIAS considers bridges on all roads.

Under the Sustain 2014 Spending scenario, the share of vehicle miles traveled (VMT) on Federal-aid highways with poor ride quality would be reduced from 17.3 percent in 2014 to 13.9 percent in 2034, while the share on pavements with good ride quality would rise slightly from 47.0 percent to 47.5 percent. Average International Roughness Index (IRI) would decrease (improve) by 0.3 percent in 2034 relative to 2014, while the average delay per VMT would decrease (improve) by 18.5 percent. The share of bridges (weighted by deck area) that are rated as poor would drop from 6.8 percent in 2014 percent to 4.7 percent in 2034, while the share rated as good would rise from 44.3 percent to 52.8 percent.

The cells shaded in Exhibit 7-5 are the values relevant to the definition of the Maintain Conditions and Performance scenario. The cell showing 6.8 percent of bridges (as measured by deck area) rated in poor condition in 2034 is highlighted, as it matches the actual value for that metric in 2014. The cell showing that the average change in VMT-weighted IRI is 0.0 percent is highlighted, showing that this metric is unchanged relative to the actual 2014 value.

VMT-Weighting vs. Deck Area-Weighting

The performance indicators presented in Exhibit 7-5 were drawn from the more detailed analysis of the impacts of alternative investment levels presented in Chapter 10. The pavement and delay statistics presented in terms of VMT were derived from HERS while the bridge condition statistics weighted by deck area were derived from NBIAS. While weighting by use is more relevant from an economic perspective, FHWA has traditionally reported bridge performance statistics on a deck area-weighted basis rather than weighting by average daily traffic.

Under the PM-2 rule referenced in the Introduction to Part I and Chapter 6, States will be setting performance targets for pavements on a lane mile-weighted basis and setting performance targets for bridges on a deck area-weighted basis. For consistency purposes, future C&P reports will place a greater emphasis on lane-mile weighted measures for pavements.

Under the Improve Conditions and Performance scenario, the share of VMT on Federal-aid highways with poor ride quality would be reduced to 11.2 percent in 2034, while the share on pavements with good ride quality would rise to 50.2 percent. Average IRI would decrease (improve) by 5.6 percent over the 20-year period, while the average delay per VMT would decrease (improve) by 19.3 percent. The share of bridges (weighted by deck area) that are rated as in poor condition is projected to drop to 0.6 percent in 2034, while the share rated as good would rise to 53.0 percent.

Exhibit 7-5: Systemwide Highway Capital Investment Scenarios for 2015 Through 2034: Projected Impacts on Selected Highway Performance Measures

| Highway Performance Measure | Actual 2014 Values | Sustain 2014 Spending Scenario | Maintain Conditions & Performance Scenario | Improve Conditions & Performance Scenario |

|---|---|---|---|---|

| Pavement Ride Quality and Bridge Conditions (Good/Fair/Poor)1 | ||||

| Percent of VMT on pavements with good ride quality1 | 47.0% | 47.5% | 47.2% | 50.2% |

| Percent of VMT on pavements with fair ride quality1 | 35.7% | 38.5% | 38.8% | 38.7% |

| Percent of VMT on pavements with poor ride quality1 | 17.3% | 13.9% | 14.1% | 11.2% |

| Percent of bridges rated as good condition, by deck area | 44.3% | 52.8% | 52.2% | 53.0% |

| Percent of bridges rated as fair condition, by deck area | 48.9% | 42.5% | 40.9% | 46.3% |

| Percent of bridges rated as poor condition, by deck area | 6.8% | 4.7% | 6.8% | 0.6% |

| Projected Changes by 2034 Relative to 2014 for Selected Indicators | ||||

| Percent change in average IRI (VMT-weighted)1 | 0.0% | -0.3% | 0.0% | -5.6% |

| Percent change in average delay per VMT1 | 0.0% | -18.5% | -18.4% | -19.3% |

1 The HERS indicators shown apply only to Federal-aid highways as HPMS sample data are not available for rural minor collectors, rural local, or urban local roads.

Sources: Highway Economic Requirements System and National Bridge Investment Analysis System.

Improve Conditions and Performance Scenario

The manner in which the Improve Conditions and Performance scenario is defined makes it easier to drill down further into the results than is the case for the Maintain Conditions and Performance scenario. For example, looking at the Maintain Conditions and Performance scenario output on a functional class basis could be misleading, as conditions and performance could improve on some functional classes while declining on others. Thus, the investment levels identified for each functional class on a systemwide analysis would differ from those obtained by analyzing each functional class separately to determine the investment level to maintain its overall conditions and performance at base-year levels. This limitation does not apply to the Improve Conditions and Performance scenario; since the objective of the scenario is to make all cost-beneficial investments, one would obtain the same result for each functional class whether analyzed separately or as part of a systemwide run.

Spending by System

Exhibit 7-6 compares the distribution of spending for the Improve Conditions and Performance scenario by system, and by capital improvement type against the actual 2014 spending. As noted in Chapter 1, the Interstate Highway System is a subset of the National Highway System, which is a subset of Federal-aid highways, which is a subset of the overall highway network (all roads).

About 49.4 percent of the Improve Conditions and Performance scenario spending goes for improvements to the NHS, while 23.2 percent goes for improvements to Interstate highways.

Spending on all capital improvement types for Interstate highways under the Improve Conditions and Performance scenario is 24.3 percent higher than actual 2014 spending. The Improve Conditions and Performance scenario would increase spending for all systems and capital improvement types except for highway system rehabilitation spending on Interstate highways, which decreases by 17.3 percent relative to the actual amount spent in 2014.

The largest gaps (in percentage terms) for each system are in system rehabilitation for bridges, which range from 58.3 percent for all roads to 150.4 percent for Interstate highways, compared with actual 2014 spending. Spending on system expansion in the Improve Conditions and Performance scenario increases modestly by 12.5 percent for all roads compared with actual 2014 spending, while for Interstate highways the increase is significantly higher at a 58.5 percent increase. In considering the implications of these gaps, it is important to note that they pertain to just a single year’s spending (2014), which may not be fully consistent with longer term trends, particularly as one drills down into smaller and smaller subsets of the overall system.

Exhibit 7-6: Improve Conditions and Performance Scenario for 2015 Through 2034: Distribution by System and by Capital Improvement Type Compared with Actual 2014 Spending

| System Component | System Rehabilitation | System Expansion | System Enhancement | Total | Percent of Total | ||

|---|---|---|---|---|---|---|---|

| Highway | Bridge | Total | |||||

| Average Annual Investment in Billions of 2014 Dollars | |||||||

| Interstate Highway System | $11.9 | $7.9 | $19.9 | $9.3 | $2.3 | $31.4 | 23.2% |

| National Highway System | $29.6 | $12.8 | $42.3 | $18.5 | $6.2 | $67.0 | 49.4% |

| Federal-aid Highways | $49.0 | $18.4 | $67.4 | $24.2 | $11.1 | $102.7 | 75.7% |

| All Public Roads | $65.7 | $22.7 | $88.4 | $29.1 | $18.3 | $135.7 | 100.0% |

| Percent Above Actual 2014 Capital Spending by All Levels of Government Combined | |||||||

| Interstate Highway System | -17.3% | 150.4% | 12.8% | 58.5% | 24.3% | 24.3% | |

| National Highway System | 9.5% | 79.5% | 24.1% | 8.9% | 19.0% | 19.0% | |

| Federal-aid Highways | 28.7% | 74.5% | 38.6% | 9.7% | 29.6% | 29.6% | |

| All Public Roads | 28.7% | 58.3% | 35.2% | 12.5% | 28.8% | 28.8% | |

Note: The "NBIAS-Derived" share includes all outlays classified as "System Rehabilitation: Bridge." The "HERS-Derived" share includes most outlays classified as "System Rehabilitation: Highway" and "System Expansion" except for the portions spent off of Federal-aid Highways, which are classified as "Other." The "Other" category also includes all outlays classified as "System Enhancement."

Source: Highway Economic Requirements System and National Bridge Investment Analysis System.

Spending by Improvement Type and Highway Functional Class

Exhibit 7-7 presents the distribution by improvement type and highway functional class for the Improve Conditions and Performance scenario compared with actual 2014 spending for Federal-aid highways.

Moving to a finer level of detail in the analysis tends to reduce the reliability of simulation results from HERS and NBIAS, so the results presented in this exhibit should be viewed with caution. Nevertheless, the patterns suggest certain directions in which spending patterns would need to change for scenario goals to be achieved. The scenarios can feature shifts in spending across highway functional classes, and in highway spending between rehabilitation and expansion, because the modeling frameworks determine allocations through benefit-cost optimization.

The Improve Conditions and Performance scenario would shift funds away from rural other principal arterials and minor arterials to other roadway types relative to what occurred in 2014, but would result in higher spending for all other functional classes. Spending on rural roads would increase by 5.7 percent from actual 2014 spending to $29.7 billion, while spending on urban roads would increase by 42.6 percent to $73.0 billion.

The largest percentage reduction in spending occurs from decreases in rural road system expansion spending, which is reduced by 63.1 percent (from $6.9 billion to $2.5 billion) compared with actual 2014 spending. This indicates that HERS finds sustaining spending in rural expansion at current levels over 20 years not to be cost-beneficial. In contrast, the Improve Conditions and Performance scenario suggests that a 42.6-percent increase (from $15.2 to $21.7 billion) in funding for system expansion of urban roads would be cost-beneficial.

Significant reductions in some types of urban spending in the Improve Conditions and Performance scenario relative to 2014 occur as well. Spending on system rehabilitation of urban Interstate roads would be reduced by 20.3 percent, system expansion of urban other principal arterial roads by 33.2 percent, and system rehabilitation on urban other principal arterial bridges by 9.1 percent.

Spending on system rehabilitation for rural roads increases by 8.6 percent (from $15.6 billion to $16.9 billion) in the Improve Conditions and Performance scenario compared with actual 2014 spending, but that increase is significantly lower than the 42.6-percent increase (from $22.5 billion to $32.1 billion) in spending for system rehabilitation needed for urban roads. Bridges on both rural and urban roads, however, require substantial system rehabilitation spending, to achieve the goals of the scenario. The Improve Conditions and Performance scenario calls for 129.6-percent and 52.9-percent increases in system rehabilitation spending over actual 2014 spending for rural and urban bridges, respectively.

The Improve Conditions and Performance scenario suggests that the largest funding gaps (in percentage terms) are for bridge rehabilitation on the rural portion of the Interstate System (368.8 percent), system expansion for urban other freeways and expressways (167.7 percent), and highway system rehabilitation on urban minor arterials (117.5 percent).

Exhibit 7-7: Improve Conditions and Performance Scenario for Federal-aid Highways: Distribution of Average Annual Investment for 2015 Through 2034 Compared with Actual 2014 Spending by Functional Class and Improvement Type

| Average Annual National Investment on Federal-aid Highways (Billions of 2014 Dollars) | ||||||

|---|---|---|---|---|---|---|

| Functional Class | System Rehabilitation | System Expansion |

System Enhancement |

Total | ||

| Highway | Bridge | Total | ||||

| Rural Arterials and Major Collectors | ||||||

| Interstate | $4.2 | $2.3 | $6.6 | $0.6 | $0.9 | $8.0 |

| Other Principal Arterial | $5.9 | $1.3 | $7.2 | $1.0 | $0.9 | $9.0 |

| Minor Arterial | $3.1 | $1.1 | $4.2 | $0.3 | $0.8 | $5.4 |

| Major Collector | $3.7 | $2.1 | $5.8 | $0.7 | $0.8 | $7.3 |

| Subtotal | $16.9 | $6.8 | $23.7 | $2.5 | $3.4 | $29.7 |

| Urban Arterials and Collectors | ||||||

| Interstate | $7.7 | $5.6 | $13.3 | $8.7 | $1.5 | $23.5 |

| Other Freeway and Expressway | $3.4 | $1.5 | $4.9 | $4.7 | $0.9 | $10.5 |

| Other Principal Arterial | $9.0 | $2.1 | $11.1 | $3.4 | $2.2 | $16.8 |

| Minor Arterial | $8.1 | $1.6 | $9.7 | $3.5 | $1.7 | $14.8 |

| Collector | $3.9 | $0.8 | $4.6 | $1.3 | $1.3 | $7.3 |

| Subtotal | $32.1 | $11.6 | $43.7 | $21.7 | $7.7 | $73.0 |

| Total, Federal-aid highways1 | $49.0 | $18.4 | $67.4 | $24.2 | $11.1 | $102.7 |

| Percent Above Actual 2014 Capital Spending on Federal-aid Highways by All Levels of Government Combined |

||||||

|---|---|---|---|---|---|---|

| Functional Class | System Rehabilitation | System Expansion | System Enhancement | Total | ||

| Highway | Bridge | Total | ||||

| Rural Arterials and Major Collectors | ||||||

| Interstate | -11.3% | 368.8% | 24.5% | -53.8% | 29.6% | 11.1% |

| Other Principal Arterial | 34.6% | 109.3% | 43.7% | -73.4% | 29.6% | -4.0% |

| Minor Arterial | 1.9% | 37.6% | 9.4% | -75.6% | 29.6% | -6.0% |

| Major Collector | 8.9% | 99.2% | 30.1% | 0.3% | 29.6% | 26.6% |

| Subtotal | 8.6% | 129.6% | 27.8% | -63.1% | 29.6% | 5.7% |

| Urban Arterials and Collectors | ||||||

| Interstate | -20.3% | 109.9% | 7.9% | 89.5% | 29.6% | 30.0% |

| Other Freeway and Expressway | 103.4% | 104.2% | 103.7% | 167.7% | 29.6% | 115.5% |

| Other Principal Arterial | 87.1% | -9.1% | 56.0% | -33.2% | 29.6% | 19.9% |

| Minor Arterial | 117.5% | 43.3% | 100.1% | 45.3% | 29.6% | 74.1% |

| Collector | 48.0% | 4.9% | 38.4% | 3.1% | 29.6% | 28.7% |

| Subtotal | 42.6% | 52.9% | 45.2% | 42.6% | 29.6% | 42.6% |

| Total, Federal-aid highways1 | 28.7% | 74.5% | 38.6% | 9.7% | 29.6% | 29.6% |

1 The term "Federal-aid highways" refers to those portions of the road network that are generally eligible for Federal funding. Roads functionally classified as rural minor collectors, rural local, and urban local are excluded, although some types of Federal program funds can be used on such facilities.

Sources: Highway Economic Requirements System and National Bridge Investment Analysis System.

Highway and Bridge Investment Backlog

The investment backlog represents all highway and bridge improvements that could be economically justified for immediate implementation, based solely on the current conditions and operational performance of the highway system (without regard to potential future increases in VMT or potential future physical deterioration of infrastructure assets). Unlike NBIAS, HERS does not routinely produce rolling backlog figures over time as an output, but is equipped to do special analyses to identify the base-year backlog. Under this scenario analysis, any potential improvement that would correct an existing pavement or capacity deficiency and that has a benefit-cost ratio greater than or equal to 1.0 is considered part of the current highway and bridge investment backlog.

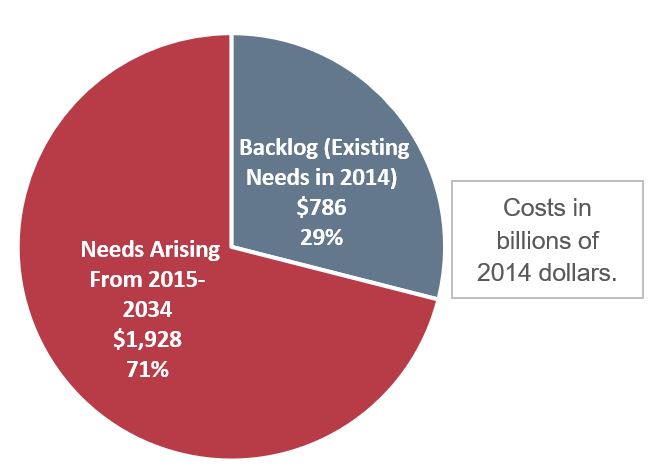

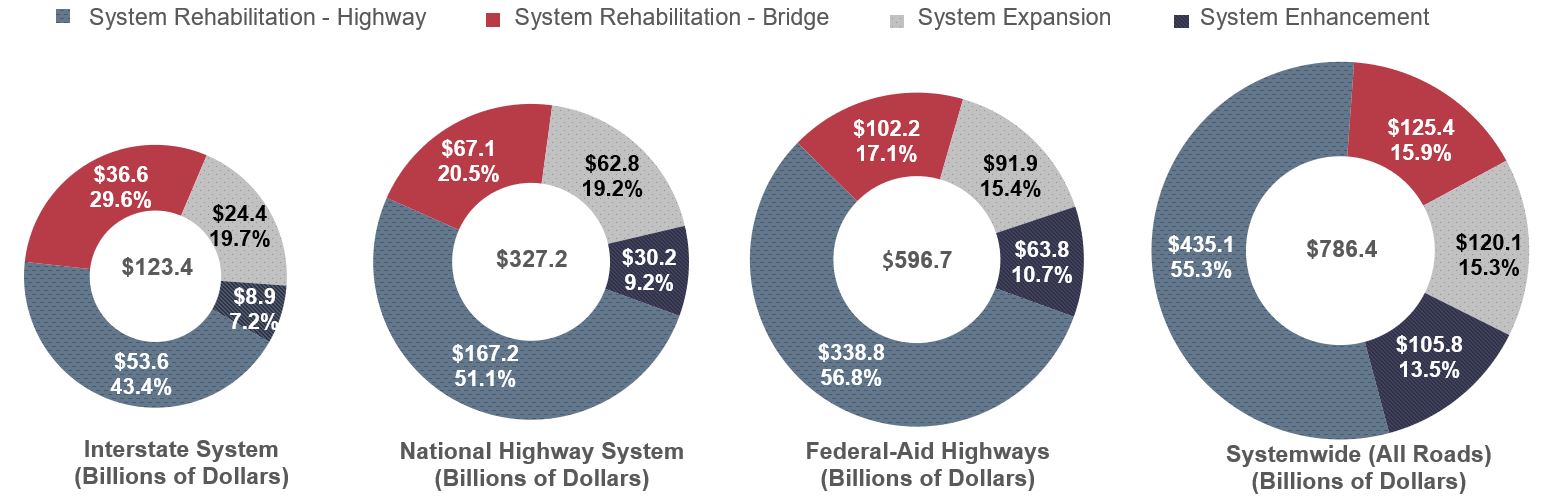

Conceptually, the backlog represents a subset of the investment levels reflected in the Improve Conditions and Performance scenario. Exhibit 7-2 had identified an average annual investment level of $135.7 billion for this scenario, for a 20-year total of approximately $2.7 trillion. Of this total, $786.4 billion (29.0 percent) is attributable to the existing backlog as of 2014, while the remainder is attributable to additional projected pavement, bridge, and capacity needs that might arise over the next 20 years (see Exhibit 7-8).

It should be noted that the procedures for estimating the backlog continue to be refined between C&P Report editions, so increases or decreases in the size of the estimated base-year backlog should not be interpreted as an indicator of changes in overall system conditions and performance.

Exhibit 7-9 presents an estimated distribution of the $786.4 billion backlog for 2014, by type of capital improvements. Similar to the process used to derive the capital investment scenario estimates, an adjustment factor was applied to the backlog values computed by HERS and NBIAS to account for nonmodeled capital improvement types. The values shown in italics are nonmodeled; NBIAS was used to compute the values in the System Rehabilitation — Bridge column, while all other values in the table were derived from HERS.

Of the estimated $786.4 billion total backlog, approximately $123.4 billion (15.7 percent) is for the Interstate System, $327.2 billion (41.6 percent) is for the NHS, and $596.7 billion (75.9 percent) is for Federal-aid highways.

Exhibit 7-8: Composition of 20-Year Improve Conditions and Performance Scenario, Backlog vs. Emerging Needs

Source: Highway Economic Requirements System and National Bridge Investment Analysis System.

Why does the bridge backlog presented in Exhibit 7-9 differ from bridge backlog figures estimated by some other organizations?

One major reason for such differences is that the $125.4 billion backlog estimated by NBIAS is not intended to constitute a complete bridge investment estimate backlog. The NBIAS figures relate only to investment needs associated with the condition of existing structures, and not capacity expansion needs. The backlog HERS estimates includes estimates of capacity-related needs for highways and bridges combined.

Some estimates of bridge backlog produced by other organizations do attempt to combine estimates of needs relating to bridge capacity with those relating to existing structures.

Exhibit 7-9: Estimated Highway and Bridge Investment Backlog, by System and Improvement Type, as of 2014

| System Component | Billions of 2014 Dollars1 | Percent of Total | |||||

|---|---|---|---|---|---|---|---|

| System Rehabilitation | System Expansion | System Enhancement | Total | ||||

| Highway | Bridge | Total | |||||

| Federal-aid Highways—Rural |

$95.1 | $35.0 | $130.2 | $16.3 | $19.6 | $166.1 | 21.1% |

| Federal-aid Highways—Urban |

$243.6 | $67.2 | $310.8 | $75.6 | $44.2 | $430.5 | 54.7% |

| Federal-aid Highways—Total |

$338.8 | $102.2 | $441.0 | $91.9 | $63.8 | $596.7 | 75.9% |

| Non-Federal-aid Highways | $96.3 | $23.1 | $119.5 | $28.2 | $42.0 | $189.7 | 24.1% |

| All Public Roads | $435.1 | $125.4 | $560.4 | $120.1 | $105.8 | $786.4 | 100.0% |

| Interstate System | $53.6 | $36.6 | $90.1 | $24.4 | $8.9 | $123.4 | 15.7% |

| National Highway System | $167.2 | $67.1 | $234.2 | $62.8 | $30.2 | $327.2 | 41.6% |

1 Italicized values are estimates for those system components and capital improvement types not modeled in HERS or NBIAS, such as system enhancements and pavement and expansion improvements to roads functionally classified as rural minor collector, rural local, or urban local for which HPMS data are not available to support a HERS analysis.

Sources: Highway Economic Requirements System and National Bridge Investment Analysis System.

Approximately 71.2 percent ($560.4 billion) of the total backlog is attributable to system rehabilitation needs, 15.3 percent ($120.1 billion) is for system expansion, and 13.5 percent ($105.8 billion) for system enhancement. The share of the total backlog attributable to system rehabilitation is roughly similar across all highway systems.

The $786.4-billion estimated backlog is weighted toward urban areas; approximately 54.7 percent of this total is attributable to Federal-aid highways in urban areas. As noted in Chapter 6, average pavement ride quality on Federal-aid highways is worse in urban areas than in rural areas; urban areas also face relatively greater problems with congestion than do rural areas. Very little of the backlog spending (just 2.1 percent) is targeted toward system expansion on rural Federal-aid highways.

Key Takeaways

- Backlog

- The backlog is estimated at $98.8 billion in 2014.

- An estimated $18.4 billion in annual reinvestment would be required to fully eliminate the SGR backlog by 2034.

- Current Investment

- If the level of investment in preservation is maintained at the 2014 level ($11.3 billion), the backlog would be projected to climb from $98.2 billion to $116.2 billion by 2034 (an increase of $18.0 billion or 19 percent).

- Expansion Investment Scenarios

- In addition to $18.4 billion annually to eliminate the backlog in 2034, the following investment levels in expansion would be required for the Low- and High-Growth scenarios.

- Low-Growth Scenario – The Low-Growth scenario forecasts $6.0 billion per year investment in new assets to accommodate an estimated annual ridership increase of 1.2 percent (20 percent below historical growth).

- High-Growth Scenario – In the High-Growth scenario, investments of $8.1 billion are needed to support a ridership increase of 1.8 percent per year (20 percent higher than historical growth).

Transit Capital Investment Scenarios

Chapter 10 considers the impacts of varying levels of capital investment on transit conditions and performance. This chapter provides in-depth analysis of three specific investment scenarios, as outlined in Exhibit 7-10. The Sustain 2014 Spending scenario assesses the effects on asset conditions and system performance that would result from sustaining 2014 expenditure levels over the next 20 years. Given that current expenditures are generally less than are required to maintain current condition and performance levels, this scenario reflects the magnitude of the expected declines in condition and performance should current capital investment rates be maintained. The Low-Growth and High-Growth scenarios both assess the required levels of reinvestment to (1) preserve existing transit assets at a condition rating of 2.5 or higher and (2) expand transit service capacity to support differing levels of ridership growth while passing TERM’s benefit-cost test.

The State of Good Repair (SGR) Benchmark considers the level of investment required to eliminate the existing capital investment backlog and the condition and performance impacts of doing so. In contrast to the three investment scenarios considered here, the SGR Benchmark considers only the preservation needs of existing transit assets (it does not consider expansion requirements). Moreover, the SGR Benchmark does not require investments to pass the Transit Economic Requirements Model’s (TERM’s) benefit-cost test. Hence, it brings all assets to an SGR regardless of TERM’s assessment of whether reinvestment is warranted and should thus be considered illustrative rather than a subset of the primary investment scenarios.

TERM’s estimates for capital expansion needs in the Low- and High-Growth scenarios are driven by the projected growth in passenger miles traveled (PMT) based on the trend rate of growth in PMT, calculated as the compound average annual PMT growth by FTA region, urbanized area (UZA) stratum, and mode over the most recent 15-year period. For example, all bus operators located in the same FTA region in UZAs of the same population stratum are assigned the same growth rate. Use of the 10 FTA regions captures regional differences in PMT growth, while use of population strata (greater than 1 million; 1 million to 500,000; 500,000 to 250,000; and less than 250,000) captures differences in urban area size. Perhaps more importantly, the approach also recognizes differences in PMT growth trends by transit mode. Over the past decade, the rate of PMT growth has differed markedly across transit modes: highest for heavy rail, vanpool, and demand-response, and low to flat for motor bus. These differences are accounted for in the expansion need projections for the Low- and High-Growth scenarios.

Exhibit 7-10: SGR Benchmark and Transit Investment Scenarios

| Scenario Aspect | SGR | Sustain 2014 Spending | Low Growth | High Growth |

|---|---|---|---|---|

| Description | Level of investment to attain and maintain SGR over next 20 years (no assessment of expansion needs) | Sustain preservation and expansion spending at 2014 levels over next 20 years | Preserve existing assets and expand asset base to support historical rate of ridership growth less 0.3%, which equals to 1.2% | Preserve existing assets and expand asset base to support historical rate of ridership growth plus 0.3%, which equals to 1.8% |

| Objective | Requirements to attain SGR (as defined by assets in condition 2.5 or better) | Assess impact of constrained funding on condition, SGR backlog, and ridership capacity | Assess unconstrained preservation and capacity expansion needs assuming low ridership growth | Assess unconstrained preservation and capacity expansion needs assuming high ridership growth |

| Apply Benefit-Cost Test? | No | Yes1 | Yes | Yes |

| Preservation? | Yes2 | Yes2 | Yes2 | Yes2 |

| Expansion? | No | Yes | Yes | Yes |

1To prioritize investments under constrained funding.

2Replace at condition 2.5.

Exhibit 7-11 summarizes the analysis results for each scenario. Note that each scenario presented in Exhibit 7-11 imposes the same asset condition replacement threshold (i.e., assets are replaced at condition rating of 2.5 when budget is sufficient) when assessing transit reinvestment needs. Hence, the differences in the total preservation expenditure amounts across each scenario primarily reflect the impact of either (1) an imposed budget constraint (Sustain 2014 Spending scenario) or (2) application of TERM’s benefit-cost test. (The SGR Benchmark does not apply the benefit-cost test.) A brief review of the national-level needs analysis in Exhibit 7-11 reveals the following:

- SGR Benchmark: The level of expenditures required to attain and maintain an SGR over the upcoming 20 years, which would cover preservation needs but excludes expansion investments, is 4.0 percent higher than that currently expended on asset preservation and expansion combined.

- Sustain 2014 Spending scenario: Total spending under this scenario is well below that of the other scenarios, indicating that sustaining recent spending levels is insufficient to attain the investment objectives of the SGR Benchmark, the Low-Growth scenario, or the High-Growth scenario. This result suggests future increases in the size of the SGR backlog and a likely increase in the number of transit riders per peak vehicle—including an increased incidence of crowding—in the absence of increased expenditures.

- Low- and High-Growth scenarios1: The level of investment to address expected preservation and expansion needs is estimated to be roughly 26 to 41 percent higher than that currently expended by the Nation’s transit operators. Preservation and expansion needs are highest for UZAs exceeding 1 million in population. (These UZAs are listed in Chapter 1, Exhibit 1-16).

Exhibit 7-11: Annual Average Cost by Investment Scenario, 2014–2034

| Mode, Purpose, and Asset Type | SGR Benchmark | Sustain 2014 Spending | Low Growth | High Growth |

|---|---|---|---|---|

| Urbanized Areas Over 1 Million in Population1 | ||||

| Nonrail2 | ||||

| Preservation | $5.1 | $3.3 | $4.5 | $4.5 |

| Expansion | NA | $0.4 | $0.4 | $0.8 |

| Subtotal Nonrail3 | $5.1 | $3.7 | $4.9 | $5.3 |

| Rail | ||||

| Preservation | $11.5 | $6.6 | $11.4 | $11.4 |

| Expansion | NA | $5.5 | $5.2 | $6.6 |

| Subtotal Rail3 | $11.5 | $12.2 | $16.5 | $18.0 |

| Total, Over 1 Million in Population3 | $16.6 | $15.9 | $21.4 | $23.3 |

| Urbanized Areas Under 1 Million in Population and Rural | ||||

| Nonrail2 | ||||

| Preservation | $1.6 | $1.3 | $1.5 | $1.5 |

| Expansion | NA | $0.5 | $0.5 | $0.7 |

| Subtotal Nonrail3 | $1.6 | $1.7 | $1.9 | $2.1 |

| Rail | ||||

| Preservation | $0.2 | $0.1 | $0.1 | $0.1 |

| Expansion | NA | $0.0 | $0.0 | $0.0 |

| Subtotal Rail3 | $0.2 | $0.1 | $0.1 | $0.1 |

| Total, Under 1 Million and Rural3 | $1.8 | $1.8 | $2.0 | $2.2 |

| Total3 | $18.4 | $17.7 | $23.4 | $25.5 |

1Includes 37 urbanized areas.

2Buses, vans, and other (including ferryboats).

3Note that totals may not sum due to rounding.

Source: Transit Economic Requirements Model.

The following subsections present more details on the assessments for each scenario.

Sustain 2014 Spending Scenario

In 2014, as reported to the National Transit Database (NTD) by transit agencies, transit operators spent an average of $17.7 billion annually on capital projects (see Chapter 10, Impact of Preservation Investments on Transit Backlog and Conditions section and the corresponding discussion). Of this amount, $11.3 billion was dedicated to preserving existing assets, while the remaining $6.4 billion was dedicated to investing in asset expansion—to support ongoing ridership growth and to improve service performance. The Sustain 2014 Spending scenario considers the expected impact on the long-term physical condition and service performance of the Nation’s transit infrastructure if these average expenditure levels were to be sustained in current dollar terms through 2034. Similar to the discussion in Chapter 10, the analysis considers the impacts of asset-preservation investments separately from those of asset expansion.

TERM’s Funding Allocation: The following analysis of the Sustain 2014 Spending scenario relies on TERM’s allocation of 2014-level preservation and expansion expenditures to the Nation’s existing transit operators, their modes, and their assets over the upcoming 20 years, as depicted in Exhibit 7-12. As with other TERM analyses involving the allocation of constrained transit funds, TERM allocates limited funds based on the results of the model’s benefit-cost analysis, which ranks potential investments based on their assessed benefit-cost ratios (with the highest-ranked investments funded first). Note that this TERM benefit-cost-based allocation of funding between assets and modes could differ from the allocation that local agencies actually pursue, assuming that total spending is sustained at current levels over 20 years.

Exhibit 7-12: Sustain 2014 Spending Scenario: Average Annual Investment by Asset Type, 2014–2034

| Asset Type | Average annual Investment (Billions of 2014 Dollars) | ||

|---|---|---|---|

| Preservation | Expansion | Total | |

| Rail | |||

| Guideway Elements | $2.5 | $1.0 | $3.5 |

| Facilities | $0.0 | $0.2 | $0.2 |

| Systems | $2.3 | $0.2 | $2.5 |

| Stations | $0.2 | $0.8 | $1.0 |

| Vehicles | $1.8 | $2.0 | $3.7 |

| Other Project Costs | $0.0 | $1.3 | $1.3 |

| Subtotal Rail* | $6.7 | $5.5 | $12.3 |

| Subtotal UZAs Over 1 Million1 | $6.6 | $5.5 | $12.2 |

| Subtotal UZAs Under 1 Million and Rural1 | $0.1 | $0.0 | $0.1 |

| Nonrail | |||

| Guideway Elements | $0.0 | $0.0 | $0.0 |

| Facilities | $0.0 | $0.1 | $0.1 |

| Systems | $0.1 | $0.0 | $0.1 |

| Stations | $0.0 | $0.0 | $0.0 |

| Vehicles | $4.5 | $0.7 | $5.2 |

| Other Project Costs | $0.0 | $0.0 | $0.0 |

| Subtotal Nonrail* | $4.6 | $0.9 | $5.5 |

| Subtotal UZAs Over 1 Million1 | $3.3 | $0.4 | $3.7 |

| Subtotal UZAs Under 1 Million and Rural1 | $1.3 | $0.5 | $1.7 |

| Total | $11.3 | $6.4 | $17.7 |

| Total UZAs Over 1 Million | $9.9 | $6.0 | $15.9 |

| Total UZAs Under 1 Million and Rural | $1.4 | $0.5 | $1.8 |

1Note that totals may not sum due to rounding.

Source: Transit Economic Requirements Model and FTA staff estimates.

Preservation Investments

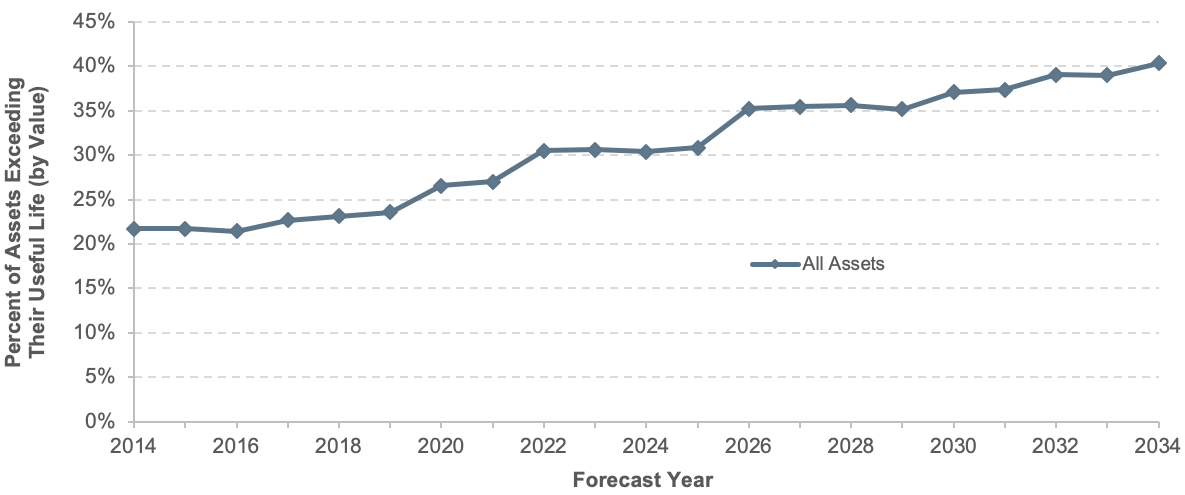

As noted above, transit operators spent an estimated $11.3 billion in 2014 rehabilitating and replacing existing transit infrastructure. Based on current TERM analyses, this level of reinvestment is less than that required to address the anticipated reinvestment needs of the Nation’s existing transit assets. If sustained over the forecasted 20 years, this level would result in an overall decline in the condition of existing transit assets and an increase in the size of the investment backlog. One impact of this underinvestment is shown in Exhibit 7-13, which presents the proportion of existing transit assets (by value) that are estimated to exceed their useful life. Under the Sustain Spending scenario, this amount is projected to increase from 22 percent of all transit assets in 2014 to roughly 40 percent in 2034.

Exhibit 7-13: Sustain 2014 Spending Scenario: Percentage of Assets Exceeding Useful Life, 2014–2034

Note: The proportion of assets exceeding their useful life is measured based on asset replacement value, not asset quantities.

Source: Transit Economic Requirements Model.

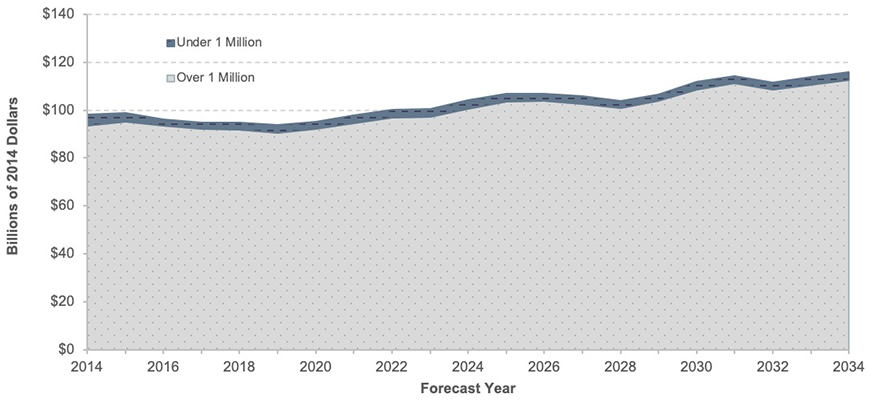

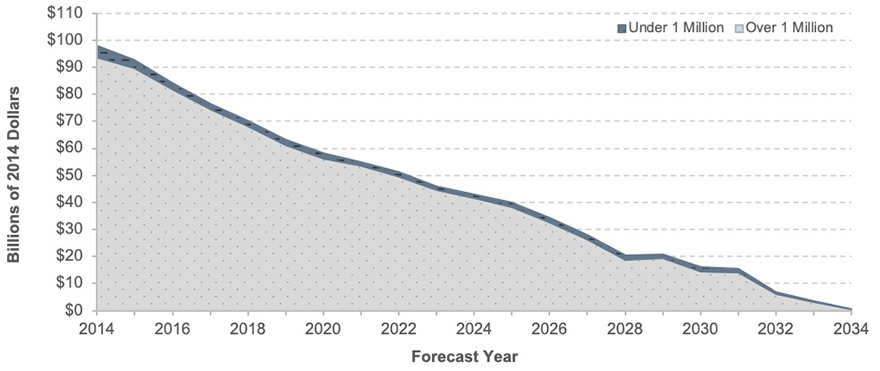

Finally, Exhibit 7-14 presents the projected change in the size of the investment backlog if reinvestment levels are sustained at the 2014 level of $11.3 billion, in constant dollar terms. As described in Chapter 10, the investment backlog represents the level of investment required to replace all assets that exceed their useful life and to address all rehabilitation activities that are currently past due. Rural and smaller urban needs are estimated using NTD records for vehicle ages and types, and from records generated for rural smaller urban agency facilities based on counts from NTD. The generated records for rural facilities include estimated facility size, replacement cost, and date built. Each estimated value was substantially revised for this C&P Report for two reasons: (1) The replacement costs for facilities used in previous reports were much higher than the costs rural and smaller urban agencies typically face; and (2) Some values for the year a facility was built, known as “date-built values,” were much greater (i.e., the facilities were older) than is typical. For this report, facility size and cost were reassessed based on agency fleet size and facility cost per vehicle. The age range used to generate date-built values also was tightened to recognize a more realistic distribution of facility ages, based on sample data. These changes significantly reduced the value of these assets and size of the rural and smaller urban backlogs. As the current rate of capital reinvestment would be insufficient to address the projected replacement needs of the existing stock of transit assets, the size of that backlog would be projected to increase from the currently estimated level of $98.0 billion to roughly $116 billion by 2034.

The chart in Exhibit 7-14 also divides the backlog amount according to size of transit service area, with the lower portion showing the backlog for UZAs having populations greater than 1 million and the upper portion showing the backlog for all other UZAs and rural areas combined. This segmentation highlights the significantly higher existing backlog for those UZAs serving the largest number of transit riders. Regardless of the actual allocation, the 2014 expenditure level of $11.3 billion, if sustained, clearly is not sufficient to prevent a further increase in the backlog needs of one or more of these UZA types.

Exhibit 7-14: Projected Backlog under the Sustain 2014 Spending Scenario, 2014–2034

Note: The proportion of assets exceeding their useful life is measured based on asset replacement value, not asset quantities.

Source: Transit Economic Requirements Model.

Expansion Investments

In addition to the average $11.3 billion spent on preserving transit assets in 2014, transit agencies spent an average of $6.4 billion on expansion investments to support ridership growth and improve transit performance. This section considers the impact of sustaining the 2014 level of expansion investment on future ridership capacity and vehicle utilization rates under the assumptions of both lower and higher growth rates in ridership (i.e., the Low-Growth and High-Growth scenarios).

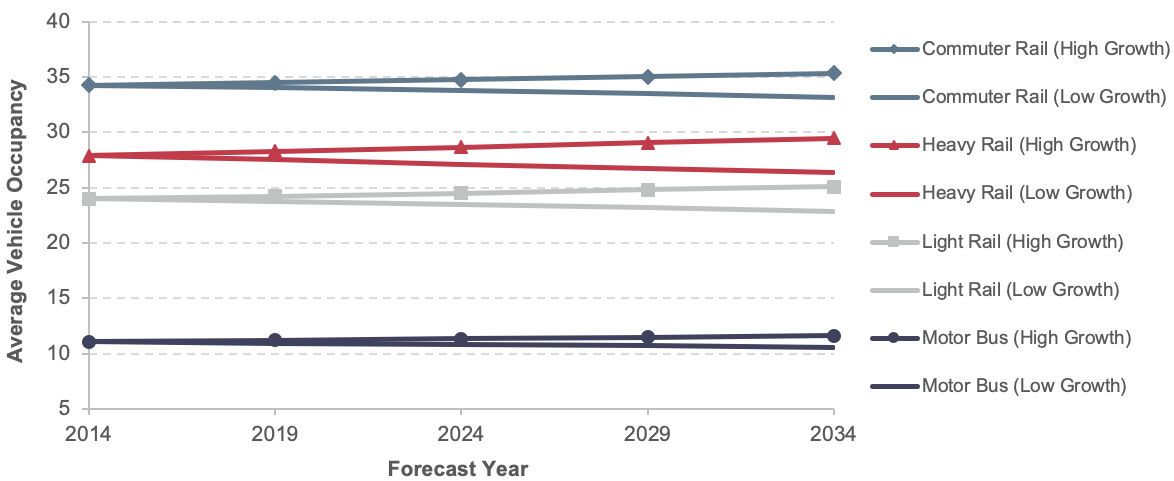

As considered in Chapter 10, the 2014 rate of investment in transit expansion is not sufficient to expand transit capacity at a rate equal to the rate of growth in travel demand, as projected by the historical trend rate of increase. Under these circumstances, transit capacity utilization (the average number of riders per transit vehicle) should be expected to increase, with the level of increase determined by actual growth in demand. Although the impact of this change could be minimal for systems that currently have lower-capacity utilization, service performance on some higher-utilization systems likely would decline as riders experience increased vehicle crowding and service delays. Exhibit 7-15 illustrates this potential impact. It presents the projected change in vehicle occupancy rates by mode from 2014 through 2034 (reflecting the impacts of spending from 2014 through 2034) under both the Low-Growth and High-Growth scenarios in transit ridership, assuming that transit agencies continue to invest an average of $6.4 billion per year on transit expansion. Under the Low-Growth scenario, capacity utilization decreases across each of the four modes depicted here, indicating that investment is sufficient or higher than needed to maintain current occupancy levels. For the High-Growth scenario, however, the average number of riders per transit vehicle rises steadily across each mode. Chapter 8 provides more detail on the methodology for both the Low- and High-Growth scenarios.

Exhibit 7-15: Sustain 2014 Spending Scenario: Capacity Utilization by Mode Forecast, 2014–2034

Source: Transit Economic Requirements Model.

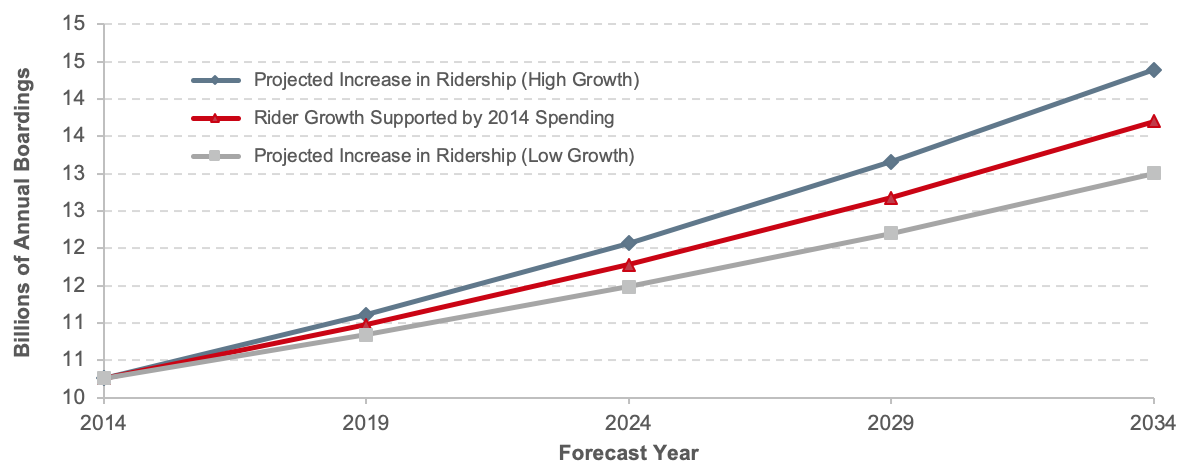

Exhibit 7-16 presents the projected growth in transit riders that the 2014 level of investment (keeping vehicle occupancy rates constant) can accommodate compared with the potential growth in total ridership under both the Low-Growth and High-Growth scenarios. The $6.4 billion level of investment for expansion can support ridership growth that is similar to the ridership increases projected in the Low-Growth scenario, but is short of that required to support continued ridership under the High-Growth scenario (i.e., without impacting service performance).

Exhibit 7-16: Projected Versus Currently Supported Ridership Growth

Source: Transit Economic Requirements Model.

State of Good Repair Benchmark

The Sustain 2014 Spending scenario considered the impacts of sustaining transit spending at current levels, which appear to be insufficient to address either deferred investment needs (which are projected to increase) or the projected growth in transit ridership (without a reduction in service performance). In contrast, this section focuses on the level of investment required to eliminate the investment backlog over the next 20 years and to provide for sustainable rehabilitation and replacement needs once the backlog has been addressed. Specifically, the SGR Benchmark estimates the level of annual investment required to replace assets that currently exceed their useful lives, to address all deferred rehabilitation activities (yielding an SGR where the asset has a condition rating of 2.5 or higher), and to address all future rehabilitation and replacement activities as they come due. The SGR Benchmark considered here uses the same methodology as that described in FTA’s National State of Good Repair Assessment, released June 2012.

What is the definition of state of good repair (SGR)?

The definition of “state of good repair” used for the SGR Benchmark relies on TERM’s assessment of transit asset conditions. Specifically, for this benchmark, TERM considers assets to be in a state of good repair if they are rated at condition 2.5 or higher and if all required rehabilitation activities have been addressed.

Differences from Scenarios: In contrast to the scenarios described in this chapter, the SGR Benchmark does not (1) assess expansion needs or (2) apply TERM’s benefit-cost test to investments proposed in TERM. These benchmark characteristics are inconsistent with the SGR concept. First, analyses of expansion investments ultimately focus on capacity improvements and not on the needs of deteriorated assets. Second, this is a purely engineering-based performance benchmark that assesses reinvestment levels for all transit assets currently in service, regardless of whether having these assets remain in service would be cost-beneficial.

SGR Investment Levels

Annual reinvestment levels under the SGR Benchmark are presented in Exhibit 7-17. Under this benchmark, an estimated $18.4 billion in annual expenditures would be required over the next 20 years to bring the condition of all existing transit assets to an SGR. Of this amount, roughly $12.1 billion (66 percent) is required to bring rail assets to SGR. Note that a large proportion of rail reinvestment spending would be associated with guideway elements (primarily aging elevated and tunnel structures) and rail systems (including train control, traction power, and communications systems) that are past their useful lives and potentially are technologically obsolete. Bus-related reinvestment spending under this benchmark is primarily associated with aging vehicle fleets.

Exhibit 7-17 also provides a breakout of capital reinvestment by type of UZA under this benchmark. This breakout emphasizes the fact that capital reinvestment levels to achieve SGR are most heavily concentrated in the Nation’s larger UZAs. Together, these urban areas account for approximately 90 percent of total reinvestment under the benchmark (across all mode and asset types), with the rail reinvestment in these urban areas accounting for more than half the total reinvestment required to bring all assets to an SGR. This high proportion of total needs reflects the high level of investment in older assets found in these urban areas.

Exhibit 7-17: SGR Benchmark: Average Annual Investment by Asset Type, 2014–2034

| Asset Type | Average Annual Investment (Billions of 2014 Dollars) | ||

|---|---|---|---|

| Urban Area Type | |||

| Over 1 Million Population | Under 1 Million Population | Total | |

| Rail | |||

| Guideway Elements | $3.3 | $0.1 | $3.4 |

| Facilities | $0.8 | $0.0 | $0.9 |

| Systems | $3.0 | $0.0 | $3.0 |

| Stations | $2.2 | $0.0 | $2.2 |

| Vehicles | $2.5 | $0.1 | $2.6 |

| Subtotal Rail1 | $11.9 | $0.3 | $12.1 |

| Nonrail | |||

| Guideway Elements | $0.1 | $0.0 | $0.1 |

| Facilities | $0.9 | $0.1 | $1.0 |

| Systems | $0.3 | $0.0 | $0.3 |

| Stations | $0.2 | $0.0 | $0.2 |

| Vehicles | $3.3 | $1.4 | $4.6 |

| Subtotal Nonrail1 | $4.8 | $1.5 | $6.2 |

| Total1 | $16.6 | $1.8 | $18.4 |

1Note that totals may not sum due to rounding.

Source: Transit Economic Requirements Model.

Impact on the Investment Backlog

A key objective of the SGR Benchmark is to determine the level of investment required to attain and then maintain an SGR across all transit assets over the next 20 years, including elimination of the existing investment backlog. Exhibit 7-18 shows the estimated impact of the $17.5 billion in annual expenditures under the SGR Benchmark on the existing investment backlog over the 20-year forecast period (compare these data with Exhibit 7-14). Given this level of expenditures, the backlog is projected to be eliminated by 2034, with most of this drawdown addressing reinvestment in UZAs having populations greater than 1 million.

Exhibit 7-18: Investment Backlog: State of Good Repair Benchmark ($17.5 Billion Annually)

Source: Transit Economic Requirements Model.

Impact on Conditions

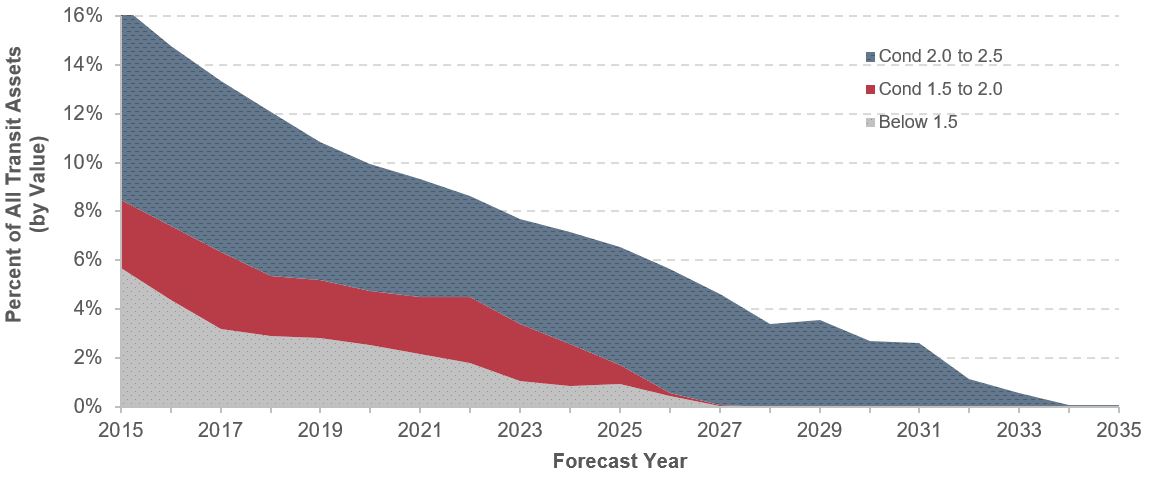

In drawing down the investment backlog, the annual capital expenditures of $17.5 billion under the SGR Benchmark also would lead to the replacement of assets with an estimated condition rating of 2.5 or less. Within TERM’s condition rating system, these assets would include those in marginal condition having ratings less than 2.5 and all assets in poor condition. Exhibit 7-19 shows the current distribution of asset conditions for assets estimated to be in a rating condition of 2.5 or less (with assets in poor condition divided into two subgroups). Note that this graphic excludes both tunnel structures and subway stations in tunnel structures because these are considered assets that require ongoing capital rehabilitation expenditures but that are never actually replaced. As with the investment backlog, the proportion of assets at condition rating 2.5 or lower is projected to decrease under the SGR Benchmark from roughly 16 percent of assets in 2015 to less than 1 percent by 2035. Once again, this replacement activity would remove from service those assets with higher occurrences of service failures, technological obsolescence, and lower overall service quality. Importantly, the assets with a condition rating of less than 2.5 presented in Exhibit 7-19 capture only a subset of assets in the SGR backlog as depicted in Exhibit 7-18. Specifically, the total SGR backlog (Exhibit 7-18) includes not just those assets in need of replacement (i.e., those at less than condition 2.5), but also those assets in need of rehabilitation or other form of capital reinvestment.

Exhibit 7-19: Proportion of Transit Assets Not in State of Good Repair (Excluding Tunnel Structures)

Source: Transit Economic Requirements Model.

Low-Growth and High-Growth Scenarios

The SGR Benchmark considered the level of investment required to bring existing transit assets to an SGR, but in doing so did not consider either (1) the economic feasibility of these investments (investments were not required to pass TERM’s benefit-cost test) or (2) the level of expansion investment required to support projected ridership growth. The Low-Growth scenario and High-Growth scenario address both of these issues. Specifically, these scenarios use the same rules to assess when assets should be rehabilitated or replaced that were applied in the SGR Benchmark (e.g., with assets being replaced at condition 2.5), but also require that these preservation and expansion investments pass TERM’s benefit-cost test. In general, some reinvestment activities do not pass this test (i.e., have a benefit-cost ratio less than 1), which can result from low ridership benefits, higher capital or operating costs, or a mix of these factors. Excluding investments that do not pass the benefit-cost test has the effect of reducing total estimated needs.

In addition, the Low- and High-Growth scenarios assess transit expansion needs given ridership growth based on the average annual compound rate experienced over the past 15 years, minus 0.3 percent (Low-Growth) or plus 0.3 percent (High-Growth). For the expansion component of this scenario, TERM assesses the level of investment required to maintain current vehicle occupancy rates (at the agency-mode level) subject to the rate of projected growth in transit demand in that UZA and subject to the proposed expansion investment passing TERM’s benefit-cost test.

Low-Growth and High-Growth Assumptions

The Low-Growth scenario is intended to represent a lower level of investment required to maintain current service performance (as measured by transit vehicle capacity utilization) as determined by a relatively lower rate of growth in travel demand. In contrast, the High-Growth scenario estimates the higher level of investment required to maintain current service performance as determined by a relatively higher rate of growth in travel demand. The methodology for the Low- and High-Growth scenarios uses a common, consistent approach that better reflects differences in PMT growth by mode. Specifically, these scenarios are based on the 15-year trend rate of growth in PMT, which is used to project future growth. When calculated across all transit operators and modes, this historical trend rate of growth converts to a national average compound annual growth rate of approximately 1.5 percent during the 20-year period.

Within this new framework, the Low-Growth scenario is defined as the trend rate of growth (by FTA region, population stratum, and mode) less 0.3 percent, while the High-Growth scenario is defined as the trend rate of growth plus 0.3 percent. Hence, the Low-Growth and High-Growth scenarios differ by a full 0.6 percent in annual growth.

Low-Growth and High-Growth Scenario Investment Levels

Exhibit 7-20 presents TERM’s projected capital investment levels on an annual average basis under the Low- and High-Growth scenarios, including those for both asset preservation and asset expansion.

Assuming the relatively low ridership growth in the Low-Growth scenario, investment needs for system preservation and expansion are estimated to average roughly $23.4 billion each year for the next two decades. Of this amount, roughly 74 percent is for preserving existing assets and approximately $11.5 billion is associated with preserving existing rail infrastructure alone. Note that the approximate $1 billion difference between the $18.4 billion in annual preservation spending under the SGR Benchmark and the $17.4 billion in preservation spending under the Low-Growth scenario is due entirely to the application of TERM’s benefit-cost test under the Low-Growth scenario. Finally, expansion needs in this scenario total $6.0 billion annually, with 86 percent of that amount associated with rail expansion costs.

In contrast, total investment needs under the High-Growth scenario are estimated to be $25.5 billion annually, a 9-percent increase over the total investment needs under the Low-Growth scenario. The High-Growth scenario total includes $17.5 billion for system preservation and an additional $8.1 billion for system expansion. Note that system preservation costs are higher under the High-Growth scenario because the higher growth rate leads to a larger expansion of the asset base compared with that under the Low-Growth scenario. Under this scenario, investment in expansion of rail assets is still larger than that for nonrail expansion (81 percent for rail and 19 percent for nonrail). Under the High-Growth scenario, however, rail takes 81 percent of total expansion investment versus 85 percent of expansion needs under the Low-Growth scenario.

Exhibit 7-20: Low- and High-Growth Scenarios: Average Annual Investment by Asset Type, 2014–2034

| Asset Type | Average Annual Investment (Billions of 2014 Dollars) | |||||

|---|---|---|---|---|---|---|

| Low-Growth | High-Growth | |||||

| Preservation | Expansion | Total | Preservation | Expansion | Total | |

| Rail | ||||||

| Guideway Elements | $3.3 | $1.0 | $4.2 | $3.3 | $1.2 | $4.5 |

| Facilities | $0.8 | $0.2 | $1.0 | $0.8 | $0.2 | $1.1 |

| Systems | $3.0 | $0.2 | $3.2 | $3.0 | $0.3 | $3.3 |

| Stations | $2.2 | $0.7 | $2.9 | $2.2 | $0.9 | $3.1 |

| Vehicles | $2.2 | $1.8 | $4.0 | $2.2 | $2.5 | $4.7 |

| Other Project Costs | $0.0 | $1.2 | $1.2 | $0.0 | $1.5 | $1.5 |

| Subtotal Rail1 | $11.5 | $5.2 | $16.6 | $11.5 | $6.6 | $18.1 |

| Subtotal UZAs Over 1 Million1 | $11.4 | $5.2 | $16.5 | $11.4 | $6.6 | $18.0 |

| Subtotal UZAs Under 1 Million and Rural1 | $0.1 | $0.0 | $0.1 | $0.1 | $0.0 | $0.1 |

| Nonrail | ||||||

| Guideway Elements | $0.1 | $0.0 | $0.1 | $0.1 | $0.1 | $0.1 |

| Facilities | $0.9 | $0.1 | $1.0 | $0.9 | $0.2 | $1.1 |

| Systems | $0.2 | $0.0 | $0.2 | $0.2 | $0.0 | $0.2 |

| Stations | $0.2 | $0.0 | $0.2 | $0.2 | $0.0 | $0.2 |

| Vehicles | $4.6 | $0.7 | $5.2 | $4.6 | $1.1 | $5.7 |

| Other Project Costs | $0.0 | $0.0 | $0.0 | $0.0 | $0.1 | $0.1 |

| Subtotal Nonrail* | $5.9 | $0.9 | $6.8 | $5.9 | $1.5 | $7.4 |

| Subtotal UZAs Over 1 Million1 | $4.5 | $0.4 | $4.9 | $4.5 | $0.8 | $5.3 |

| Subtotal UZAs Under 1 Million and Rural1 | $1.6 | $0.5 | $2.0 | $1.5 | $0.7 | $2.1 |

| Total Investment1 | $17.4 | $6.0 | $23.4 | $17.5 | $8.1 | $25.5 |

| Total UZAs Over 1 Million1 | $15.8 | $5.6 | $21.4 | $15.9 | $7.4 | $23.3 |

| Total UZAs Under 1 Million and Rural1 | $1.7 | $0.5 | $2.1 | $1.6 | $0.7 | $2.2 |

1Note that totals may not sum due to rounding.

Source: Transit Economic Requirements Model.

Impact on Conditions and Performance

The impact of the Low- and High-Growth rate preservation investments on transit conditions is essentially the same as that already presented for the SGR Benchmark in Exhibits 7-18 and 7-19. As noted above, the Low and High-Growth scenarios use the same rules to assess when assets should be rehabilitated or replaced as were applied in the SGR Benchmark (e.g., with all assets being replaced at condition rating 2.5). In terms of asset conditions, the primary difference between the SGR Benchmark and the Low- and High-Growth scenarios relates to (1) TERM’s benefit-cost test not applying to the SGR Benchmark (leading to higher SGR preservation spending overall) and (2) the Low- and High-Growth scenarios having some additional spending for replacing expansion assets with short service lives. Together, these impacts tend to work in opposite directions. The result is that the rate of drawdown in the investment backlog and the elimination of assets exceeding their useful lives are roughly comparable between the SGR Benchmark and these scenarios and between the two scenarios.

Similarly, the impact of the Low- and High-Growth rate expansion investments on transit ridership was considered in Exhibit 7-16. That analysis demonstrated the significant difference in the level of ridership growth supported by the High-Growth scenario compared with either the current level of expenditures (average $5.9 billion annually in 2014 for UZAs with populations greater than 1 million) or the rate of growth supported under the Low-Growth scenario.

Scenario Impacts Comparison

Finally, this subsection summarizes and compares many of the investment impacts associated with each of the three analysis scenarios and the SGR Benchmark considered above. Although much of this comparison is based on measures already introduced above, this discussion also considers a few additional investment impact measures. These comparisons are presented in Exhibit 7-21. Note that the first column of data in Exhibit 7-21 presents the current values for each of these measures (as of 2014). The subsequent columns present the estimated future values in 2034, assuming the levels, allocations, and timing of expenditures associated with each of the three investment scenarios and the SGR Benchmark.

Exhibit 7-21 includes the following measures:

- Average annual expenditures (billions of dollars): This amount is broken down into preservation and expansion expenditures.

- Condition of existing assets: This analysis considers only the impact of investment funds on the condition of those assets currently in service.

- Average physical condition rating: The weighted average condition of all existing assets on TERM’s condition scale of 5 (excellent) through 1 (poor).

- Investment backlog: The value of all deferred capital investment, including assets exceeding their useful lives and rehabilitation activities that are past due. (This value can approach but never reach zero due to assets continually aging, with some exceeding their useful lives.) The backlog is presented here both as a total dollar amount and as a percent of the total replacement value of all U.S. transit assets.

- Backlog ratio: The ratio of the current investment backlog to the annual level of investment required to maintain normal annual capital needs once the backlog is eliminated.

- Performance measures: The impact of investments on U.S. transit ridership capacity and system reliability.

- New boardings supported by expansion investments: The number of additional riders that transit systems can carry without a loss in performance (given the projected ridership assumptions for each scenario).

- Revenue service disruptions per PMT: Number of disruptions to revenue service per million passenger miles.

- Fleet maintenance cost per vehicle revenue mile: Fleet maintenance costs tend to increase with fleet age (or reduced asset condition). This measure estimates the change in fleet maintenance costs expressed in a per-revenue-vehicle-mile basis.

Exhibit 7-21: Scenario Investment Benefits Scorecard

| Measure | Baseline 2014 Actual Spending, Conditions and Performance | SGR | Sustain 2014 Spending | Low Growth | High Growth |

|---|---|---|---|---|---|

| Average Annual Expenditures (Billions of 2014 Dollars) | |||||

| Preservation | $10.3 | $18.4 | $11.3 | $17.4 | $17.5 |

| Expansion | $7.0 | NA | $6.4 | $6.0 | $8.1 |

| Total | $17.3 | $18.4 | $17.7 | $23.4 | $25.6 |

| Conditions (Existing Assets) | |||||

| Average Physical Condition Rating | 3.1 | 3.0 | 2.8 | 3.3 | 3.4 |

| Investment Backlog (Billions of Dollars) | $98.0 | $0.0 | $109.2 | $0.0 | $0.0 |

| Investment Backlog (% of Replacement Costs) | 12.0% | 0.0% | 13.4% | 0.0% | 0.0% |

| Backlog Ratio1 | 7.3 | 0.0 | 8.1 | 0.0 | 0.0 |

| Performance | |||||

| Ridership Impacts of Expansion Investments (2014) | |||||

| New Boardings Supported by Expansion (Billions) | NA | NA | 3.7 | 3.0 | 4.6 |

| Total Projected Boardings in 2034 (Billions) | NA | NA | 14.0 | 13.4 | 14.9 |

| Fleet Performance | |||||

| Revenue Service Disruptions per Thousand PMT | 9.5 | 9.8 | 9.5 | 9.8 | 9.8 |

|

Fleet Maintenance Cost per Revenue Vehicle Mile |

$1.91 | $1.92 | $1.89 | $1.92 | $1.92 |

1The backlog ratio is the ratio of the current investment backlog to the annual level of investment to maintain SGR once the backlog is eliminated.

Source: Transit Economic Requirements Model.

Scorecard Comparisons

Exhibit 7-21 summarizes a review of the scorecard results for each of the three investment scenarios and the SGR Benchmark reveals the impacts discussed below.

Continued reinvestment at the 2014 annual spending level is likely to yield a decline in overall asset conditions (from 3.1 in 2014 to 2.8 in 2034) and an increase in the size of the investment backlog (from $98.0 billion in 2014 to $109.2 billion in 2034). Continued reinvestment at the 2014 annual spending level, however, likely will cause no change in service disruptions per thousand passenger miles and a decrease in maintenance costs per vehicle revenue mile. In contrast, with the exception of overall asset conditions, opposite results occur under the SGR Benchmark, the Low-Growth scenario, and the High-Growth scenario. Note that the overall condition rating measures of 3.0, 3.3, and 3.4 under the SGR Benchmark, the Low-Growth scenario, and the High-Growth scenario, respectively, represent sustainable condition levels for the Nation’s existing transit assets over the long term. This is in contrast to the current measure of roughly 3.1, which would be difficult to maintain over the long term without replacing many asset types prior to the conclusion of their expected useful lives.

For this report, expansion assets are included in the overall condition rating measures. This approach is a departure from that used in previous reports, in which the goal was to be cognizant of what happens to the SGR of existing assets under alternative scenarios.

Although continued expansion investment at the 2014 annual spending level appears sufficient to support a low rate of increase in transit ridership to about 3.7 billion new boardings in 2034, higher rates of growth to nearly 4.6 billion new boardings in 2034 suggest that a significantly higher rate of expansion investment (nearly $1 billion more annually in expansion investment) would be required to avoid a decline in overall transit performance (e.g., in the form of increased crowding on high-utilization systems) if future transit ridership growth were to exceed historical levels.